When it comes to managing your financial health, few numbers are as important as your credit score. This three-digit number serves as a snapshot of your creditworthiness, influencing everything from loan approvals to interest rates, rental applications, and even job opportunities. Whether you’re planning to buy a home, finance a car, or apply for a credit card, your credit score plays a crucial role in determining the terms and conditions you’ll receive. But what exactly is a credit score, and why does it matter so much? In this article, we’ll break down how credit scores are calculated, why they impact your financial future, and the steps you can take to improve yours. Understanding your credit score is the first step toward making smarter financial decisions and securing better opportunities.

What is a Credit Score?

A credit score is a three-digit number that represents your creditworthiness, or how likely you are to repay borrowed money. Lenders, including banks, credit card companies, and mortgage providers, use this score to assess the risk of lending to you. Credit scores are calculated based on your credit history, which includes factors like payment history, total debt, length of credit history, types of credit used, and new credit applications. The most widely used credit scoring models are FICO® Score and VantageScore, both of which range from 300 to 850—with higher scores indicating better credit health. A good credit score can make it easier to qualify for loans, secure lower interest rates, and access better financial opportunities, while a poor score can lead to higher borrowing costs and loan denials.

Why Credit Scores Matter

Your credit score is more than just a number—it’s a financial tool that can significantly impact your life. Whether you’re applying for a mortgage, financing a car, or even securing a job, your credit score plays a crucial role in determining your eligibility and the terms you receive. A higher score indicates responsible financial behavior and makes you a lower-risk borrower, leading to better loan offers and lower interest rates. On the other hand, a poor credit score can limit your financial opportunities, making it harder to borrow money, rent a home, or even get affordable insurance. Understanding the importance of credit scores can help you make informed financial decisions and build a secure financial future.

Why Your Credit Score is Important:

Why Your Credit Score is Important:

1. Loan Approvals & Interest Rates

Lenders use your credit score to decide whether to approve your loan applications and what interest rates to offer. A higher score means lower interest rates, which can save you thousands of dollars over time. A lower score may result in higher borrowing costs or outright denials.

2. Credit Card Benefits

A good credit score can unlock credit cards with better rewards, higher limits, and lower interest rates. In contrast, individuals with poor credit may only qualify for high-interest credit cards with strict terms.

3. Renting a Home

Many landlords check credit scores before renting out apartments or houses. A strong credit score increases your chances of approval, while a poor score may require you to pay a larger security deposit or provide a co-signer.

4. Employment Considerations

Some employers, especially in financial sectors, review credit history as part of the hiring process. A poor credit score may indicate financial instability, which can be a concern for roles requiring financial responsibility.

5. Insurance Premiums

Auto and home insurance providers often use credit scores to determine insurance rates. A lower score may lead to higher premiums, while a good credit score can help you qualify for discounts.

6. Utility & Cell Phone Services

Utility companies and mobile carriers may check credit scores before approving service contracts. A low score may require a security deposit or limit your options for postpaid plans.

How Credit Scores Are Calculated

Your credit score is determined by various factors that reflect your financial behavior and credit management. Lenders rely on these scores to assess how responsibly you handle credit and whether you’re a reliable borrower. The two most commonly used credit scoring models, FICO® Score and VantageScore, use different formulas, but both consider similar factors such as payment history, credit utilization, and the length of your credit history. Understanding how these elements contribute to your score can help you take steps to improve it and maintain a strong financial standing.

Key Factors in Credit Score Calculation

| Factor | FICO Score Weight | VantageScore Weight | Description |

| Payment History | 35% | 40% | Timely payments on loans and credit cards significantly impact your score. Late or missed payments can lower it. |

| Credit Utilization | 30% | 20% | The ratio of your outstanding credit card balances to your total credit limit. Lower utilization (below 30%) is better. |

| Length of Credit History | 15% | 21% | A longer credit history demonstrates financial stability and responsible credit management. |

| New Credit Inquiries | 10% | 5% | Applying for multiple new credit accounts in a short period can negatively affect your score. |

| Credit Mix | 10% | 11% | Having a diverse mix of credit accounts, such as credit cards, auto loans, and mortgages, shows responsible credit handling. |

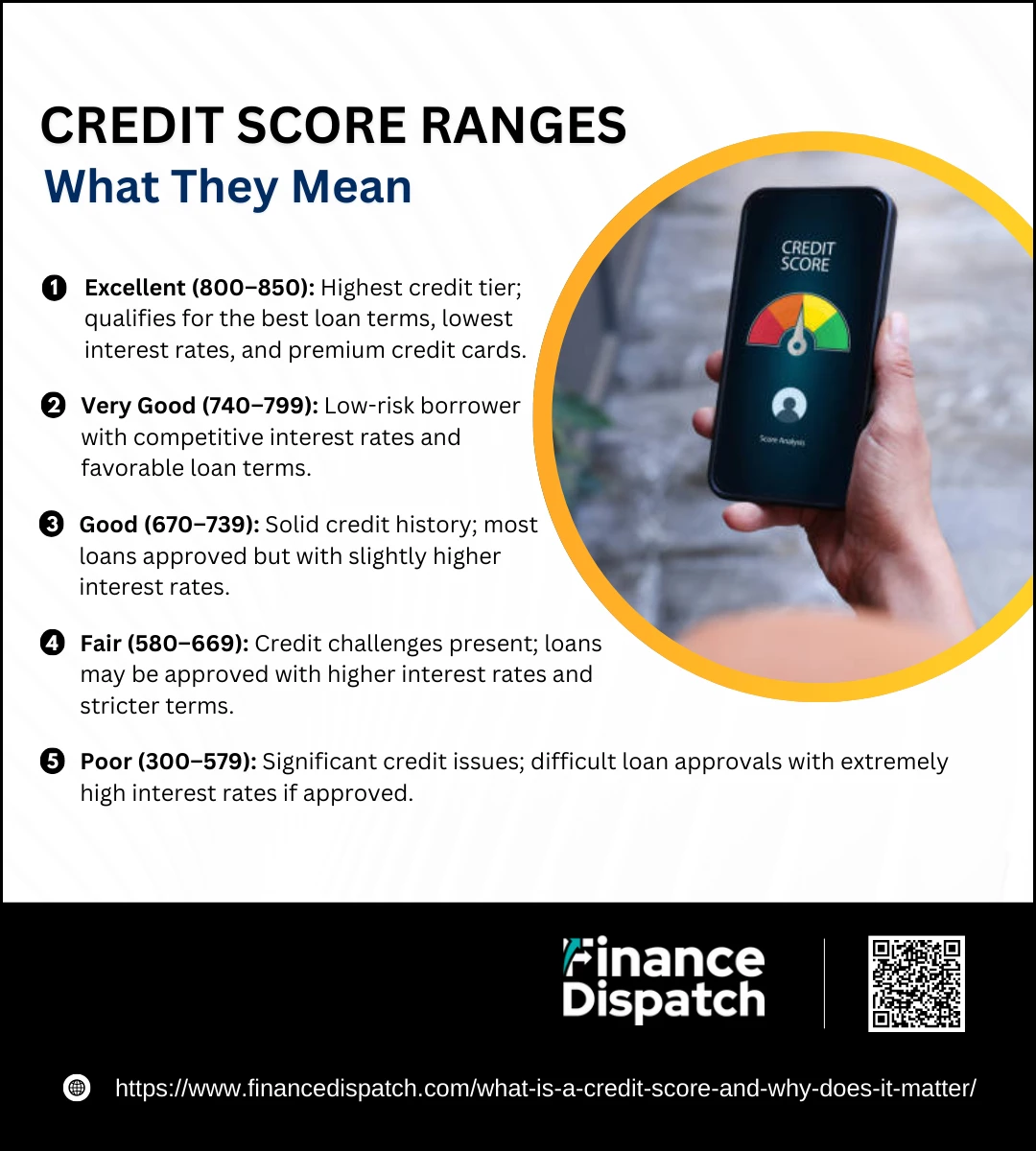

Credit Score Ranges & What They Mean

Credit Score Ranges & What They Mean

Your credit score is a numerical representation of your creditworthiness, and it falls within a specific range that lenders use to assess risk. Whether you’re applying for a loan, credit card, or mortgage, your score determines the terms and interest rates you receive. Higher scores indicate responsible credit behavior and make borrowing easier, while lower scores may lead to higher interest rates or loan denials. Credit scores typically range from 300 to 850 under the FICO® and VantageScore models, with different categories defining what is considered poor, fair, good, or excellent credit. Understanding these ranges can help you set financial goals and improve your credit standing over time.

Credit Score Categories & Their Meaning

1. Excellent (800–850)

This is the highest credit tier, indicating exceptional credit management. Borrowers in this range qualify for the best loan terms, lowest interest rates, and premium credit card offers.

2. Very Good (740–799)

A very good credit score means you’re a low-risk borrower. You’ll have access to competitive interest rates and favorable loan terms, though not always the absolute best rates.

3. Good (670–739)

Falling within this range means you have a solid credit history. Most lenders will approve your applications, but your interest rates might be slightly higher than those with excellent credit.

4. Fair (580–669)

This range suggests some credit challenges, such as late payments or high credit utilization. You may still qualify for loans, but at higher interest rates and with stricter terms.

5. Poor (300–579)

A score in this range indicates significant credit issues, such as missed payments, high debt levels, or even bankruptcy. Borrowers with poor credit may struggle to get approved for loans and may face extremely high interest rates if approved.

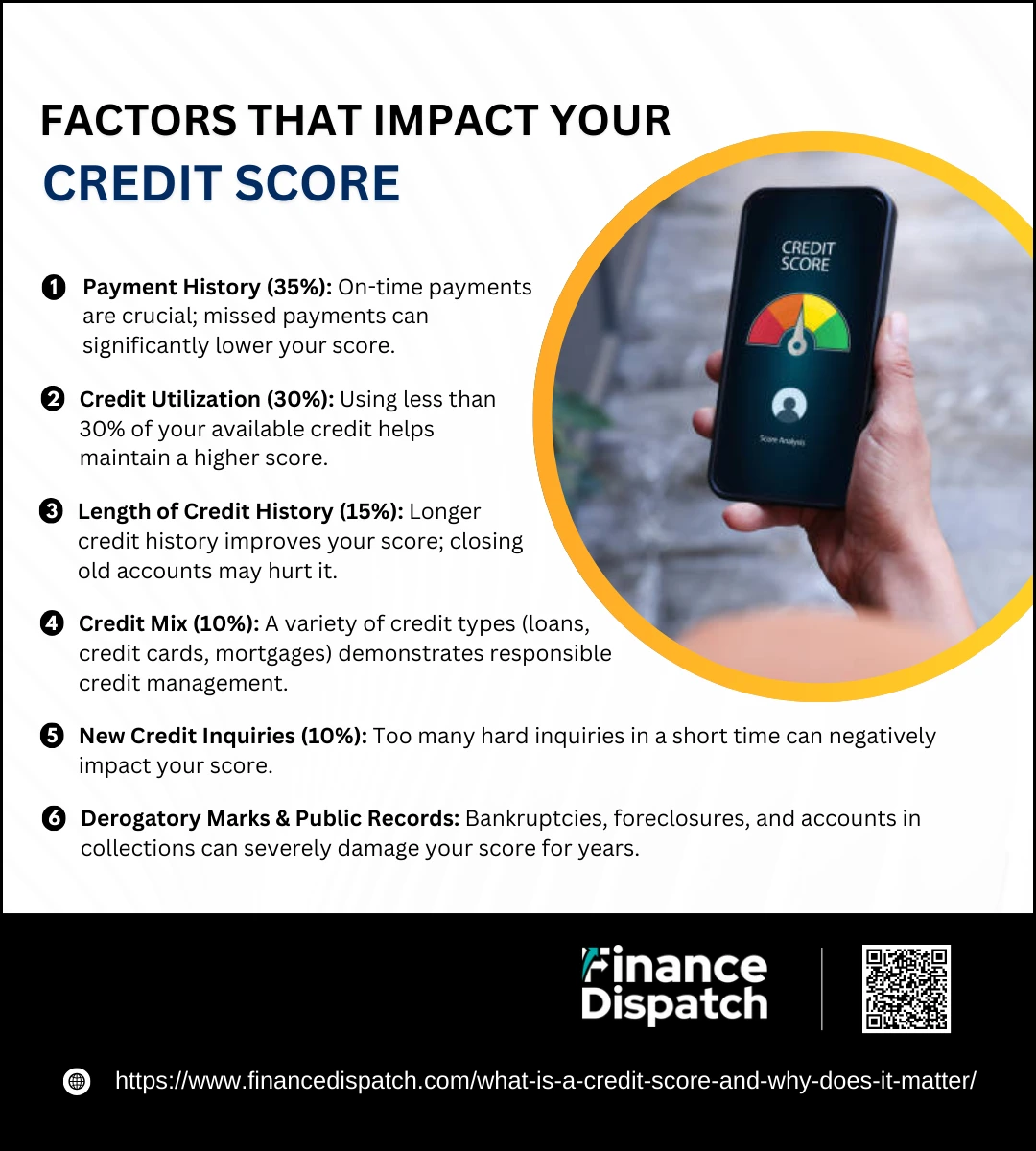

Factors That Impact Your Credit Score

Factors That Impact Your Credit Score

Your credit score is influenced by several key factors that reflect how well you manage credit and debt. Lenders use these factors to determine whether you’re a reliable borrower and what terms to offer you. While different scoring models, such as FICO® Score and VantageScore, may weigh these factors slightly differently, they all focus on similar aspects of your credit history. Understanding these elements can help you take control of your financial health and improve your credit score over time.

Key Factors That Impact Your Credit Score

1. Payment History (35%)

This is the most important factor in your credit score. Lenders want to see a consistent record of on-time payments for credit cards, loans, and other financial obligations. Missed or late payments can significantly lower your score.

2. Credit Utilization (30%)

This refers to how much of your available credit you’re using. Keeping your credit utilization below 30% is ideal, as maxing out your credit cards can negatively impact your score.

3. Length of Credit History (15%)

The longer your credit history, the better. Lenders prefer borrowers with long-standing credit accounts because it provides a more comprehensive view of their financial behavior. Closing old accounts may shorten your credit history and lower your score.

4. Credit Mix (10%)

A diverse mix of credit types, such as credit cards, auto loans, mortgages, and personal loans, shows lenders that you can manage different types of credit responsibly.

5. New Credit Inquiries (10%)

Applying for multiple new credit accounts in a short period can negatively affect your score. Each hard inquiry (when a lender checks your credit report for a new loan or credit card) can lower your score slightly.

6. Derogatory Marks & Public Records

Issues such as bankruptcies, foreclosures, accounts in collections, or charge-offs can have a severe negative impact on your credit score. These remain on your credit report for several years, making it difficult to secure new credit.

How to Check Your Credit Score

How to Check Your Credit Score

Knowing your credit score is an essential step in managing your financial health. Your credit score determines your ability to secure loans, credit cards, and even rental agreements. Checking your score regularly helps you track your progress, identify potential errors, and take proactive steps to improve it. Fortunately, there are several ways to check your credit score for free without negatively impacting it. Here’s how you can access your credit score and stay informed about your financial standing.

Ways to Check Your Credit Score:

1. Credit Bureaus (Equifax, Experian, TransUnion)

The three major credit bureaus maintain records of your credit history and provide credit scores based on their data. Since each bureau may have slightly different information, your score might vary between them. You can request your score directly from these bureaus, though some may charge a small fee.

2. AnnualCreditReport.com (Official Free Report)

U.S. consumers are entitled to one free credit report per year from each of the three major credit bureaus via AnnualCreditReport.com. While this report contains all your credit details, it does not always include your credit score. Some bureaus offer the option to purchase your score separately.

3. Credit Card Issuers & Banks

Many financial institutions provide free credit score access as part of their online banking services. If you have a credit card or an account with a major bank, check their website or mobile app to see if they offer this feature. Banks often use FICO® Scores or VantageScore models to display your credit score.

4. Credit Monitoring Services

Platforms like Credit Karma, NerdWallet, and Credit Sesame offer free access to your credit score and credit reports. These services also provide insights into how your financial habits affect your score, suggest ways to improve it, and alert you to any unusual activity.

5. Loan & Mortgage Lenders

If you apply for a mortgage or auto loan, lenders typically provide your FICO® Score as part of the approval process. While this is not a way to check your score regularly, it can give you an accurate picture of your standing before making major financial decisions.

6. Financial Advisors & Credit Counselors

Some financial advisors and nonprofit credit counseling agencies offer free credit report reviews to help you understand your credit score and suggest ways to improve it. If you’re struggling with debt or need financial guidance, these professionals can be valuable resources.

Myths and Misconceptions about Credit Scores

Credit scores are often misunderstood, leading to myths that can cause people to make poor financial decisions. Many believe that checking their credit score will lower it, that closing old accounts improves their score, or that married couples share a credit score. These misconceptions can prevent individuals from taking the right steps to improve their financial health. Understanding the truth behind these myths is essential for making informed financial choices and maintaining a strong credit profile. Below are some of the most common myths about credit scores, debunked.

Common Myths about Credit Scores

- Myth #1: Checking Your Credit Score Lowers It

Fact: Checking your own credit score is a soft inquiry and does not affect your credit. Only hard inquiries, such as applying for a new loan or credit card, can temporarily lower your score. - Myth #2: Closing Old Credit Accounts Helps Your Score

Fact: Closing old accounts can reduce your credit history length and increase your credit utilization, both of which can negatively impact your score. Instead, keep old accounts open to maintain a longer credit history. - Myth #3: You Need to Carry a Balance to Build Credit

Fact: Carrying a balance on your credit card does not improve your score. Paying off your full balance each month is actually the best way to maintain a high credit score while avoiding interest charges. - Myth #4: Married Couples Have a Shared Credit Score

Fact: Each person has their own individual credit score. While joint accounts and shared debts can impact both spouses’ credit, their scores remain separate. - Myth #5: All Credit Scores Are the Same

Fact: There are multiple credit scoring models, including FICO® Score and VantageScore, and each credit bureau (Equifax, Experian, TransUnion) may have slightly different information. Your score may vary depending on which model and bureau is used. - Myth #6: Employers Can See Your Credit Score

Fact: Employers cannot check your credit score, but they may request a credit report (without your score) as part of background checks, especially for financial positions. - Myth #7: A Higher Income Means a Higher Credit Score

Fact: Your income is not a factor in your credit score. Your score is based on your credit history, including payment history, credit utilization, and length of credit history. - Myth #8: You Can Instantly Improve Your Credit Score

Fact: Building or repairing your credit takes time. While paying off debt and making timely payments help, credit scores update gradually based on your financial behavior.

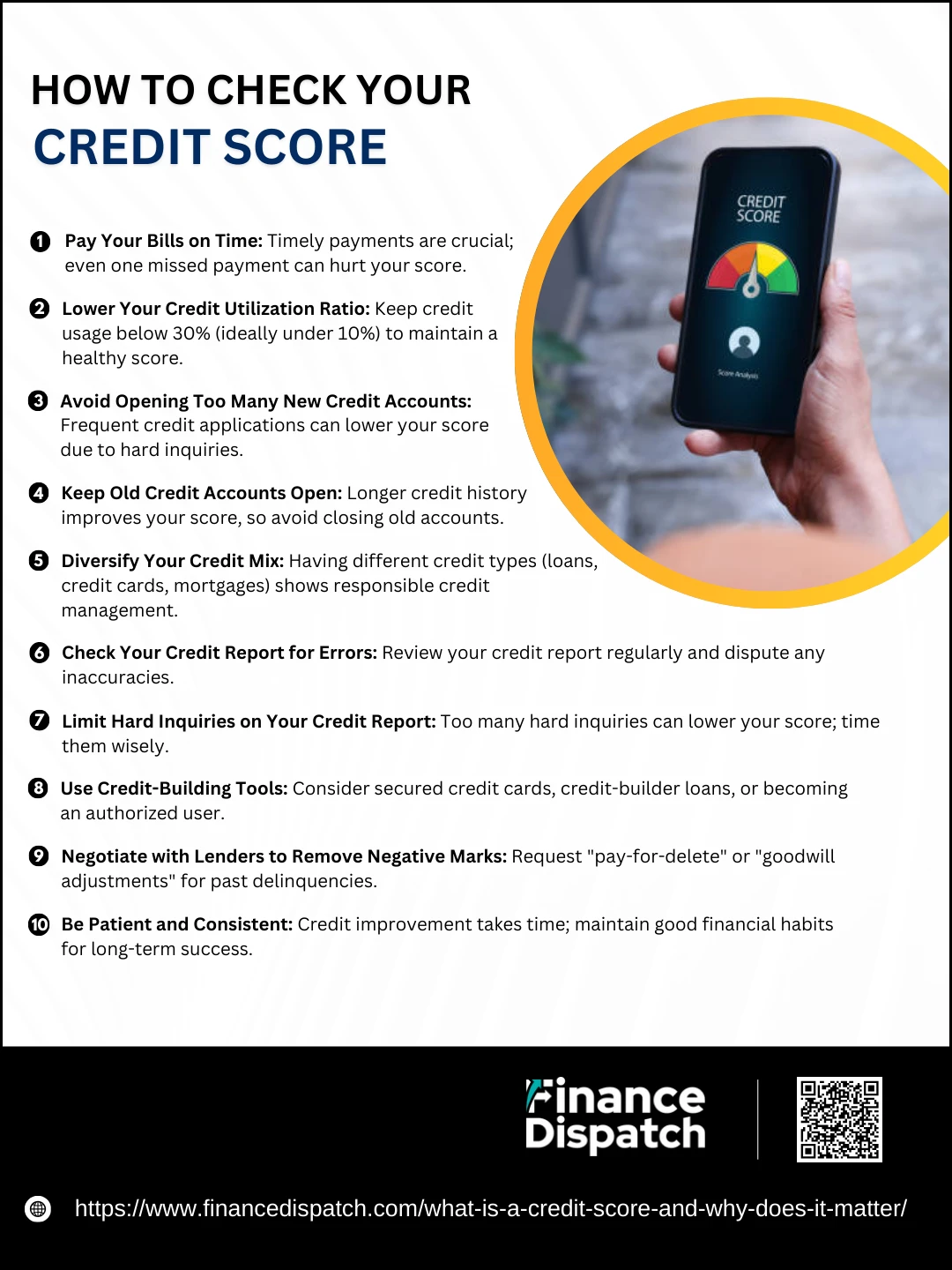

How to Improve Your Credit Score

How to Improve Your Credit Score

Your credit score is a key factor in determining your financial opportunities, including loan approvals, interest rates, and credit card offers. A higher credit score can save you money and provide better financial stability, while a lower score can make borrowing more expensive or even lead to loan denials. If your score isn’t where you want it to be, don’t worry—there are proven steps you can take to improve it. By making smart financial choices and developing good credit habits, you can gradually boost your credit score and strengthen your financial future.

Steps to Improve Your Credit Score

1. Pay Your Bills on Time

Payment history is the most significant factor affecting your credit score. Make sure to pay all your bills—credit cards, loans, utilities, and rent—on time every month. Even one missed payment can have a negative impact.

2. Lower Your Credit Utilization Ratio

Keep your credit utilization (the percentage of your available credit that you’re using) below 30%, and ideally under 10%. Paying down your credit card balances and avoiding maxing out your cards can help boost your score.

3. Avoid Opening Too Many New Credit Accounts

Every time you apply for new credit, a hard inquiry appears on your credit report, which can slightly lower your score. Avoid applying for multiple credit cards or loans within a short period unless absolutely necessary.

4. Keep Old Credit Accounts Open

The length of your credit history matters, so avoid closing old credit card accounts, even if you don’t use them frequently. Keeping older accounts open can help maintain a longer credit history, which positively affects your score.

5. Diversify Your Credit Mix

Having a mix of credit types—such as credit cards, auto loans, and mortgages—demonstrates responsible credit management. However, don’t open new accounts just to improve your credit mix.

6. Check Your Credit Report for Errors

Obtain a free credit report from AnnualCreditReport.com and review it for inaccuracies. If you find incorrect late payments, accounts that don’t belong to you, or outdated information, dispute them with the credit bureaus to get them corrected.

7. Limit Hard Inquiries on Your Credit Report

Hard inquiries occur when lenders check your credit for loan or credit card applications. Too many inquiries in a short period can lower your score. If you’re shopping for a mortgage or car loan, try to keep applications within a 14-day window, as they may be treated as a single inquiry.

8. Use Credit-Building Tools

If you have a limited or poor credit history, consider using tools like secured credit cards, credit-builder loans, or authorized user status on a responsible family member’s credit card to improve your score.

9. Negotiate with Lenders to Remove Negative Marks

If you’ve had late payments or collections, you may be able to negotiate a “pay-for-delete” agreement with creditors or request a “goodwill adjustment” to remove negative marks from your credit report.

10. Be Patient and Consistent

Credit improvement doesn’t happen overnight. It takes time to rebuild a strong credit history. Focus on maintaining good financial habits, and over time, you’ll see positive changes in your score.

Conclusion

Your credit score is a powerful financial tool that influences your ability to borrow money, secure favorable interest rates, and access various financial opportunities. Maintaining a strong credit score requires responsible financial habits, such as paying bills on time, keeping credit utilization low, and monitoring your credit report for errors. While improving your credit score takes time, consistency in managing debt and making informed financial decisions can lead to long-term benefits. A good credit score not only saves you money on loans and credit cards but also enhances your financial stability and opens doors to better housing, job opportunities, and lower insurance premiums. By understanding how credit scores work and taking proactive steps to improve yours, you can build a healthier financial future with greater financial freedom and security.