A tax levy is one of the most serious actions the government can take to collect unpaid taxes. Unlike a tax lien, which is a claim on your property, a tax levy involves the actual legal seizure of your assets—such as wages, bank accounts, or property—to satisfy a tax debt. Understanding how tax levies work, what triggers them, and how they can lead to asset seizure is essential for anyone facing IRS collection actions. In this article, we’ll break down the tax levy process and explain how to prevent or resolve it before it significantly disrupts your financial life.

What Is a Tax Levy?

A tax levy is a legal action taken by the Internal Revenue Service (IRS) or a state taxing authority to seize a taxpayer’s property in order to satisfy unpaid tax debt. It is not merely a warning or claim like a tax lien; instead, it is the actual enforcement of that claim, allowing the government to take ownership of your wages, bank accounts, real estate, vehicles, or other assets. Tax levies are typically used as a last resort after repeated notices and demands for payment have gone unanswered. Once a levy is in place, it can severely impact your finances and access to essential resources, making it crucial to address any tax issues before enforcement begins.

Tax Levy vs. Tax Lien

A tax levy and a tax lien are both tools used by the IRS to collect unpaid taxes, but they serve different purposes and occur at different stages of the collection process. A tax lien is a public notice that the government has a legal claim against your property due to unpaid tax debt, while a tax levy is the actual act of seizing that property to satisfy the debt. Understanding the distinction between the two can help taxpayers take timely action to avoid more severe consequences.

Here’s a quick comparison:

| Feature | Tax Lien | Tax Levy |

| Definition | Legal claim against property for unpaid taxes | Legal seizure of property to satisfy tax debt |

| Action | Notifies creditors of government’s claim | Government takes and sells property |

| Impact on Credit | Can affect credit score | Does not appear on credit report directly |

| Public Record | Yes | No |

| Timing | Filed before levy is issued | Issued after lien and multiple payment notices |

| Resolution | Removed after debt is paid or settled | Stopped by paying debt, appeal, or hardship claim |

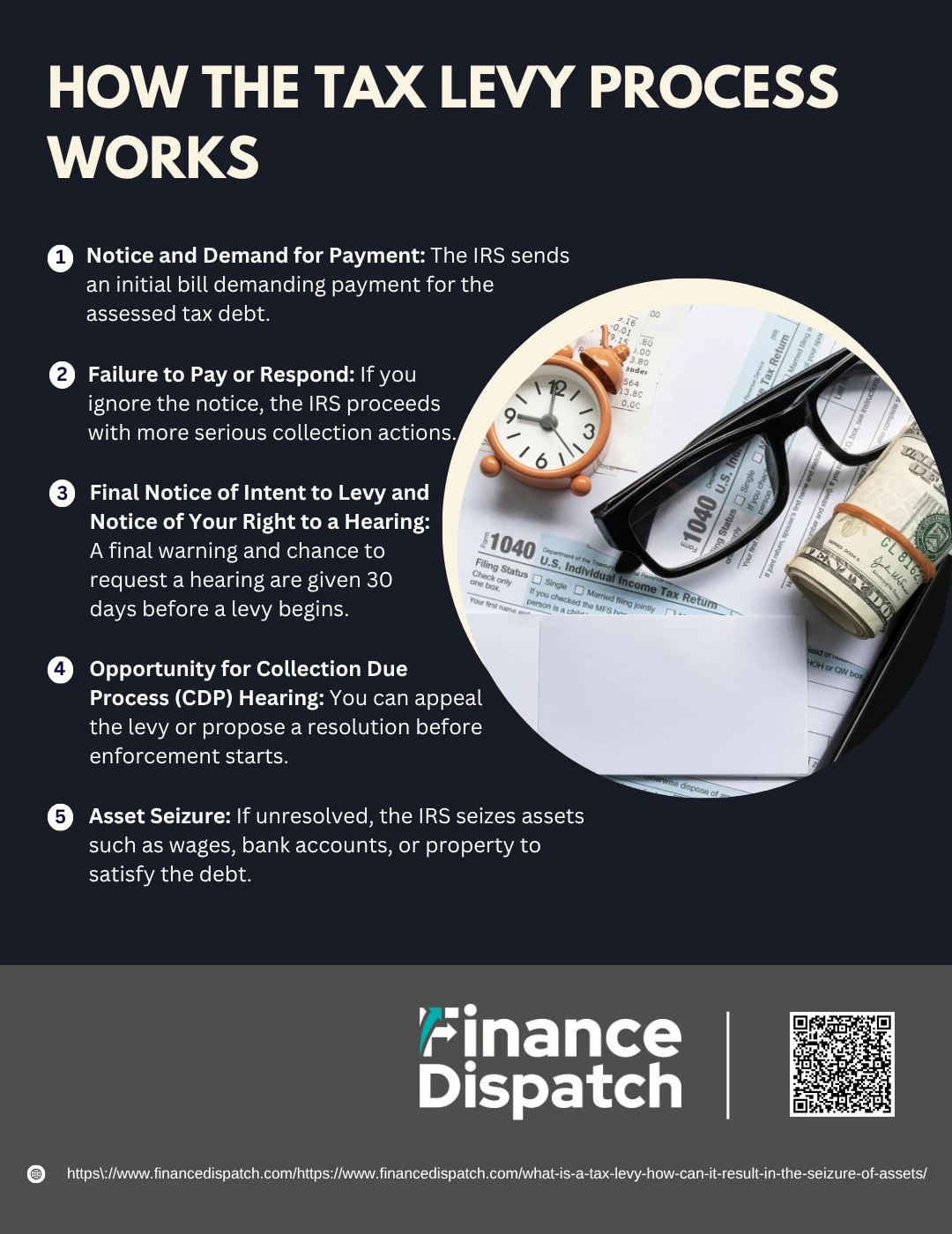

How the Tax Levy Process Works

How the Tax Levy Process Works

The tax levy process is a methodical enforcement action the IRS takes when a taxpayer neglects or refuses to pay an outstanding tax debt. Unlike a sudden action, this process includes a series of legally required steps designed to inform and give the taxpayer multiple chances to comply. The IRS typically uses a levy only after it has made repeated attempts to collect the debt voluntarily. If these efforts are ignored, the IRS can move forward with seizing wages, bank accounts, real estate, or other assets to cover the owed taxes. Understanding each stage of the process can help you avoid the severe consequences of enforced collections.

Here’s a closer look at how the tax levy process unfolds:

1. Notice and Demand for Payment

The IRS starts by assessing the amount you owe and sending a formal bill called the “Notice and Demand for Payment.” This notice outlines your total tax debt and requests full payment within a certain timeframe.

2. Failure to Pay or Respond

If you do not respond to the initial notice or fail to pay the amount due, the IRS continues its collection efforts. Ignoring this notice sets the stage for more aggressive actions.

3. Final Notice of Intent to Levy and Notice of Your Right to a Hearing

Before the IRS can legally seize any property, it must send you a “Final Notice of Intent to Levy” and “Notice of Your Right to a Hearing.” These are sent at least 30 days before any action is taken and provide you with a final opportunity to respond or appeal.

4. Opportunity for Collection Due Process (CDP) Hearing

You have the right to request a CDP hearing within 30 days of receiving the final notice. This hearing allows you to dispute the debt, propose a payment plan, or explore alternative resolutions like an Offer in Compromise before any levy is enforced.

5. Asset Seizure

If no payment is made and no appeal is filed within the allowed period, the IRS can move forward with seizing your assets. This may include garnishing wages, freezing bank accounts, or taking physical property. The seized assets are then sold, and the proceeds are used to pay down your tax debt.

What Assets Can Be Seized Under a Tax Levy?

What Assets Can Be Seized Under a Tax Levy?

When the IRS initiates a tax levy due to unpaid tax debt, it doesn’t just target one asset—it has the power to seize a broad range of property to recover what’s owed. These levies can severely impact your daily life, financial stability, and even your ability to run a business. The IRS generally targets the most accessible or valuable assets first, and while some items are exempt by law, many forms of income and property are fair game. It’s important to act quickly when you receive notices, because once the IRS begins the levy process, the consequences can be difficult—and sometimes impossible—to reverse.

Below is a more detailed look at the types of assets the IRS can seize through a tax levy:

1. Wages and Salary (Wage Garnishment)

Your employer may be legally required to withhold a portion of each paycheck and send it directly to the IRS. The amount you are allowed to keep depends on your filing status and number of dependents. This garnishment continues until the debt is paid in full or the IRS agrees to release the levy.

2. Bank Accounts

The IRS can issue a bank levy, instructing your financial institution to freeze your funds for 21 days. During this time, you cannot access the money. If you don’t resolve the issue within the 21-day window, the bank must transfer the frozen funds to the IRS.

3. Real Estate and Vehicles

The IRS can seize and sell property you own, such as houses, land, cars, or boats. While seizure of a primary residence requires a court order, other properties do not. The proceeds from the sale are applied to your tax debt, and any excess may be refunded to you.

4. Retirement Accounts

Funds in IRAs, self-employed retirement plans, pensions, and other retirement accounts can be levied if you have the right to access them. However, some employer-sponsored plans may be protected depending on state law.

5. Rental Income and Dividends

The IRS can redirect payments from tenants or investment dividends to satisfy your tax debt. They may contact third parties directly and require them to send the payments to the government instead of you.

6. Accounts Receivable and Commissions

If you are self-employed or run a business, the IRS can intercept client payments, accounts receivable, or earned commissions before they reach you. This can significantly disrupt cash flow and business operations.

7. Cash Value of Life Insurance Policies

Life insurance policies with a cash surrender value can be levied. The IRS may require the insurer to pay out the cash value to the IRS, reducing the value of your policy or even canceling it in the process.

8. Federal and State Tax Refunds

The IRS can apply any current or future tax refunds you’re due toward your outstanding tax bill. This includes both federal and state refunds through programs like the State Income Tax Levy Program (SITLP).

9. Business Assets

Business equipment, inventory, vehicles, and even bank accounts tied to your business may be subject to levy, especially if payroll taxes or corporate taxes remain unpaid. This can paralyze operations and damage customer relationships.

10. Other Personal Property

In rare and serious cases, the IRS may also seize personal property such as jewelry, electronics, or collectibles. Though not common, such actions are typically reserved for high-value items or severe cases of tax fraud or evasion.

Types of Tax Levy

Types of Tax Levy

A tax levy isn’t limited to just your paycheck or bank account. The IRS and state tax authorities can legally seize a wide range of assets to recover unpaid taxes, and the method they use often depends on the nature of the taxpayer’s income, lifestyle, and holdings. These levies can disrupt your personal finances, professional life, and even long-term savings plans. Some levies are straightforward, like wage garnishment, while others can involve business revenue or even retirement funds. By understanding the different types of tax levies, you’ll be better equipped to identify the risks and take steps to avoid or resolve them before they escalate.

Here are the major types of tax levies in more detail:

1. Wage Garnishment

One of the most common tax levies, wage garnishment forces your employer to withhold a portion of your income and send it directly to the IRS. The amount withheld is based on your income and number of dependents, but it can still significantly reduce your take-home pay. This garnishment remains in place until the debt is paid in full or an agreement is reached with the IRS.

2. Bank Levy

The IRS can instruct your bank to freeze the funds in your account for 21 days. During that time, you cannot access or withdraw any money. If you don’t settle the debt within the holding period, the bank must transfer the frozen funds to the IRS. This type of levy can cause bounced checks, missed payments, and serious financial disruption.

3. Property Seizure

In more serious cases, the IRS may seize your physical property—such as cars, boats, land, or even a house. While primary residences are more difficult to seize (requiring court approval), other property can be taken and sold to cover the tax debt. You’ll be notified of the sale, and any leftover proceeds after the tax is paid may be refunded to you.

4. Reduced Tax Refunds

If you’re due a refund from the IRS or your state, they can automatically apply it toward your back taxes. This is often one of the earliest forms of collection enforcement and doesn’t require further notice.

5. Accounts Receivable Levy

If you’re a business owner or freelancer, the IRS can levy the payments you’re set to receive from clients or customers. These third parties are instructed to send the money to the IRS instead of to you, which can cripple your cash flow and threaten business survival.

6. Retirement Account Levy

Retirement accounts such as IRAs, 401(k)s, pensions, and military retirement plans are not off-limits. If you have access to the funds, the IRS can seize them. While this is not typically the first step in a levy, it becomes a consideration if other assets are insufficient.

7. Life Insurance Levy

If you own a whole life or universal life insurance policy with a cash value, the IRS may claim that amount through a levy. The insurer is required to pay the IRS from the surrender value of your policy.

8. 1099 Income Levy

Independent contractors and self-employed individuals may have their 1099 payments levied. The IRS can instruct businesses or clients who owe you money to redirect payments to them instead, leading to loss of income without direct warning.

9. Business Asset Levy

Businesses that fail to pay payroll or corporate taxes can have their equipment, inventory, and even business vehicles seized. This not only disrupts operations but also puts jobs and customer relationships at risk.

10. Passport Revocation (Indirect Levy Consequence)

If you owe more than a certain threshold (e.g., $54,000 in seriously delinquent tax debt), the IRS may notify the U.S. State Department. This could lead to denial or revocation of your passport, affecting your ability to travel internationally. While not a direct seizure of property, it’s a powerful enforcement tool tied to unpaid taxes.

How a Tax Levy Affects You

A tax levy can have serious and immediate consequences on your financial stability and personal life. Once enforced, it gives the IRS the legal authority to seize your income, bank funds, property, or other valuable assets to recover unpaid taxes. The impact can be deeply disruptive—ranging from frozen accounts and shrinking paychecks to the potential loss of your home or business assets. Even if you’re not directly contacted, the IRS may reach out to employers, banks, or third parties to collect what you owe. Understanding how a tax levy affects you is essential to taking timely action before the situation worsens.

Here are key ways a tax levy can affect you:

1. Wage Garnishment: A portion of each paycheck is withheld by your employer and sent to the IRS, reducing your disposable income and making it harder to cover living expenses.

2. Frozen Bank Accounts: The IRS can freeze your bank account for 21 days and then seize the funds, potentially causing bounced checks or missed payments.

3. Seizure of Personal Property: Vehicles, real estate, and other assets may be taken and sold to pay your tax debt, especially in severe cases.

4. Intercepted Tax Refunds: Federal and state tax refunds you’re owed can be redirected to cover your outstanding balance.

5. Loss of Retirement Funds: The IRS can levy IRAs, pensions, and other retirement accounts if you have access to those funds.

6. Disruption to Business Operations: Business assets, customer payments, and inventory can be seized, harming operations and revenue flow.

7. Credit and Travel Restrictions: While a levy itself doesn’t appear on your credit report, related tax liens or resulting unpaid bills might. If you owe more than a certain amount, your passport could be denied or revoked.

8. Emotional and Legal Stress: Facing a levy can create significant emotional pressure and may require legal or financial assistance to resolve.

How to Avoid a Tax Levy

Avoiding a tax levy starts with proactive communication and responsible tax habits. The IRS doesn’t begin seizing property without warning—it sends multiple notices and offers options for payment plans or dispute resolution before taking action. By staying ahead of deadlines, addressing tax issues promptly, and reaching out for help when needed, you can prevent your situation from escalating to the point of asset seizure. Avoiding a levy is often much easier—and far less stressful—than trying to stop or reverse one once it’s begun.

Here are effective ways to avoid a tax levy:

1. File Tax Returns on Time: Late or unfiled tax returns can trigger IRS enforcement actions, even if you can’t pay right away.

2. Pay Taxes When Due: Paying your taxes in full and on time each year is the simplest way to stay off the IRS’s radar.

3. Request an Extension If Needed: If you can’t file on time, request a filing extension to avoid penalties and preserve your compliance status.

4. Set Up a Payment Plan: If you can’t pay in full, apply for an IRS installment agreement to make manageable monthly payments.

5. Apply for an Offer in Compromise: If you’re unable to pay the full amount, you may qualify to settle your tax debt for less.

6. Respond to IRS Notices Promptly: Ignoring IRS letters is one of the fastest ways to face enforcement. Always open and act on them right away.

7. Request a Collection Due Process (CDP) Hearing: If you receive a Final Notice of Intent to Levy, file for a CDP hearing within 30 days to delay enforcement and explore alternatives.

8. Communicate Financial Hardship: If a levy would cause serious financial strain, inform the IRS. They may delay or halt action if you demonstrate hardship.

9. Consult a Tax Professional: If you’re unsure how to proceed, working with a CPA, tax attorney, or enrolled agent can help you navigate your options effectively.

How to Stop or Remove a Tax Levy

Stopping or removing a tax levy is possible, but it requires swift and strategic action. Once the IRS places a levy on your wages, bank accounts, or assets, it doesn’t automatically go away—you must either resolve the debt or qualify for relief. The good news is that the IRS provides several pathways to have a levy released, especially if the seizure causes financial hardship or if you’ve taken steps to resolve your tax situation. Acting quickly can protect your property and give you time to work out a solution.

Here are common ways to stop or remove a tax levy:

1. Pay Your Tax Debt in Full: The most direct way to remove a levy is to pay the total amount you owe, including any penalties and interest.

2. Enter Into an Installment Agreement: If you can’t pay in full, negotiating a monthly payment plan with the IRS can lead to a levy release.

3. Submit an Offer in Compromise (OIC): If you qualify, you may settle your debt for less than the full amount. Approval of an OIC can stop collection actions.

4. Prove Financial Hardship: If the levy prevents you from covering basic living expenses, the IRS may release it due to economic hardship.

5. Request a Collection Due Process (CDP) Hearing: If you act within 30 days of receiving a Final Notice of Intent to Levy, a CDP hearing can pause the levy and allow you to appeal or resolve the issue.

6. File for Bankruptcy (As a Last Resort): In some cases, bankruptcy can stop or eliminate certain tax debts and levies, but it comes with serious long-term consequences.

7. Demonstrate That the Levy Was Issued in Error: If the IRS levied you by mistake—such as after the collection period expired or during an appeal—you may request an immediate release.

8. Prove That the Seized Assets Have No Equity: If the IRS is levying property that has no real value or can’t be sold, you may request that the levy be lifted.

9. Show That Releasing the Levy Will Help Pay the Debt: If you can prove that lifting the levy will allow you to make payments or sell assets to pay the IRS, they may agree to remove it.

Conclusion

A tax levy is one of the most serious enforcement actions the IRS can take, often resulting in the direct seizure of your income, property, or financial assets. However, it doesn’t have to reach that point. By understanding how tax levies work, recognizing the types of assets at risk, and taking early, proactive steps—such as communicating with the IRS, setting up a payment plan, or seeking professional help—you can avoid or resolve a levy before it causes lasting damage. Whether you’re facing collection notices or already under a levy, timely action is key to protecting your financial future and regaining control over your tax situation.