In today’s rapidly evolving digital landscape, blockchain technology has emerged as a powerful force reshaping various industries, with banking at the forefront. Defined by its decentralized structure, enhanced security, and immutable recordkeeping, blockchain offers a radical departure from traditional financial systems. As banks face mounting pressure to improve transparency, reduce operational costs, and guard against cyber threats, many are turning to blockchain to modernize their infrastructure. This article explores what blockchain technology is and delves into how it is transforming the banking sector—from streamlining cross-border payments to enabling smart contracts and beyond.

What is Blockchain Technology?

Blockchain technology is a decentralized digital ledger system that records transactions across a network of computers in a secure, transparent, and tamper-proof manner. Unlike traditional centralized databases managed by a single authority, blockchain distributes data across multiple nodes, ensuring that once information is added, it cannot be altered or deleted without consensus from the network. Each transaction is grouped into a “block,” and these blocks are cryptographically linked to form a continuous “chain”—hence the name. This structure enhances data integrity, prevents unauthorized access, and enables trust among participants without relying on intermediaries. As a result, blockchain is gaining traction as a reliable foundation for secure digital transactions in sectors like finance, healthcare, and supply chain management.

How blockchain technology Works

How blockchain technology Works

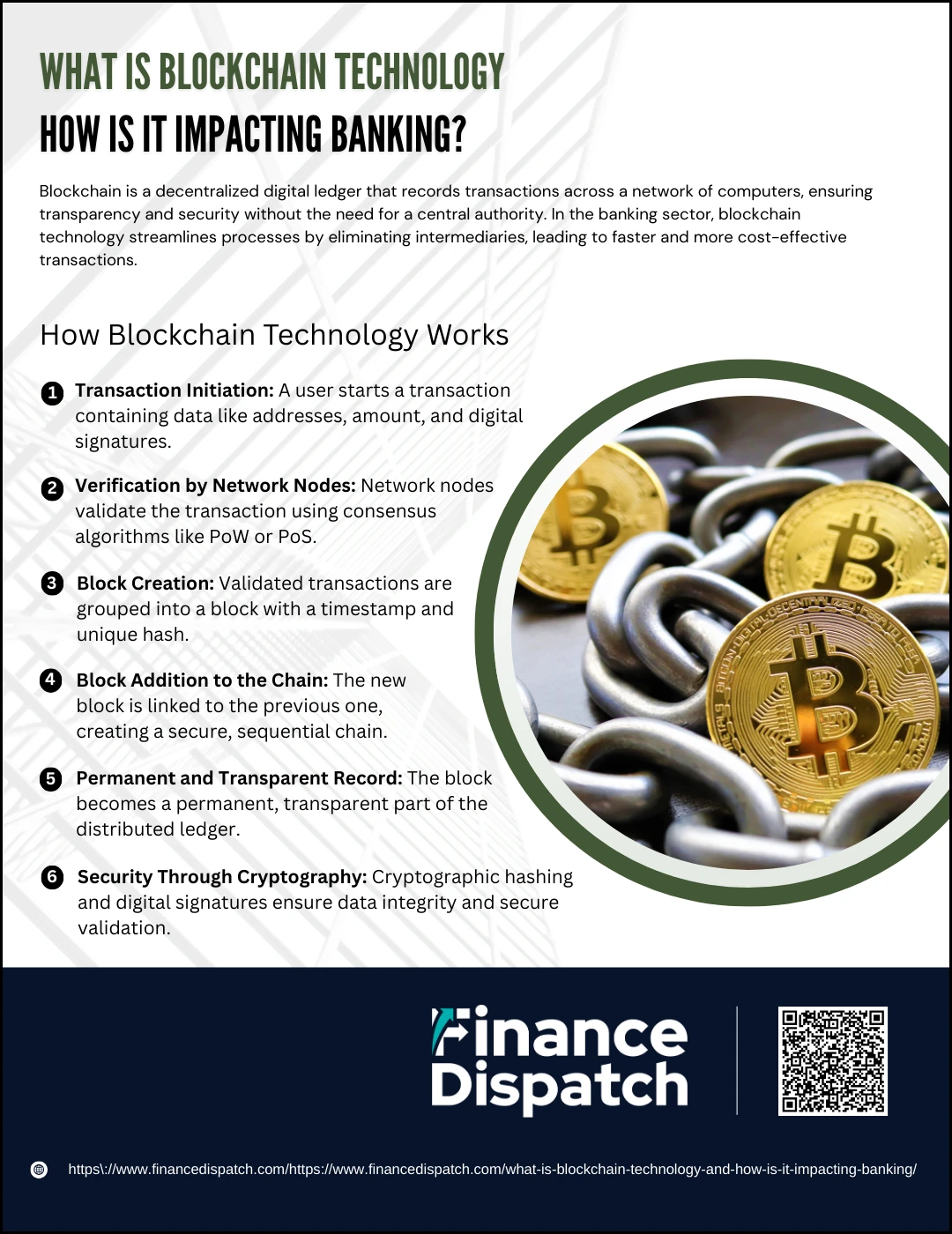

Blockchain is a revolutionary technology that enables secure, transparent, and decentralized recordkeeping across a peer-to-peer network. It eliminates the need for a central authority by allowing participants (nodes) to validate and store data collectively. This process ensures data integrity, transparency, and trust. Here’s a detailed breakdown of how blockchain functions step by step:

1. Transaction Initiation

A blockchain process begins when a user initiates a transaction. This could involve sending cryptocurrency, updating a record, or executing a smart contract. The transaction contains critical information such as sender and receiver addresses, the amount or data involved, and digital signatures for security. Once created, the transaction is broadcast to the blockchain network for validation.

2. Verification by Network Nodes

After the transaction is broadcast, it needs to be verified. This is done by a network of decentralized nodes (computers) that apply specific consensus algorithms—like Proof of Work (PoW) or Proof of Stake (PoS)—to validate the transaction. These algorithms ensure that only legitimate and authorized transactions are added to the blockchain. This verification process prevents double-spending, fraud, or unauthorized changes.

3. Block Creation

Once a transaction (or a group of transactions) is verified, it is bundled into a “block.” Each block contains:

- The verified transaction(s)

- A timestamp

- A reference (hash) to the previous block

- A unique cryptographic hash representing its data

4. Block Addition to the Chain

After a block is created, it is linked to the most recent block in the chain through its unique hash value. This hash functions like a digital fingerprint and connects the blocks in sequential order. This linking ensures that any tampering with one block would invalidate all subsequent blocks, making the blockchain tamper-resistant and secure by design.

5. Permanent and Transparent Record

Once added to the chain, the block and its transaction data become a permanent part of the blockchain ledger. This record is visible and accessible to all participants in the network (depending on whether it’s a public or permissioned blockchain). The transparency of the system builds trust among users, while the decentralized nature ensures that no single entity can alter the history.

6. Security Through Cryptography

Blockchain uses advanced cryptographic techniques to secure data. Each block’s hash is generated from its data using a cryptographic function. If even a single character of the block’s data changes, the hash changes entirely, making any tampering obvious. Additionally, digital signatures ensure that only authorized users can initiate valid transactions, and consensus mechanisms ensure the network collectively agrees on the validity of each new block.

Key Features of Blockchain Relevant to Banking

Blockchain technology offers a transformative set of features that align closely with the needs of the banking sector. As financial institutions seek to improve security, transparency, and operational efficiency, blockchain provides a decentralized infrastructure that addresses many traditional challenges. From reducing fraud to enabling real-time transactions, these features are driving innovation in how banks operate and serve their customers.

1. Decentralization: Removes the need for a central authority by distributing control across a network, reducing single points of failure and enhancing system resilience.

2. Immutability: Once data is recorded on the blockchain, it cannot be altered or deleted. This ensures the integrity of financial records and prevents tampering or fraud.

3. Transparency: Transactions are visible to all authorized participants in the network, increasing accountability and trust among stakeholders.

4. Security: Advanced cryptographic algorithms protect data and transactions, making it nearly impossible for unauthorized users to alter records or initiate fraudulent activity.

5. Efficiency: Automates processes like settlements and verifications, reducing manual work, cutting costs, and enabling faster transaction processing.

6. Smart Contracts: Self-executing contracts stored on the blockchain that automatically enforce rules and terms, streamlining activities such as loan approvals and compliance checks.

7. Auditability: Every transaction is time-stamped and permanently recorded, making it easy to trace and verify the flow of funds—essential for regulatory compliance.

8. Interoperability: Enables integration with existing systems and other blockchain platforms, allowing seamless communication and data sharing across institutions.

How blockchain technology Impacting on Banking

How blockchain technology Impacting on Banking

Blockchain technology is transforming the traditional banking model by introducing a decentralized, secure, and highly efficient system for handling financial transactions and data. Unlike conventional systems that rely on centralized databases and intermediaries, blockchain allows banks to operate with increased transparency, speed, and trust. As a result, many financial institutions are integrating blockchain into their operations to remain competitive in the digital age. Below are the major ways blockchain is making an impact on banking:

1. Faster and Cheaper Transactions

Traditional bank transfers, especially international ones, can take several days to settle and often involve high fees. Blockchain eliminates intermediaries like correspondent banks and clearinghouses, allowing transactions to be processed within minutes or even seconds, with significantly lower costs.

2. Enhanced Security and Fraud Prevention

Blockchain’s decentralized nature, combined with cryptographic encryption, makes it extremely difficult for hackers to alter transaction records. Once a transaction is validated and added to the blockchain, it becomes immutable, reducing the risk of fraud, cyberattacks, and unauthorized access to sensitive data.

3. Reduced Operational Costs

Banking operations involve high costs related to manual paperwork, reconciliation, and third-party verifications. Blockchain automates these processes through smart contracts and shared ledgers, cutting administrative burdens and enabling banks to save billions annually.

4. Improved Transparency and Auditability

Every transaction on the blockchain is permanently recorded and time-stamped. This allows banks, customers, and regulators to trace the entire history of a transaction, making auditing and compliance reporting faster, more accurate, and more reliable.

5. Streamlined Compliance and KYC Processes

Know Your Customer (KYC) and Anti-Money Laundering (AML) processes are often repetitive and inefficient across banks. Blockchain enables secure, real-time sharing of verified customer identities between institutions, reducing duplication, speeding up onboarding, and improving regulatory compliance.

6. New Financial Products and Services

Blockchain opens doors to new offerings such as decentralized lending, tokenized assets, and programmable financial products via smart contracts. Banks can use these innovations to expand their product lines and attract tech-savvy customers.

7. Increased Financial Inclusion

Blockchain-powered financial services require only an internet connection, which helps bring banking to unbanked and underbanked populations. Digital wallets and mobile blockchain platforms allow people in remote areas to access and use basic banking services without needing a physical bank branch.

Real-World Examples of Blockchain in Banking

As blockchain technology matures, leading banks and financial institutions around the world are launching real-world projects to test and implement its capabilities. These initiatives aim to enhance efficiency, security, and transparency across various banking functions such as payments, trade finance, and loan servicing. Below are notable examples of how blockchain is being applied in the banking industry today:

- JPMorgan Chase – Kinexys (formerly Onyx): A private blockchain network used for wholesale payments, securities settlement, and foreign exchange. It handles over $2 billion in daily transactions and connects clients globally.

- Fnality International: A consortium including Santander, HSBC, Barclays, and UBS, focused on using “utility settlement coins” to simplify and speed up cross-border payments backed by central bank reserves.

- JPMorgan Chase – Link: A permissioned blockchain platform that improves interbank communication, helping over 400 institutions streamline payment inquiries and account verifications.

- Project Agora (Bank for International Settlements): Built on the R3 Corda platform, this initiative tokenizes trade finance assets like invoices and letters of credit to enhance transparency and reduce fraud.

- Canton Network (Goldman Sachs, Deutsche Börse, SIX): A privacy-enabled, interoperable blockchain designed for institutional asset handling and smart contract execution across financial markets.

- Versana Platform: Backed by major banks such as JPMorgan, Citi, and Barclays, this platform uses blockchain and smart contracts to modernize syndicated loan servicing with real-time data sharing.

Challenges and Limitations of blockchain technology

While blockchain technology holds great promise for transforming industries like banking, it is not without its challenges. From technical barriers to regulatory uncertainties, several limitations have slowed its widespread adoption. For blockchain to reach its full potential, these issues must be addressed through innovation, collaboration, and policy development. Below are some of the key challenges and limitations currently facing blockchain technology:

- Scalability Issues: Many blockchain networks struggle to process a large volume of transactions quickly, leading to delays, congestion, and high transaction fees—especially during peak usage.

- Integration with Legacy Systems: Banks and large enterprises often operate on outdated IT infrastructures that are not easily compatible with blockchain platforms, making integration costly and complex.

- Regulatory Uncertainty: The lack of clear and consistent regulations around blockchain and cryptocurrencies across different countries creates legal risks and discourages investment.

- Privacy Concerns: Public blockchains are transparent by nature, which can conflict with privacy laws like GDPR and the confidentiality requirements of financial institutions.

- High Energy Consumption: Some consensus mechanisms, such as Proof of Work, require significant computational power, leading to concerns about environmental sustainability.

- Interoperability Challenges: Different blockchain platforms often use incompatible technologies, making it difficult for systems to communicate or share data efficiently across networks.

- Lack of Standardization: The blockchain ecosystem lacks uniform standards for development, security, and data sharing, which hinders widespread adoption and trust.

- Security Risks in Smart Contracts: Although smart contracts are automated, poorly coded contracts can be exploited, leading to financial losses and security vulnerabilities.

Future Outlook of blockchain technology

The future of blockchain technology appears promising as it continues to evolve from a niche innovation into a foundational component of digital infrastructure across industries. In banking, its potential to streamline operations, enhance security, and reduce costs is pushing more institutions toward pilot programs and large-scale implementations. As regulatory clarity improves and interoperability standards develop, adoption is expected to accelerate. Emerging use cases—such as central bank digital currencies (CBDCs), decentralized finance (DeFi), and asset tokenization—are likely to redefine the financial landscape. With ongoing advancements in scalability, privacy, and energy efficiency, blockchain is positioned to become a critical driver of transparency, trust, and innovation in the global economy.

Conclusion

Blockchain technology is redefining the foundations of the banking industry by offering a decentralized, secure, and transparent alternative to traditional systems. From speeding up cross-border transactions to enabling smart contracts and improving fraud prevention, its benefits are already being realized through real-world applications. However, challenges such as scalability, regulatory uncertainty, and integration with legacy systems continue to hinder widespread adoption. Despite these obstacles, the momentum behind blockchain innovation is strong, and its future in banking looks increasingly inevitable. As the technology matures and global standards emerge, blockchain is set to play a pivotal role in shaping the next generation of financial services.