In today’s fast-paced financial world, every second counts when money changes hands. Traditional settlement systems, which often process payments in batches at the end of the day, can create frustrating delays that affect businesses, banks, and consumers alike. Real-Time Settlement offers a modern solution by processing transactions instantly and individually, ensuring funds move seamlessly without waiting periods. By eliminating bottlenecks and reducing settlement risks, this system not only enhances speed but also builds greater trust and efficiency across the global financial network.

What is Real-Time Settlement?

Real-Time Settlement refers to the process of transferring and finalizing financial transactions instantly, without waiting for end-of-day batch processing. Unlike traditional systems where payments are grouped and settled later, real-time settlement ensures that each transaction is processed individually and irrevocably the moment it is initiated. This approach is commonly seen in systems like Real-Time Gross Settlement (RTGS) and Real-Time Payments (RTP), where funds are credited to the recipient’s account almost immediately. By offering immediate confirmation and availability of funds, real-time settlement has become a cornerstone of modern banking, especially for high-value or time-sensitive transactions.

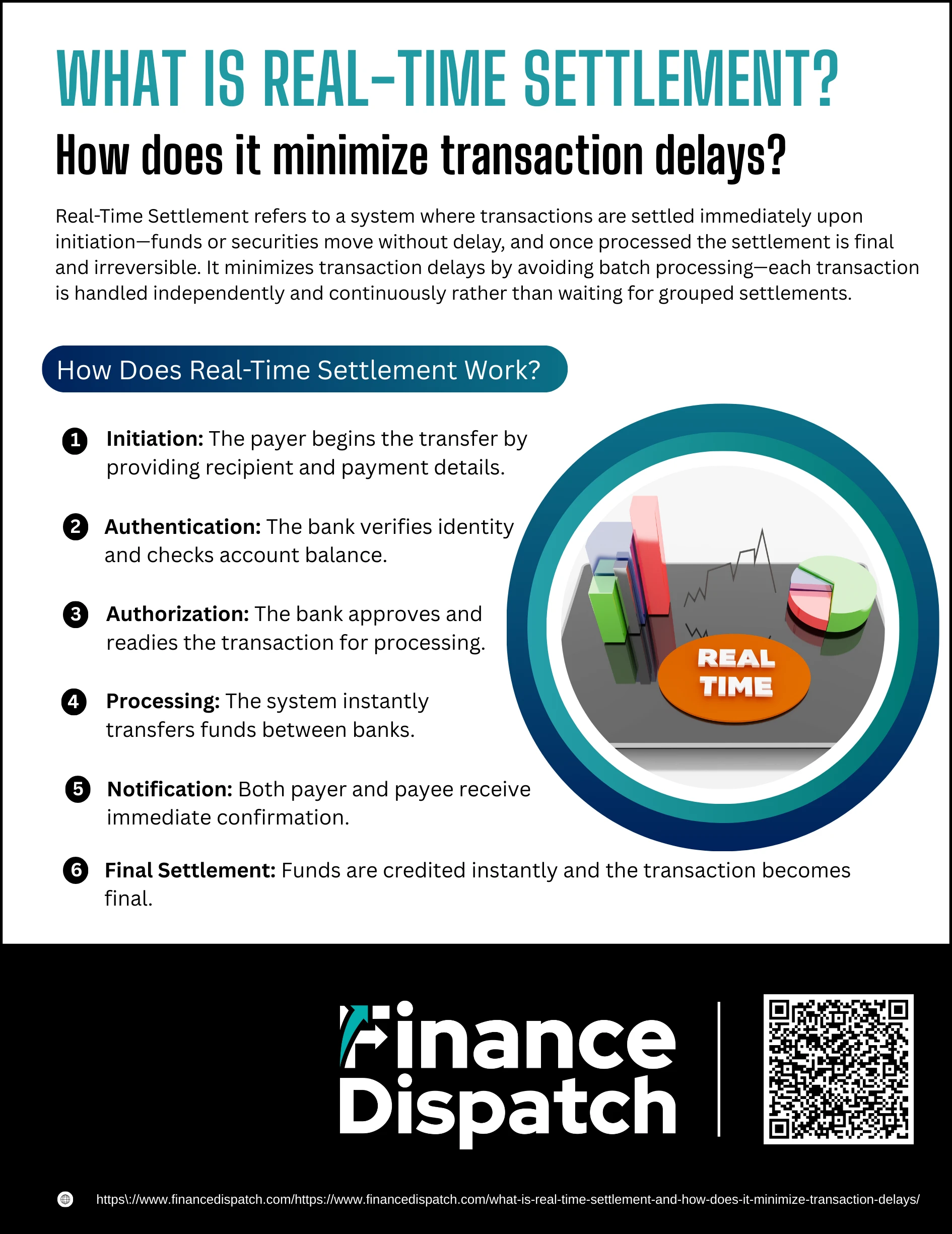

How Does Real-Time Settlement Work?

How Does Real-Time Settlement Work?

Real-Time Settlement ensures that every transaction is processed instantly and individually, rather than being grouped together in batches. This system provides immediate confirmation, reduces risks, and ensures funds are available to the recipient without delay. Here’s a closer look at how the process unfolds step by step:

1. Initiation

The process begins when the payer decides to transfer money. This can be done through online banking, mobile banking apps, QR code scanning, or even at a physical bank branch. At this stage, the payer provides details such as the recipient’s name, account number, and transfer amount.

2. Authentication

Once the transaction request is submitted, the payer’s bank verifies the identity of the payer. This could involve entering a password, providing a one-time PIN (OTP), biometric authentication like a fingerprint or facial scan, or two-factor verification. At the same time, the bank checks if the payer’s account has enough balance to cover the transaction.

3. Authorization

If the verification is successful and sufficient funds are available, the payer’s bank authorizes the transaction. This means the payment instruction is formally approved and ready to be sent to the settlement system for processing.

4. Processing

The transaction details are then transmitted through the real-time settlement system. Unlike traditional systems that wait until the end of the day to process payments, this system handles transactions one by one, immediately. The central bank (or a designated authority) updates the accounts involved by deducting funds from the sender’s bank and crediting the recipient’s bank.

5. Notification

Once the processing is complete, both the payer and the payee are notified instantly. These confirmations usually arrive via SMS, email, or push notifications from a mobile banking app. This transparency reassures both parties that the payment has gone through successfully and without delay.

6. Final Settlement

The last step is the actual crediting of funds to the recipient’s account. In real-time settlement systems, this happens almost immediately, making the funds available for use right away. Importantly, the transaction is final and irrevocable at this stage, meaning it cannot be reversed, which reduces uncertainty and settlement risk.

How Real-Time Settlement Minimizes Transaction Delays

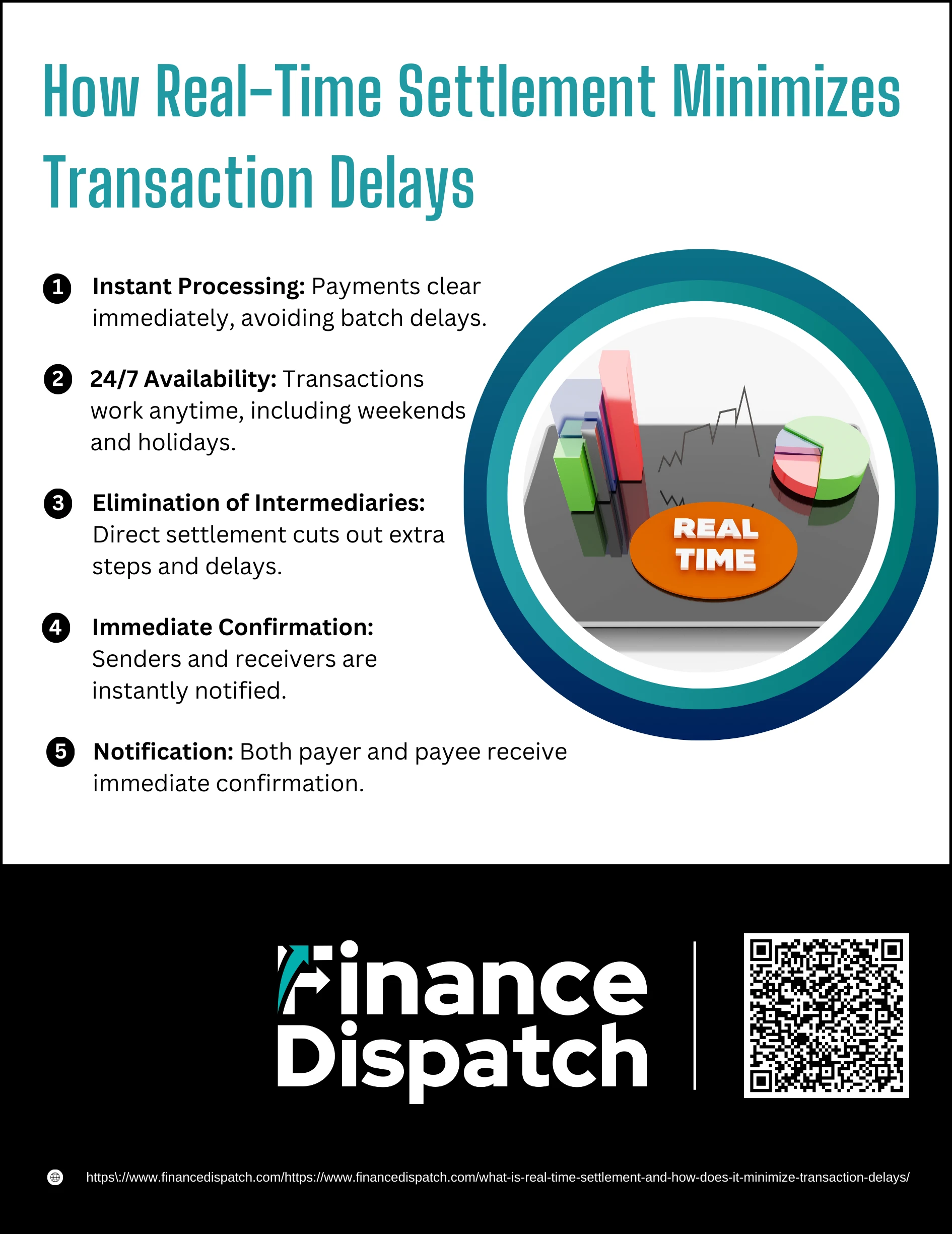

How Real-Time Settlement Minimizes Transaction Delays

One of the biggest advantages of real-time settlement is its ability to remove the waiting times and bottlenecks that occur in traditional payment systems. Instead of grouping payments into batches for end-of-day processing, every transaction is handled instantly and individually. This not only accelerates the speed of fund transfers but also ensures that both businesses and individuals can access their money right away. Here’s how it works:

1. Instant Processing

Traditional settlement systems like NEFT or BACS process payments in batches, which means transfers may take hours or even days to complete. Real-time settlement eliminates this delay by processing each transaction as soon as it is initiated. This immediate action prevents funds from being “stuck in transit” and ensures smooth, on-the-spot clearing.

2. 24/7 Availability

Older payment systems often operated only during business hours and excluded weekends or holidays, leading to further delays. Real-time settlement systems, by contrast, are increasingly designed to run around the clock—24 hours a day, 7 days a week. This continuous availability means users can transfer and access funds whenever they need, without waiting for banks to open.

3. Elimination of Intermediaries

In batch settlement systems, transactions may pass through multiple clearing houses or intermediaries before reaching the recipient. Each additional step adds time and complexity. Real-time settlement simplifies the process by directly adjusting balances between banks through a central authority (often the central bank). By cutting out unnecessary intermediaries, the system speeds up fund transfers significantly.

4. Immediate Confirmation

In traditional systems, uncertainty about whether a payment has gone through can cause delays in reconciliation and trust issues between parties. Real-time settlement addresses this by providing instant notifications to both the sender and the receiver. These confirmations—via SMS, email, or app alerts—assure both sides that the transaction is completed, saving time and reducing confusion.

5. Faster Fund Accessibility

Perhaps the most important benefit is that recipients can access their funds immediately after a transaction is completed. Businesses can manage cash flow more effectively, consumers can use their money without waiting, and governments can disburse subsidies or refunds instantly. This immediate fund availability minimizes liquidity issues and ensures that financial obligations can be met on time.

Real-Time Settlement vs. Traditional Methods

While traditional payment systems rely on batch processing and limited banking hours, real-time settlement processes each transaction instantly, offering speed and certainty. The contrast between these methods highlights why real-time settlement has become the preferred choice for high-value and time-sensitive transactions.

| Feature | Traditional Methods (Batch Settlement, BACS, NEFT, ACH) | Real-Time Settlement (RTGS, RTP) |

| Processing Style | Transactions grouped and processed in batches | Each transaction processed individually in real time |

| Settlement Speed | Hours to days, depending on cut-off times | Instantaneous, usually within seconds or minutes |

| Operating Hours | Restricted to banking hours, excludes weekends/holidays | 24/7 availability, including holidays |

| Fund Availability | Delayed; recipient may wait until next business day | Immediate; funds available instantly |

| Risk of Delays | Higher, due to system downtime, batching, or intermediaries | Very low, as settlement happens instantly |

| Use Cases | Routine or low-value payments (e.g., salaries, bills) | High-value or urgent payments needing immediate clearance |

Advantages of Real-Time Settlement

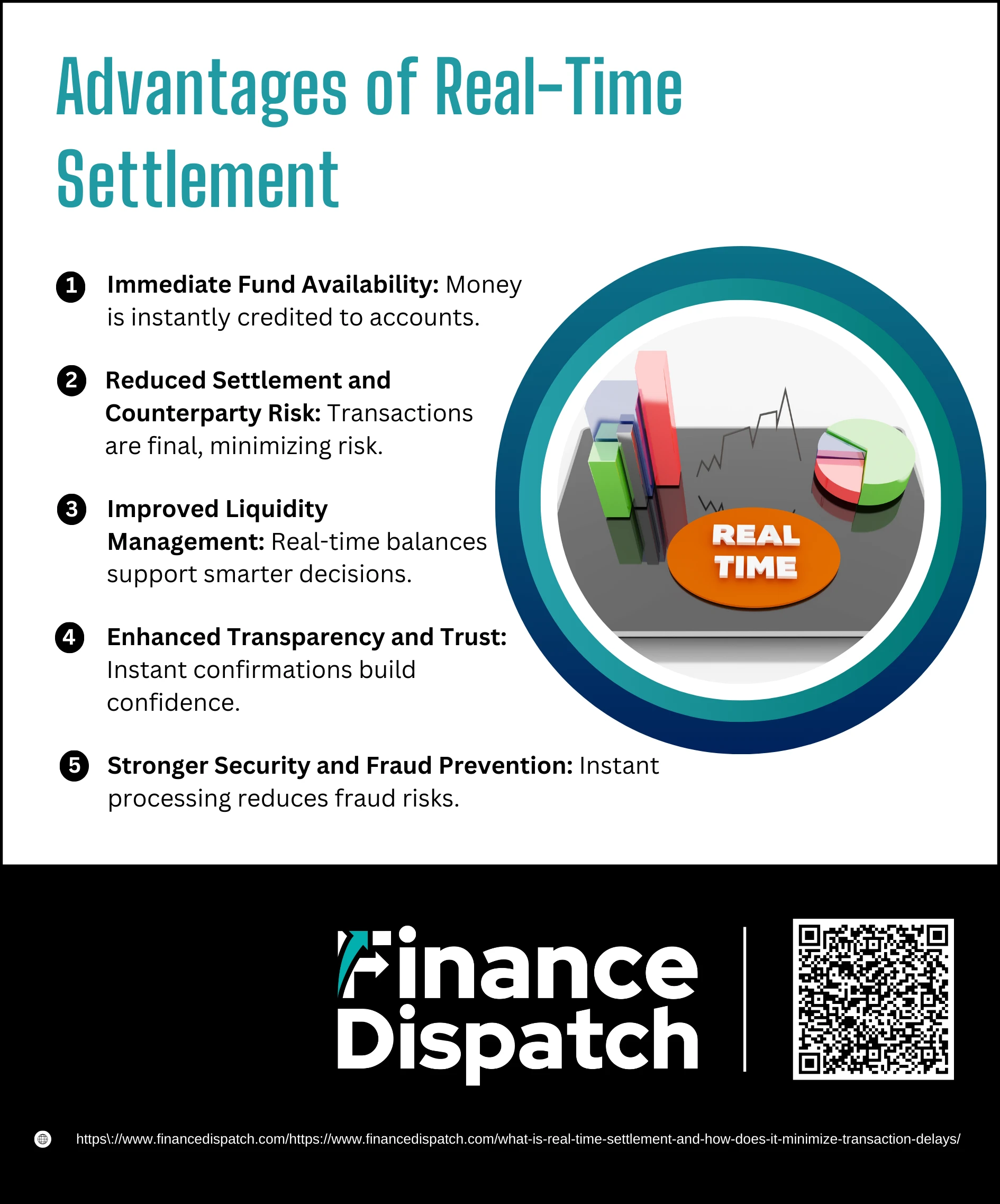

Advantages of Real-Time Settlement

Real-time settlement provides a faster, safer, and more reliable way to move money compared to traditional batch systems. By processing each transaction instantly and individually, it eliminates unnecessary delays and provides certainty to all parties involved. Below are the main advantages in detail:

1. Immediate Fund Availability

One of the most important benefits is that recipients can access their money right away. Instead of waiting hours or even days for funds to clear, businesses and individuals receive instant credit into their accounts. This is particularly useful for time-sensitive needs such as payroll processing, emergency transfers, or vendor payments.

2. Reduced Settlement and Counterparty Risk

In traditional settlement systems, there is always a risk that one party may default before the transaction clears. Real-time settlement removes this uncertainty because transactions are finalized the moment they are processed. This minimizes counterparty risk, making high-value transfers more secure and reliable.

3. Improved Liquidity Management

Real-time settlement gives banks, businesses, and individuals an accurate picture of their financial position at any given moment. With up-to-date cash balances, organizations can make better financial decisions, plan investments more effectively, and avoid the need for short-term borrowing to cover gaps.

4. Enhanced Transparency and Trust

Both the sender and receiver receive instant confirmation once the transaction is completed. This transparency builds confidence, as all parties know immediately that the transfer has gone through successfully. For businesses, this reduces disputes with clients or vendors, while for consumers it provides reassurance and trust.

5. Stronger Security and Fraud Prevention

Because transactions are processed and completed instantly, there is a much smaller window of vulnerability for fraudsters to exploit. Real-time settlement systems also use strong security measures like two-factor authentication, encryption, and central bank oversight, which help safeguard sensitive financial data and reduce the risk of cyberattacks.

Challenges and Limitations of Real-Time Settlement

While real-time settlement brings speed, transparency, and efficiency to financial transactions, it is not without challenges. Certain technical, financial, and operational limitations may affect its adoption and usability, especially in large-scale or cross-border environments.

1. Transaction Fees: Some systems charge higher fees for real-time processing, which can discourage smaller or frequent transactions.

2. Liquidity Requirements: Banks must maintain sufficient funds at all times to support instant settlements, which can strain resources.

3. Irreversible Transactions: Once processed, payments cannot be reversed, making errors or incorrect details costly.

4. System Dependency: Technical failures, cyberattacks, or downtime in banking infrastructure can disrupt real-time operations.

5. Limited Accessibility: Not all banks and regions provide universal real-time settlement services, reducing its availability.

6. Operational Hours in Some Systems: While many aim for 24/7 availability, some systems still restrict transactions to working hours, limiting convenience.

Technology Driving Real-Time Settlement

The growth of real-time settlement has been made possible by advanced technologies that ensure speed, security, and reliability in financial transactions. These innovations not only process payments instantly but also help detect fraud, improve interoperability, and provide transparency across global financial systems.

1. Blockchain and Distributed Ledger Technology (DLT): Enables secure, decentralized, and tamper-proof transaction records, reducing reliance on intermediaries.

2. Application Programming Interfaces (APIs): Facilitate seamless integration between banks, payment systems, and apps, ensuring instant data exchange for faster settlements.

3. Artificial Intelligence (AI) and Machine Learning (ML): Enhance fraud detection, automate processes, and identify anomalies in real-time to ensure safer transactions.

4. Central Bank Digital Currencies (CBDCs): Digital currencies issued by central banks that support instantaneous, regulated, and highly secure fund transfers.

5. Smart Contracts: Self-executing digital agreements that automatically trigger settlements once conditions are met, reducing manual errors and delays.

The Future of Real-Time Settlement

The future of real-time settlement looks promising as technology, regulation, and global adoption continue to evolve. With central banks worldwide introducing systems like FedNow in the U.S., TIPS in Europe, and UPI in India, instant payments are becoming the new standard for both high-value and everyday transactions. Emerging innovations such as blockchain, artificial intelligence, and central bank digital currencies (CBDCs) are expected to make settlements even faster, more secure, and accessible across borders. At the same time, regulatory frameworks and interoperability standards are being developed to ensure that different payment systems can seamlessly connect, reducing fragmentation. Together, these advancements point toward a financial ecosystem where delays are eliminated, risks are minimized, and efficiency is maximized for businesses and consumers alike.

Conclusion

Real-time settlement has redefined how financial transactions are conducted by removing delays, improving security, and providing immediate access to funds. Unlike traditional batch systems that create bottlenecks, it ensures every payment is processed instantly and irrevocably, minimizing risk and building trust. Supported by technologies like blockchain, APIs, and central bank digital currencies, real-time settlement is not just a tool for faster payments but a foundation for more efficient and transparent global finance. As adoption expands, it promises to strengthen liquidity, enhance customer confidence, and shape the future of a seamless, delay-free financial ecosystem.