Economic ups and downs are a natural part of life, but when the word “recession” makes the headlines, it often sparks worry about jobs, savings, and day-to-day living costs. A recession simply means the economy is slowing down—businesses may earn less, people may spend more cautiously, and unemployment can rise. While that sounds unsettling, the good news is that recessions don’t last forever, and with the right preparation, you can protect yourself and your family from financial strain. By understanding what a recession is and taking a few smart steps now, you can build resilience, reduce stress, and feel more confident about your financial future.

What is a Recession?

A recession is a period when the economy slows down for several months, often marked by falling Gross Domestic Product (GDP), rising unemployment, and reduced consumer spending. In simple terms, it means businesses are producing and selling less, people may lose jobs or cut back on purchases, and overall economic activity declines. Unlike depressions, which are much deeper and longer-lasting, recessions are usually temporary and part of the normal economic cycle. While they can feel disruptive, understanding that they are a recurring phase of growth and slowdown can help you prepare with more confidence.

Signs and Causes of a Recession

Recessions are rarely sudden; they usually develop as the economy shows signs of slowing down. Recognizing these signals early can help individuals and businesses make smarter financial choices. Here are some of the most common indicators and causes:

Common Signs and Causes of a Recession:

1. Falling Gross Domestic Product (GDP): When the total value of goods and services produced in the economy declines for two or more consecutive quarters, it often signals a recession.

2. Rising Unemployment: As businesses see lower demand, they may reduce their workforce, leading to job losses and higher unemployment rates.

3. High Inflation: Rapidly increasing prices make essentials like food, gas, and housing more expensive, straining household budgets and reducing overall spending power.

4. Higher Interest Rates: Central banks sometimes raise rates to fight inflation, but this also makes borrowing for mortgages, loans, or business investments more costly, slowing economic growth.

5. Decline in Consumer Confidence: When people fear losing jobs or worry about rising prices, they cut back on spending, which reduces demand and further weakens the economy.

6. Global Shocks: Unexpected events such as wars, pandemics, or supply chain disruptions can create uncertainty and push economies into recession.

7. Stock Market Volatility: Sharp or prolonged declines in the market often reflect reduced investor confidence, which can impact retirement savings, investments, and corporate growth.

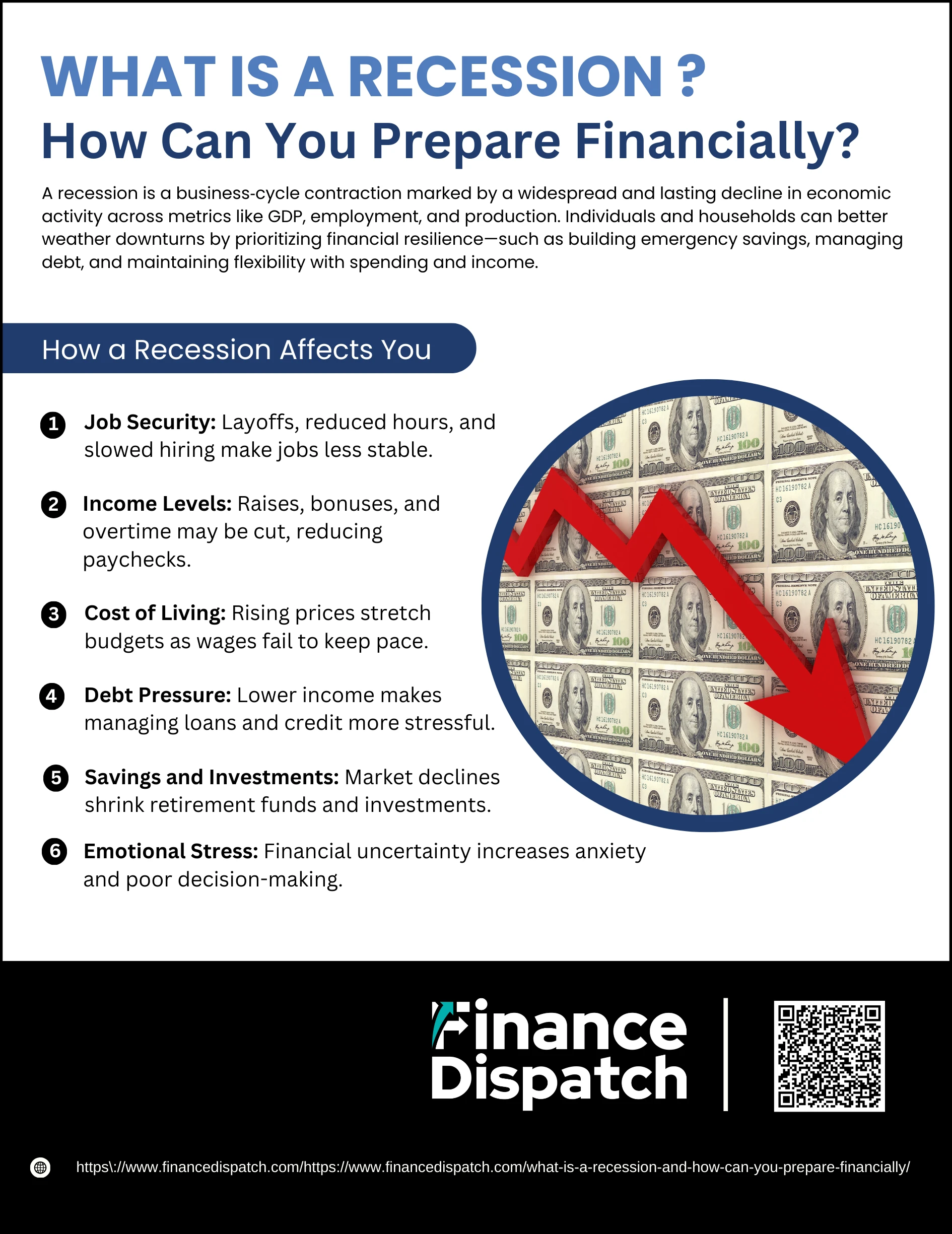

How a Recession Affects You

How a Recession Affects You

A recession isn’t just an abstract economic term—it has real consequences that can affect your day-to-day life. From the stability of your job to the value of your savings, the impacts can be wide-ranging. By understanding these effects, you can take proactive steps to protect your financial well-being.

Key Ways a Recession Can Affect You:

1. Job Security

During a recession, businesses often experience reduced demand for their products or services. To cut costs, they may slow down hiring, reduce work hours, or lay off employees. Industries like retail, travel, or construction are often hit harder than essential services such as healthcare or utilities. This uncertainty can leave many workers feeling vulnerable about their careers.

2. Income Levels

Even if you remain employed, you may notice changes in your paycheck. Employers sometimes pause annual raises, cut bonuses, or reduce overtime opportunities. This can lead to smaller take-home pay at a time when everyday expenses may be rising, making it harder to save or invest.

3. Cost of Living

Recessions can go hand-in-hand with inflation, which pushes up the prices of necessities like groceries, gas, and rent. When wages don’t rise at the same pace, your money doesn’t stretch as far, forcing you to make tougher choices about how to spend.

4. Debt Pressure

Debt can feel especially heavy during a downturn. With less income coming in, meeting fixed obligations like mortgages, student loans, or credit card payments becomes more stressful. Missing payments can hurt your credit score, making it harder or more expensive to borrow in the future.

5. Savings and Investments

Financial markets usually decline during recessions, which can reduce the value of retirement accounts, stocks, and other investments. While these losses are often temporary, they can be unsettling—especially if you’re nearing retirement or rely on those funds for future plans.

6. Emotional Stress

Beyond the financial impact, recessions can take a toll on mental health. Anxiety about losing a job, paying bills, or watching investments shrink can lead to emotional decision-making, such as panic-selling investments or overspending out of stress. Staying calm and focusing on long-term goals becomes more important than ever.

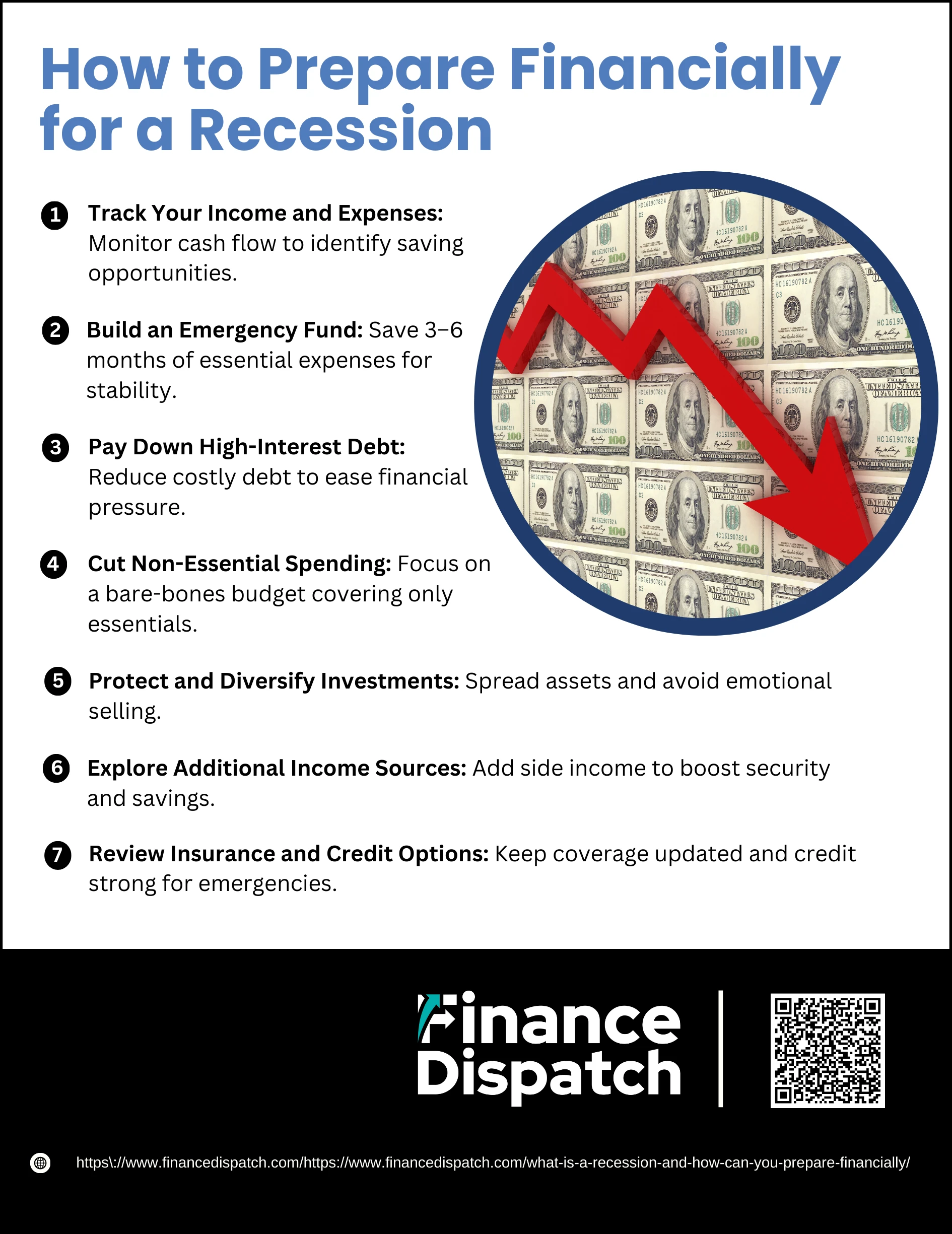

How to Prepare Financially for a Recession

How to Prepare Financially for a Recession

No one can control the economy, but you can control how prepared you are when times get tough. A recession often brings uncertainty—lost jobs, tighter budgets, and unstable markets—but taking smart steps today can reduce stress and keep you financially steady. Here are key strategies to help you safeguard your money.

Steps to Prepare for a Recession:

1. Track Your Income and Expenses

Begin by examining your cash flow—how much comes in versus how much goes out. Break expenses into categories like housing, food, transportation, debt payments, and extras. A clear view of your finances helps you see where you can adjust, cut back, or save more. Tools like budgeting apps, spreadsheets, or even a simple notebook can keep you accountable.

2. Build an Emergency Fund

An emergency fund acts as your financial safety net. Ideally, save enough to cover three to six months of essential living costs. This way, if you lose a job or face sudden bills, you won’t have to rely on high-interest credit cards. Start small if you need to—even $20 or $50 set aside regularly adds up over time.

3. Pay Down High-Interest Debt

Debt becomes more stressful during a downturn because monthly payments don’t pause when income does. Focus first on high-interest debt like credit cards or payday loans. Reducing these balances lowers your financial obligations and frees up money for more important needs. You might also explore refinancing or consolidating loans to lock in a lower rate.

4. Cut Non-Essential Spending

Look closely at your budget and ask yourself what’s truly necessary. Subscriptions, dining out, luxury shopping, and entertainment are areas you may be able to trim. Creating a “bare-bones budget” focused on essentials like rent, food, healthcare, and utilities ensures you can stretch your money further during hard times.

5. Protect and Diversify Investments

Market volatility can tempt people to panic-sell, but history shows markets eventually recover. Instead of making emotional decisions, check whether your portfolio is diversified across different asset types—stocks, bonds, and cash equivalents. If you’re close to retirement, consider adjusting to safer investments. Long-term investors, on the other hand, may even see downturns as buying opportunities.

6. Explore Additional Income Sources

Relying on a single paycheck is riskier in a recession. Consider ways to add income, such as freelancing, consulting, tutoring, or selling unused items online. Even part-time or gig work can help bridge financial gaps, boost savings, and give you peace of mind. Upskilling—taking online courses or certifications—can also make you more competitive if layoffs occur.

7. Review Insurance and Credit Options

Make sure your health, home, and life insurance policies are updated to protect you from unexpected costs. At the same time, keep your credit score strong by paying bills on time and keeping balances low. Good credit gives you better access to emergency loans or lower-interest financing if you ever need it.

Common Mistakes to Avoid in Recession

When money feels tight and uncertainty looms, it’s easy to make quick decisions that may hurt your financial future. Recessions create stress, but avoiding certain common mistakes can save you from added hardship. By staying calm and making thoughtful choices, you’ll be better positioned to weather the downturn.

1. Panic-Selling Investments: Selling when markets dip locks in losses and prevents you from benefiting when they recover.

2. Relying Too Heavily on Credit Cards: Using high-interest credit for daily expenses can trap you in long-term debt.

3. Draining Retirement Accounts Early: Cashing out retirement savings can trigger taxes, penalties, and reduce future growth.

4. Making Big Purchases Without Necessity: Buying cars, luxury items, or taking on new loans adds financial pressure when stability matters most.

5. Ignoring Your Budget: Failing to adjust spending during a recession can drain savings faster than expected.

6. Neglecting Insurance Coverage: Canceling or reducing insurance to save money may leave you exposed to costly emergencies.

7. Avoiding Professional Advice: Skipping guidance from financial planners can cause you to overlook safer options for managing money and investments.

Maintaining a Strong Financial Mindset

A recession doesn’t just challenge your wallet—it also tests your mindset. Fear and stress can lead to hasty decisions that do more harm than good. Building resilience and staying focused on long-term goals can help you manage both your money and your emotions during uncertain times.

Ways to Maintain a Strong Financial Mindset:

1. Stay Calm and Avoid Panic: Market dips and job concerns are temporary; remind yourself that recessions eventually pass.

2. Focus on Long-Term Goals: Keep your retirement, savings, and investment objectives in view rather than reacting to short-term setbacks.

3. Practice Mindfulness: Simple habits like journaling, meditation, or breathing exercises can reduce stress and keep you grounded.

4. Limit Negative News Consumption: Constantly checking headlines can increase anxiety; choose reliable updates and avoid information overload.

5. Celebrate Small Wins: Whether it’s paying down a bit of debt or saving an extra $50, acknowledging progress helps you stay motivated.

6. Seek Support if Needed: Talking with a financial advisor, mentor, or supportive friends and family can provide guidance and reassurance.

Conclusion

Recessions may be an inevitable part of the economic cycle, but they don’t have to derail your financial well-being. By understanding what a recession is, recognizing the warning signs, and taking proactive steps—like budgeting wisely, building savings, and avoiding common mistakes—you can protect yourself and your family from unnecessary stress. Most importantly, remember that recessions are temporary. With preparation, patience, and a strong financial mindset, you’ll not only make it through tough times but also be in a better position to thrive when the economy recovers.