Maintaining control over your finances often comes down to understanding how much of your income goes toward paying off debt. One of the most important tools for measuring this is your debt-to-income (DTI) ratio. Whether you’re applying for a mortgage, personal loan, or credit card, lenders use this ratio to evaluate how responsibly you manage debt and whether you can afford to take on more. In this article, we’ll explore what the debt-to-income ratio is, how it’s calculated, and why it plays such a crucial role in lending decisions.

What Is a Debt-to-Income (DTI) Ratio?

A debt-to-income (DTI) ratio is a financial metric that compares your total monthly debt payments to your gross monthly income. It represents the percentage of your income that goes toward repaying debts such as credit cards, loans, and housing costs. For example, if you earn $5,000 a month before taxes and spend $2,000 on debt payments, your DTI ratio would be 40%. This ratio gives lenders a clear picture of your financial obligations and helps them assess whether you can comfortably handle additional debt. A lower DTI indicates better financial balance, while a higher DTI may signal increased risk to lenders.

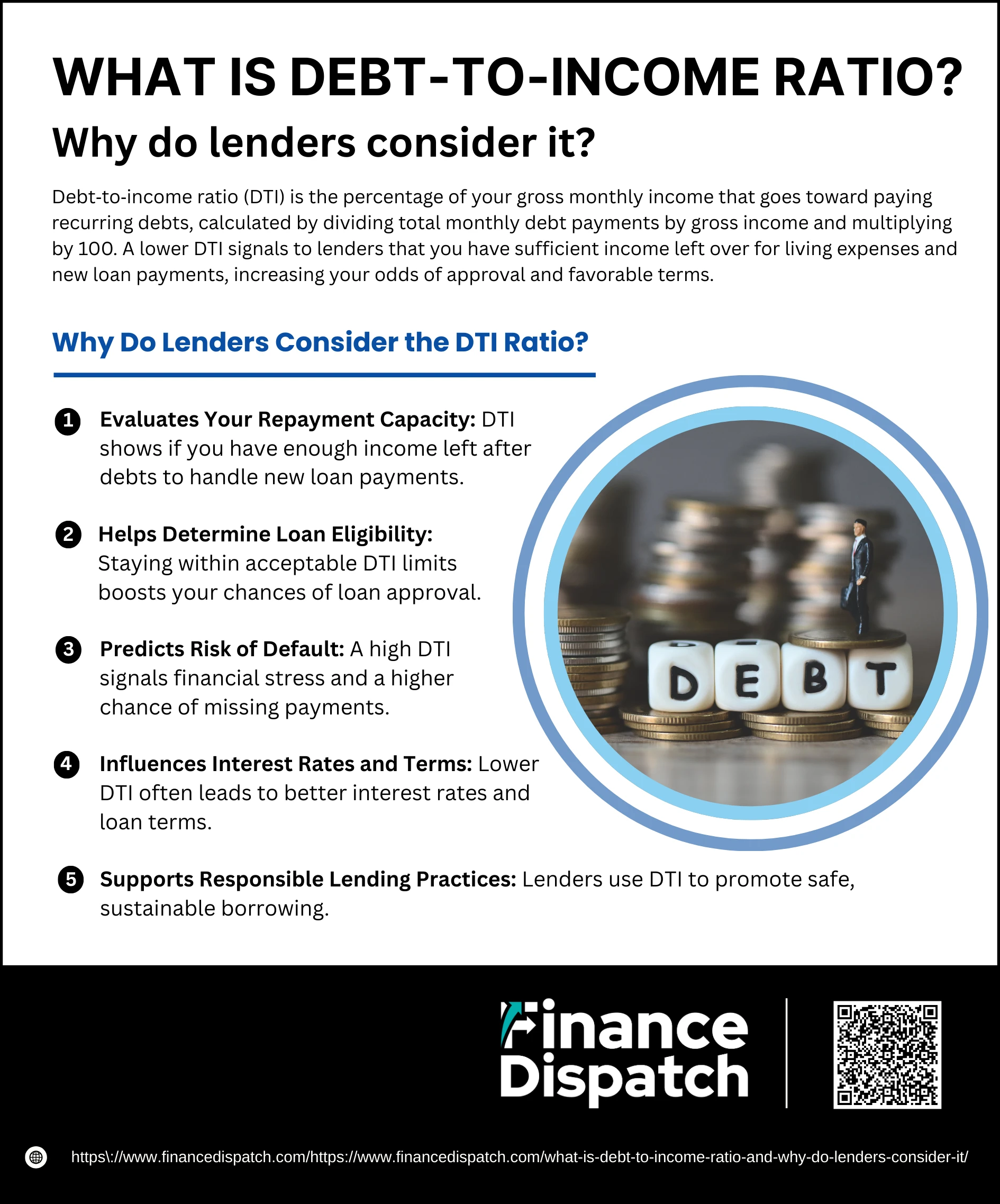

Why Do Lenders Consider the DTI Ratio?

Why Do Lenders Consider the DTI Ratio?

Lenders use the debt-to-income (DTI) ratio to assess your ability to take on and repay additional debt. It’s more than just a number—it’s a financial snapshot that helps them determine whether you are financially overextended or well-positioned for a new loan. A high DTI ratio can be a red flag for lenders, suggesting that you may struggle to manage new debt, while a lower ratio demonstrates strong financial health. Below are the main reasons lenders give serious weight to your DTI:

1. Evaluates Your Repayment Capacity

Lenders want to ensure that borrowers have enough income left over after paying current debts to comfortably handle new loan payments. The DTI ratio shows how much of your income is already committed to existing obligations. If a significant portion of your income is already being used to repay debts, lenders may question whether you can reliably repay another loan. A lower DTI ratio indicates you have a cushion in your budget, which reassures lenders of your ability to repay.

2. Helps Determine Loan Eligibility

Most lenders have defined thresholds for acceptable DTI ratios depending on the loan type. For example, while many conventional mortgages prefer a back-end DTI below 36%, FHA loans may accept higher ratios, up to 57% in some cases. If your DTI is within the acceptable range, you’re more likely to qualify for a loan. If it exceeds those limits, your application might be denied—even if your credit score is high—because your income appears overburdened by debt.

3. Predicts Risk of Default

The DTI ratio is a reliable predictor of a borrower’s financial stress. A high DTI means a large portion of your income is already allocated toward debt, leaving less room for emergencies or unexpected expenses. This can increase the chances of missed payments or loan defaults, especially if income decreases or expenses rise. Lenders consider borrowers with high DTI ratios to be riskier, as they’re statistically more likely to fall behind on repayments.

4. Influences Interest Rates and Terms

Even if a high DTI ratio doesn’t disqualify you from a loan, it can affect the interest rate and terms offered. Borrowers with lower DTI ratios are often rewarded with more favorable loan terms, such as lower interest rates or higher credit limits. This is because they represent a lower risk to the lender. On the other hand, a higher DTI could result in higher rates or stricter repayment conditions to offset the lender’s risk.

5. Supports Responsible Lending Practices

Regulations such as those enforced by the Consumer Financial Protection Bureau (CFPB) encourage lenders to assess a borrower’s ability to repay a loan. Using the DTI ratio helps ensure that credit is extended responsibly and that borrowers are not set up to fail. By including DTI analysis in their decision-making process, lenders help reduce the risk of loan defaults, protect borrowers from overextending themselves, and contribute to overall financial system stability.

How to Calculate Debt-to-Income Ratio

Calculating your debt-to-income (DTI) ratio is a simple yet powerful way to assess your financial health and determine whether you’re in a good position to take on more debt. The DTI ratio shows what percentage of your gross income goes toward paying off monthly debt obligations. Understanding this number can help you make informed decisions about budgeting, borrowing, and long-term financial planning. Here’s how to calculate it:

Steps to Calculate Your Debt-to-Income Ratio:

1. List all your monthly debt payments

Include minimum payments for credit cards, mortgage or rent, auto loans, student loans, personal loans, and any court-ordered obligations like child support or alimony.

2. Determine your gross monthly income

This is your total income before taxes and deductions. It includes your salary, bonuses, freelance income, and other consistent income sources.

3. Divide total monthly debt by gross monthly income

Take the sum of your debt payments and divide it by your gross income to get a decimal value.

4. Multiply the result by 100

Convert the decimal into a percentage by multiplying by 100. This percentage is your debt-to-income ratio.

What Is a Good Debt-to-Income Ratio?

A good debt-to-income (DTI) ratio indicates that you have a healthy balance between income and debt, making you a lower-risk borrower in the eyes of lenders. While acceptable DTI thresholds can vary depending on the type of loan or lender, a lower percentage is generally better. Lenders use your DTI to evaluate whether you can take on new debt without compromising your financial stability. Here’s a breakdown of what different DTI ranges typically mean:

Debt-to-Income Ratio Guidelines

| DTI Range | Financial Health Indicator | Lender’s Perspective |

| Below 20% | Excellent — very low debt burden | Very likely to be approved with favorable terms |

| 20% – 35% | Good — manageable debt levels | Generally qualifies for most loans |

| 36% – 43% | Acceptable — may be approaching risk level | May qualify, especially for FHA or VA loans |

| 44% – 50% | Risky — tight budget | Possible approval with higher interest or limits |

| Above 50% | High risk — over-leveraged | Often denied; considered financially overextended |

Front-End vs. Back-End DTI

When evaluating a borrower’s debt-to-income ratio, especially for mortgage applications, lenders often break it down into two parts: front-end and back-end DTI. Both ratios give insight into different aspects of your financial obligations. The front-end DTI focuses solely on housing-related expenses, while the back-end DTI takes into account all of your monthly debt obligations. Understanding the difference between the two can help you better assess your financial standing and prepare for loan approval.

Comparison of Front-End vs. Back-End DTI

| Aspect | Front-End DTI | Back-End DTI |

| Definition | Portion of income spent on housing costs | Portion of income spent on total monthly debt obligations |

| Includes | Mortgage or rent, property taxes, insurance, HOA fees | Front-end items plus car loans, credit cards, student loans, etc. |

| Typical Limit (Conventional Loans) | Around 28% | Up to 36%–43% (some lenders allow up to 50%) |

| Used in | Mortgage pre-qualification and affordability analysis | Full loan approval assessment |

| Purpose | Evaluates ability to afford housing alone | Evaluates overall financial capacity and risk |

Does DTI Ratio Affect Your Credit Score?

The debt-to-income (DTI) ratio does not directly affect your credit score because credit scoring models, such as those used by FICO or VantageScore, do not consider your income as part of their calculation. However, the factors that influence your DTI—like how much debt you carry—can indirectly impact your credit score. For example, high credit card balances relative to your limits (known as credit utilization) can both raise your DTI and lower your credit score. Similarly, if you reduce your debt or pay off loans, your DTI improves and your credit score may also benefit. While your DTI isn’t shown on your credit report, lenders often consider it alongside your credit score when assessing your overall financial health and creditworthiness.

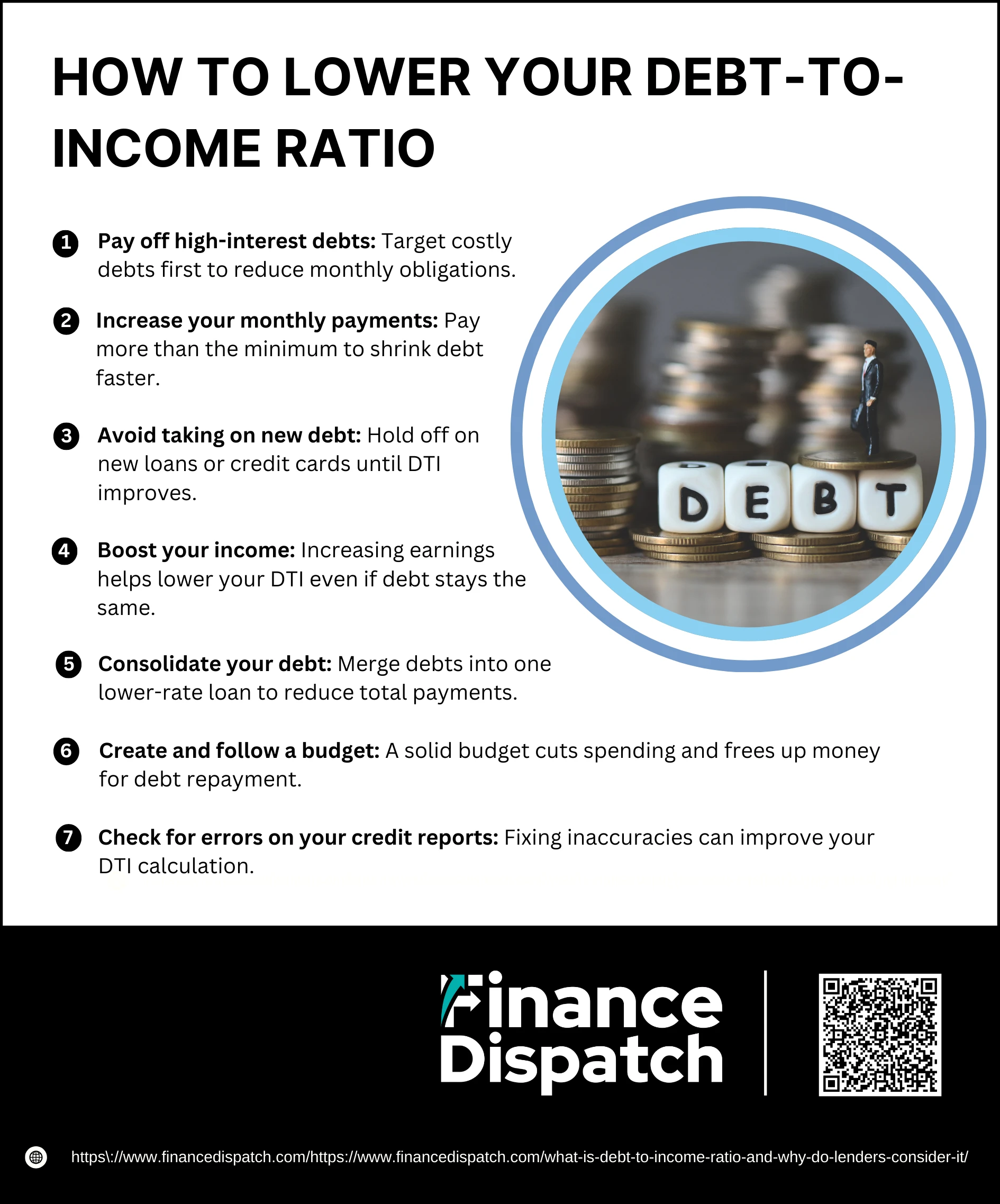

How to Lower Your Debt-to-Income Ratio

How to Lower Your Debt-to-Income Ratio

Lowering your debt-to-income (DTI) ratio is essential for gaining financial flexibility and improving your chances of loan approval. A high DTI ratio may suggest that you’re overextended, making it harder to qualify for favorable loan terms. Whether you’re planning to apply for a mortgage, a personal loan, or simply aiming to get your finances under control, reducing your DTI can make a significant difference. Below are actionable steps you can take, explained in greater detail:

Steps to Lower Your Debt-to-Income Ratio

1. Pay off high-interest debts

Start by tackling debts that carry high interest rates, such as credit card balances. These debts often come with higher minimum payments, which inflate your DTI. Paying them down or off completely reduces your monthly obligations and frees up more of your income.

2. Increase your monthly payments

Paying more than the minimum due on loans and credit cards helps reduce the principal balance faster. This not only lowers your debt over time but also decreases the monthly amount factored into your DTI ratio.

3. Avoid taking on new debt

Adding new loans or credit card balances increases your total monthly debt payments, raising your DTI. Delay large purchases that require financing until your DTI ratio is under control. Focus on reducing existing debts first.

4. Boost your income

If feasible, pursue additional income sources. This could mean negotiating a raise, finding freelance work, launching a side business, or switching to a higher-paying job. Since DTI is calculated using gross income, increasing your earnings can significantly improve your ratio even if your debt stays the same.

5. Consolidate your debt

Debt consolidation involves combining multiple high-interest debts into a single loan—usually at a lower interest rate. This can reduce your total monthly payments, streamline your finances, and help you pay down debt more efficiently, ultimately lowering your DTI.

6. Create and follow a budget

Building a realistic monthly budget helps you identify unnecessary expenses and areas where you can cut back. Allocating these savings toward debt repayment accelerates your progress in reducing your DTI.

7. Check for errors on your credit reports

Sometimes, outdated or incorrect debt amounts are reported on your credit history, which may artificially raise your DTI. Review your credit reports regularly and dispute any inaccuracies that could be misrepresenting your financial obligations.

Conclusion

Understanding and managing your debt-to-income (DTI) ratio is a crucial step toward achieving financial stability and securing favorable loan opportunities. While your credit score often takes the spotlight, your DTI offers lenders a deeper look into how well you manage your existing financial obligations. A low DTI signals responsible borrowing habits and improves your chances of loan approval, while a high DTI may indicate financial strain. By regularly calculating your ratio, reducing debt, and increasing income where possible, you can take control of your finances and make smarter decisions about borrowing. Whether you’re preparing for a major purchase or simply aiming for healthier financial habits, keeping your DTI in check is a move in the right direction.