Managing your money doesn’t have to be overwhelming or complicated. A budget is a simple yet powerful tool that helps you take control of your finances, track your spending, and work toward your financial goals with confidence. Whether you’re saving for a big purchase, paying off debt, or just aiming to live within your means, a budget serves as your financial roadmap. It’s not just about cutting expenses; it’s about aligning your money with your priorities and making informed decisions about where it goes. In this guide, we’ll explore what a budget is, why it’s essential, and provide a step-by-step approach to creating one that works for your unique lifestyle.

What is a Budget?

A budget is a financial plan that helps you manage your income and expenses over a specific period, such as a month or a year. It serves as a tool to allocate your money toward essential needs, discretionary spending, and financial goals like savings or debt repayment. Rather than being restrictive, a budget empowers you to take control of your finances by offering a clear picture of how much you earn, spend, and save. Whether you’re an individual, a family, or even a business, creating a budget provides a structured approach to prioritize your spending, avoid unnecessary debt, and build a foundation for long-term financial stability.

Why is Budgeting Important?

Budgeting is an essential tool that lays the foundation for financial health and stability. It allows you to take control of your money, plan for the future, and prepare for life’s uncertainties. A well-constructed budget is more than just a plan; it’s a pathway to achieving your financial goals, whether they involve saving for an emergency, reducing debt, or building wealth. Here’s a closer look at why budgeting is so important.

1. Gives Control Over Your Finances

Budgeting puts you in the driver’s seat of your financial life. By clearly tracking your income and expenses, you can see exactly where your money goes and make intentional decisions about how to allocate it. This clarity ensures that your spending aligns with your priorities and prevents financial chaos. Without a budget, it’s easy to lose track of your finances, leading to overspending or unnecessary debt. A budget ensures every dollar has a purpose, giving you control and confidence in your money management.

2. Encourages Savings

One of the key benefits of budgeting is its ability to help you save consistently. Whether it’s for short-term goals like a vacation or long-term objectives like retirement, a budget creates a structure for setting aside money regularly. By including savings as a category in your budget, you prioritize it just as you would your essential expenses. Over time, this consistent saving builds financial security, helping you prepare for planned and unplanned needs alike.

3. Helps Avoid Debt

Living without a budget often leads to spending beyond your means, which can result in accumulating debt. Budgeting prevents this by showing you how much money you have to work with and helping you live within your limits. It also allows you to allocate funds for paying down existing debt, reducing interest payments, and freeing up money for other goals. By sticking to a budget, you can avoid the stress and financial strain of falling into debt traps.

4. Supports Goal Achievement

A budget transforms your financial goals from vague dreams into actionable plans. Whether you want to save for a down payment on a house, start a business, or send your child to college, a budget provides the structure needed to make steady progress. It helps you break big goals into smaller, manageable steps, allowing you to allocate resources effectively and track your progress. With a budget, your goals feel more attainable and within reach.

5. Reduces Financial Stress

Financial uncertainty can be a major source of stress, but a budget provides peace of mind. By knowing exactly what you have and what you owe, you can plan for your expenses and avoid last-minute financial scrambles. A budget gives you a sense of preparedness, ensuring that you’re not caught off guard by bills or unexpected expenses. This clarity reduces anxiety and allows you to approach your finances with confidence.

6. Promotes Financial Awareness

Budgeting forces you to examine your spending habits closely, revealing patterns and areas where you might be overspending. It highlights opportunities to cut back and optimize, such as reducing discretionary spending or finding better deals on necessities. This increased awareness helps you make smarter financial decisions, ensuring that your money is used effectively to support your needs and goals.

7. Prepares for Unexpected Expenses

Life is full of surprises, and budgeting helps you prepare for them. By setting aside a portion of your income in an emergency fund, you create a financial cushion that can cover unexpected costs like medical bills, car repairs, or sudden job loss. This foresight prevents emergencies from turning into financial crises and gives you the confidence to face challenges without derailing your financial plans.

8. Builds Long-Term Stability

Budgeting isn’t just about managing today’s money; it’s about setting yourself up for a secure future. By consistently saving, managing debt, and spending wisely, you create a foundation for long-term financial stability. Over time, these habits allow you to build wealth, achieve financial independence, and enjoy a life free from financial worries. Budgeting creates a cycle of disciplined money management that benefits you for years to come.

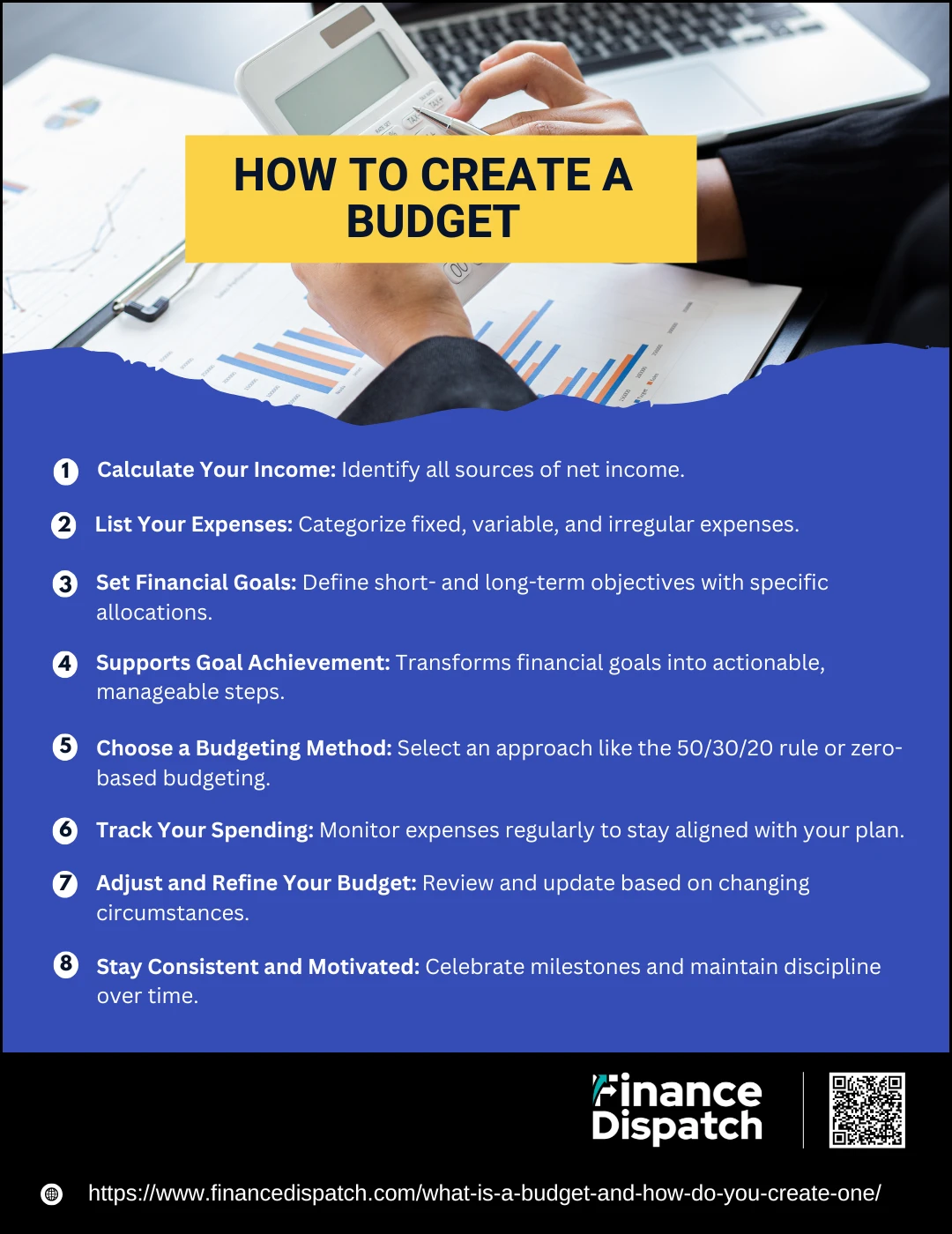

How to Create a Budget

How to Create a Budget

Creating a budget is an essential step toward achieving financial stability and reaching your goals. It’s not about restricting your spending but about taking control of your money and ensuring that every dollar is used wisely. A budget helps you understand your financial situation, prioritize expenses, and plan for the future. Here’s a step-by-step guide to creating a budget that works for you.

1. Calculate Your Income

Start by determining your total income. This includes all sources of money you receive regularly, such as your salary, freelance earnings, rental income, or government benefits. Focus on your net income—the amount left after taxes and deductions—since this represents the money you can actually spend.

2. List Your Expenses

Record all your monthly expenses and group them into categories. Fixed expenses like rent, mortgage, and insurance are consistent, while variable expenses like groceries, utilities, and entertainment can fluctuate. Don’t forget irregular expenses like annual subscriptions or car maintenance. Reviewing bank statements and receipts can help ensure accuracy.

3. Set Financial Goals

Define your short-term and long-term financial goals. Short-term goals might include building an emergency fund or paying off credit card debt, while long-term goals could involve saving for retirement or purchasing a home. Be specific about how much you need to allocate to these goals each month.

4. Create a Spending Plan

Compare your income with your expenses and goals to create a spending plan. Allocate specific amounts for each expense category, ensuring your total expenses and savings align with your income. This step helps you visualize how your money will be distributed throughout the month.

5. Choose a Budgeting Method

Decide on a budgeting method that suits your style and needs. Popular options include the 50/30/20 rule (50% for needs, 30% for wants, 20% for savings), the envelope system (cash-only for spending categories), or zero-based budgeting (assigning every dollar a purpose).

6. Track Your Spending

Monitor your expenses regularly to ensure they align with your budget. Use apps, spreadsheets, or a simple notebook to record every purchase. Tracking helps you identify areas where you might overspend and make adjustments as needed.

7. Adjust and Refine Your Budget

Life circumstances and expenses change, so it’s important to review your budget regularly. Reassess your spending habits, adjust for new expenses or income changes, and ensure your budget continues to support your financial goals effectively.

8. Stay Consistent and Motivated

Sticking to a budget takes time and discipline. Celebrate small wins, like meeting savings goals or cutting back on unnecessary expenses. Staying consistent with your budget will help you build financial habits that lead to long-term success.

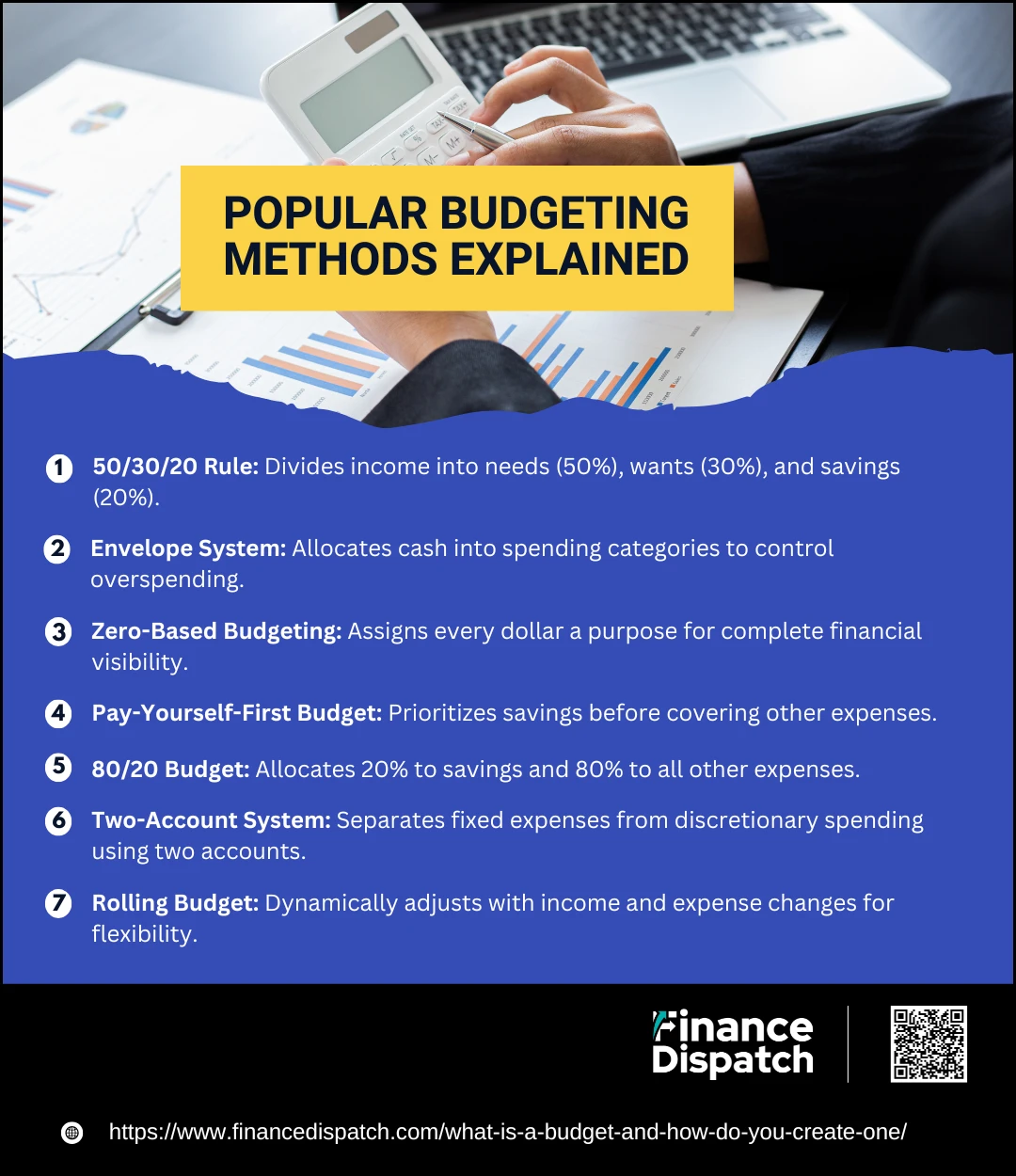

Popular Budgeting Methods Explained

Popular Budgeting Methods Explained

Budgeting is not one-size-fits-all. Different methods work for different people depending on their financial goals, spending habits, and lifestyle. Whether you’re aiming to save more, pay off debt, or manage irregular income, there’s a budgeting method that can help you succeed. Below are some of the most popular budgeting approaches, each with its unique benefits and features.

1. 50/30/20 Rule

This method simplifies budgeting by dividing your income into three categories: 50% for necessities (like rent and groceries), 30% for wants (like entertainment and dining out), and 20% for savings or debt repayment. It’s a straightforward approach ideal for those looking for a balanced way to manage money without tracking every expense.

2. Envelope System

In this cash-based method, you allocate money for each spending category (like groceries, utilities, or entertainment) into separate envelopes. Once the money in an envelope is spent, you can’t spend more in that category. This system is great for visualizing limits and controlling overspending.

3. Zero-Based Budgeting

With zero-based budgeting, every dollar of your income is assigned a specific purpose, ensuring that your income minus expenses equals zero. This detailed approach provides complete visibility into where your money is going and is excellent for people who prefer meticulous tracking.

4. Pay-Yourself-First Budget

This method prioritizes savings by setting aside a predetermined amount for savings and investments before paying for other expenses. It’s perfect for those focused on building wealth or creating a financial cushion without detailed expense tracking.

5. 80/20 Budget

This simplified method allocates 20% of your income toward savings and debt repayment, while the remaining 80% is for everything else, including necessities and discretionary spending. It’s a great option for people who prefer minimal structure.

6. Two-Account System

In this method, you separate your fixed expenses from discretionary spending by maintaining two bank accounts. One account is for fixed bills like rent and insurance, while the other is for flexible spending like dining and entertainment. It helps you avoid overspending on non-essentials.

7. Rolling Budget

A rolling budget adjusts dynamically as circumstances change, making it ideal for those with irregular incomes or fluctuating expenses. This method allows for flexibility, ensuring your budget remains relevant and accurate.

Common Budgeting Myths Debunked

Many people avoid budgeting because of misconceptions that make it seem restrictive, time-consuming, or unnecessary. However, these myths often prevent individuals from gaining control over their finances and achieving their goals. Budgeting isn’t about deprivation—it’s about empowerment. Let’s debunk some of the most common myths about budgeting to show why everyone can benefit from having a financial plan.

- “I Don’t Need a Budget If I Earn Enough”: Regardless of income level, budgeting helps track spending, plan for the future, and avoid unnecessary waste. Even high earners can benefit from a clear financial roadmap.

- “Budgeting is Too Restrictive”: A budget doesn’t mean cutting out all fun; it simply ensures you allocate money for both needs and wants while working toward goals.

- “I’m Bad at Math, So I Can’t Budget”: Modern budgeting tools, apps, and calculators make it easy to manage finances without complex calculations. Basic math skills are all you need.

- “Budgeting is Only for People in Debt”: While it helps manage debt, budgeting is a valuable tool for saving, investing, and preparing for unexpected expenses, even if you’re debt-free.

- “I Don’t Have Time to Budget”: Setting up a budget takes minimal effort with tools and apps that streamline the process. A few minutes of planning can save hours of stress later.

- “I’ll Feel Deprived if I Budget”: A good budget includes space for discretionary spending, allowing you to enjoy life while staying financially secure.

- “I Can’t Budget with an Irregular Income”: Budgeting with fluctuating income is possible by focusing on average earnings and prioritizing essential expenses and savings.

- “Budgeting is Too Complicated”: With simple methods like the 50/30/20 rule or envelope system, budgeting can be straightforward and tailored to your needs.

- “I Can’t Stick to a Budget”: Budgets are flexible and can be adjusted as circumstances change, making it easier to adapt and stay consistent over time.

- “Budgeting Isn’t Fun”: Watching your savings grow and achieving financial goals is incredibly rewarding, making budgeting a motivating and positive experience.

- “I Don’t Make Enough Money to Budget”: Budgeting is especially critical for those with limited income, as it helps maximize resources and prioritize essential expenses.

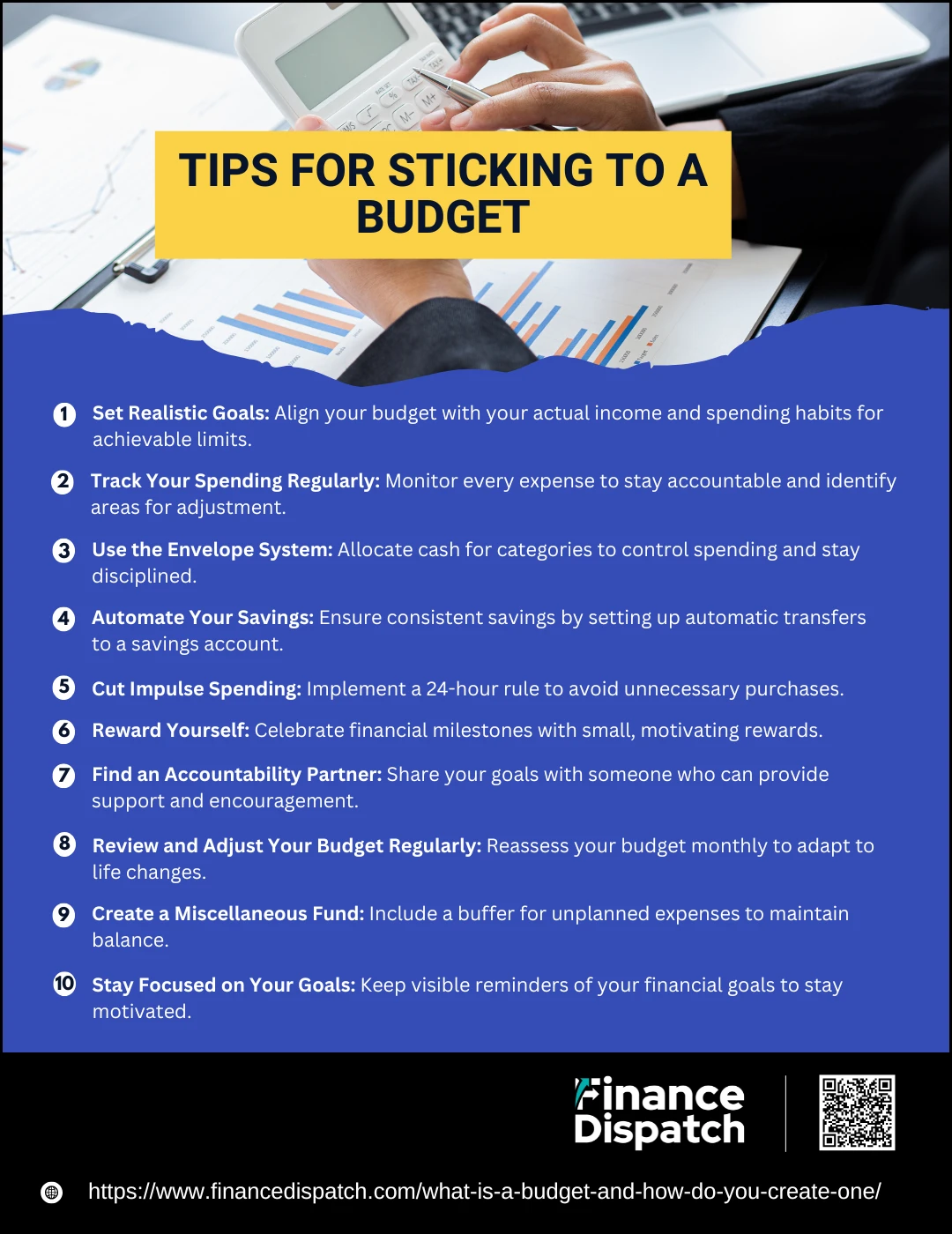

Tips for Sticking to a Budget

Tips for Sticking to a Budget

Creating a budget is only the first step toward financial success—sticking to it is where the real challenge lies. It’s easy to get derailed by unexpected expenses, impulsive purchases, or even a lack of motivation. However, a budget isn’t meant to restrict your lifestyle; it’s a tool to help you align your spending with your goals. By implementing practical strategies and making adjustments as needed, you can turn budgeting into a sustainable habit. Here are some detailed tips to help you stay on track and achieve financial stability.

1. Set Realistic Goals

Your budget should reflect your actual income and spending habits. Unrealistic goals, such as cutting all discretionary spending, can lead to frustration and failure. Instead, set achievable limits that allow you to balance saving, spending, and enjoying life.

2. Track Your Spending Regularly

Monitor where every dollar goes by using budgeting apps, a spreadsheet, or even a simple notebook. Tracking your expenses daily or weekly gives you a clear picture of your spending patterns and helps you identify areas to adjust.

3. Use the Envelope System

Assign cash to categories like groceries, entertainment, and dining out, and place the money in envelopes. This visual and tangible approach helps you stay disciplined—when the envelope is empty, spending for that category stops.

4. Automate Your Savings

Automatically transferring a portion of your income to a savings account ensures that saving becomes a priority, not an afterthought. Automation eliminates the temptation to skip saving and helps you stay consistent.

5. Cut Impulse Spending

Avoid buying non-essential items on a whim by implementing a 24-hour rule. This cooling-off period helps you determine if the purchase is truly necessary or just an impulsive desire.

6. Reward Yourself

Sticking to a budget can be challenging, so celebrate your successes along the way. Treat yourself to a small reward, like a coffee outing or movie night, after meeting a financial milestone. Rewards reinforce positive behavior and keep you motivated.

7. Find an Accountability Partner

Share your budget and financial goals with someone you trust, like a friend, partner, or family member. Regular check-ins with an accountability partner can keep you focused and provide encouragement during tough times.

8. Review and Adjust Your Budget Regularly

Budgets aren’t set in stone. Life changes, such as a raise, a new job, or an unexpected expense, may require adjustments. Reviewing your budget monthly ensures it remains relevant and effective in meeting your goals.

9. Create a Miscellaneous Fund

Include a small buffer in your budget for unexpected expenses, like a surprise birthday gift or a parking ticket. This flexibility prevents overspending in other categories and keeps your budget intact.

10. Stay Focused on Your Goals

Keep your financial goals visible, such as a picture of the vacation destination you’re saving for or a note about paying off debt. These reminders help you stay committed to your budget by reinforcing why you’re doing it.

Overcoming Budgeting Challenges

Sticking to a budget can be challenging, especially when life throws unexpected expenses or temptations your way. Common hurdles like fluctuating income, unplanned costs, or difficulty maintaining discipline can make it hard to stay on track. However, these obstacles are not insurmountable. The key to overcoming budgeting challenges lies in flexibility, consistency, and a proactive approach. Start by preparing for the unexpected with an emergency fund to cushion financial surprises. If your income varies, base your budget on your lowest monthly earnings to ensure stability. Regularly reviewing and adjusting your budget allows it to evolve with your needs and circumstances, while tracking every expense keeps you accountable. Embrace tools like budgeting apps to simplify the process and reduce manual effort. By facing challenges head-on and adapting to changes, you can turn your budget into a reliable roadmap for achieving your financial goals.

Conclusion

Budgeting is more than just a financial exercise—it’s a pathway to greater control, clarity, and confidence in your money management. While creating and sticking to a budget may present challenges, the rewards far outweigh the effort. A well-crafted budget empowers you to prioritize your spending, prepare for unexpected expenses, and work steadily toward your short-term and long-term goals. It’s not about restrictions but about making intentional decisions that align with your values and aspirations. By adopting practical strategies, staying consistent, and being flexible when life changes, you can transform budgeting into a lifelong habit that supports financial freedom and peace of mind. Remember, every small step toward managing your money better brings you closer to the future you envision.