Managing money in today’s digital-first world no longer requires sitting across a desk from a financial professional. With the rise of technology, many people are turning to Virtual Financial Advisors (VFAs)—qualified experts who deliver the same financial planning, investment management, and retirement strategies as traditional advisors, but entirely online. Whether through video calls, secure portals, or mobile apps, a virtual advisor brings professional guidance to you wherever you are. Beyond convenience, the real strength of a virtual financial advisor lies in their ability to craft personalized, tailored advice that adapts to your goals, lifestyle, and changing circumstances.

What is a Virtual Financial Advisor?

A Virtual Financial Advisor (VFA) is a licensed professional who provides financial guidance and planning entirely through digital channels such as video calls, secure client portals, email, or mobile apps. Just like a traditional advisor, they can help with investment management, retirement planning, tax strategies, estate planning, and even insurance advice—but without the need for face-to-face office meetings. By combining professional expertise with digital tools, virtual advisors make financial planning more convenient, flexible, and accessible, no matter where you live.

How Does a Virtual Financial Advisor Work?

How Does a Virtual Financial Advisor Work?

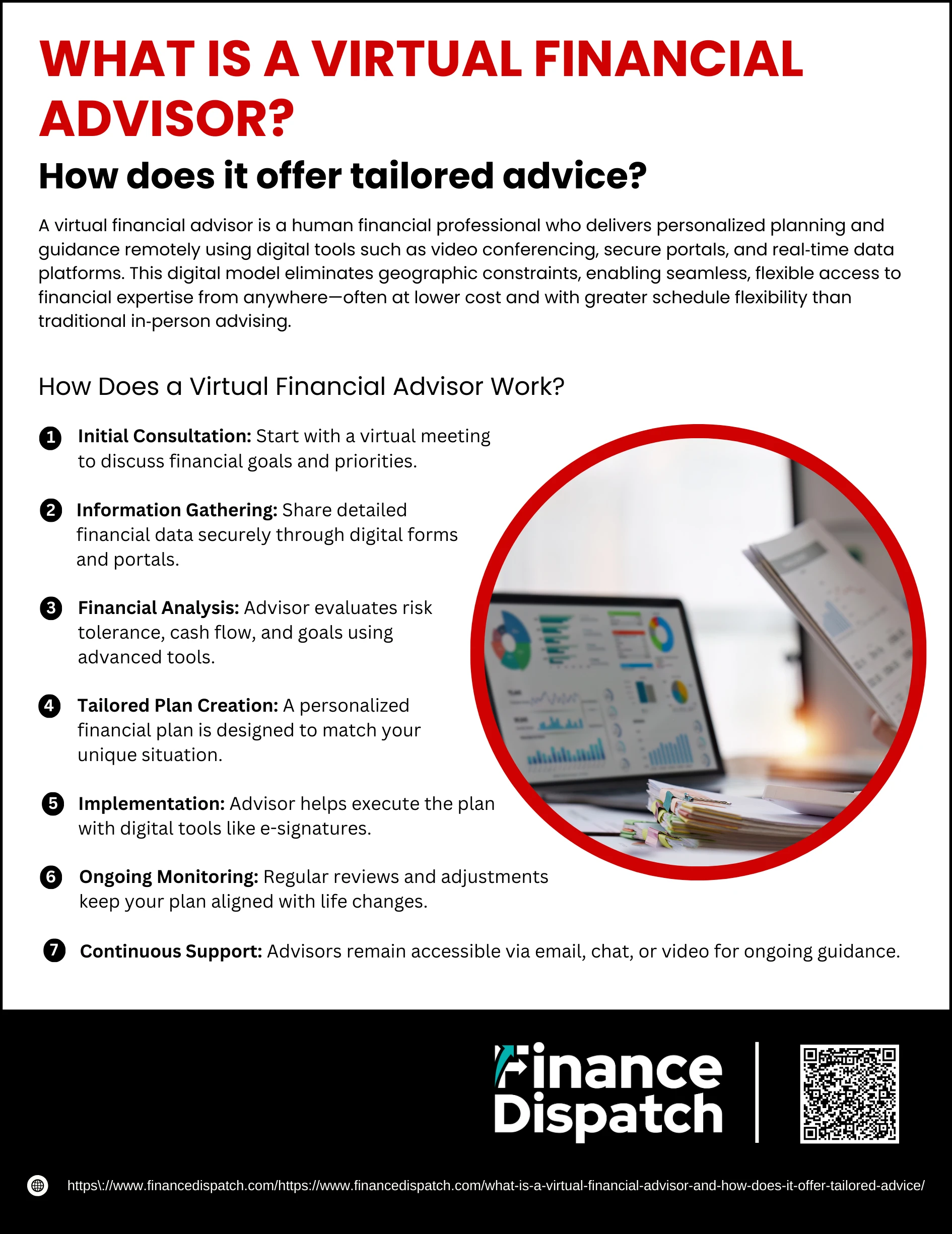

A virtual financial advisor provides the same services as a traditional advisor but delivers them through digital platforms. By using secure portals, video conferencing, and cloud-based tools, they make it possible to manage your financial future from anywhere. Below is a detailed look at the process:

1. Initial Consultation

Your journey usually begins with a virtual meeting—via Zoom, Google Meet, or a secure platform—where you and the advisor discuss your financial goals. This could include retirement dreams, debt management, investment growth, or planning for big milestones like buying a home. The aim is to get a clear picture of your priorities and comfort level.

2. Information Gathering

After the first meeting, the advisor requests detailed information about your finances. This may include your income, expenses, debts, investments, insurance policies, and future aspirations. Secure digital forms and encrypted portals make sharing documents safe and efficient, eliminating the need for paper-based processes.

3. Financial Analysis

Using advanced software, the advisor evaluates your current financial position. They assess your risk tolerance, cash flow, and long-term objectives. Data visualization tools or dashboards often help you see your full financial picture in one place, making the process more transparent.

4. Tailored Plan Creation

Based on your profile, the advisor designs a personalized financial plan. This could involve optimizing your investment strategy, creating a retirement roadmap, building tax-efficient approaches, or recommending insurance coverage. Unlike robo-advisors that use generic models, human virtual advisors craft advice that aligns with your unique situation.

4. Implementation

Once the plan is ready, the advisor helps you take action. This may include opening or restructuring investment accounts, reallocating assets, or purchasing suitable financial products. Digital tools such as e-signatures make this process quick and seamless, without the need for in-person paperwork.

5. Ongoing Monitoring

Financial planning isn’t “set and forget.” A virtual financial advisor regularly reviews your progress and makes adjustments when needed. For example, they may rebalance your portfolio during market changes or adapt your retirement savings plan if your income shifts. You can expect quarterly or annual reviews, often done virtually.

6. Continuous Support

Beyond formal reviews, you have access to ongoing support. Many advisors offer communication through email, chat, or quick video sessions to answer questions. This flexibility means you can seek advice whenever life changes occur—whether it’s a new job, marriage, or unexpected expenses—without waiting weeks for an appointment.

Benefits of a Virtual Financial Advisor

Benefits of a Virtual Financial Advisor

A virtual financial advisor (VFA) brings the expertise of a traditional advisor into the digital space, making financial guidance more convenient, accessible, and often more affordable. Instead of spending time driving to an office or fitting into rigid schedules, you can manage your financial life on your terms. Here’s a closer look at the key benefits:

1. Convenience and Flexibility

Virtual advisors remove the barriers of location and time. Whether you’re at home, traveling for work, or even living abroad, you can connect with your advisor through secure video calls or phone sessions. Meetings are easier to fit into a busy schedule and can often be shorter and more focused. For people with mobility challenges or those living in remote areas, this accessibility is especially valuable.

2. Lower Costs

Because virtual advisors don’t need to maintain physical office spaces or large in-person teams, their overhead expenses are much lower. Many pass these savings directly to clients in the form of reduced fees. Over the long run, paying less for professional guidance helps you keep more of your money invested and compounding toward your goals.

3. Access to Broader Expertise

Working virtually gives you access to financial advisors beyond your local area. This means you can choose a specialist who truly understands your needs—for example, retirement planning for business owners, tax strategies for freelancers, or estate planning for families. Instead of settling for whoever is nearby, you can select the best match for your situation, no matter where they are located.

4. Tailored Financial Advice

Virtual advisors don’t just give generic recommendations. Using digital intake forms, secure document sharing, and financial planning software, they gather a complete view of your financial picture. This allows them to create a customized plan that reflects your goals, income, lifestyle, and risk tolerance. As your circumstances change—like getting married, changing jobs, or planning for retirement—they can quickly adjust your plan.

5. Cutting-Edge Technology

Many VFAs rely on advanced platforms and tools such as robo-advisors, real-time portfolio trackers, and wealth management dashboards. These technologies allow you to see your financial health at a glance, track your progress, and even get automated alerts when adjustments are needed. The combination of professional advice and technology makes the planning process smoother and more transparent.

6. Ongoing Support and Accessibility

With virtual advisors, communication isn’t limited to formal office appointments. You can reach out through email, secure messaging, or video calls whenever questions come up. This accessibility ensures you get timely advice—for example, if the market changes suddenly or you need quick input on a financial decision. The continuous support creates a stronger advisor-client relationship and helps keep your financial plan up to date.

How Virtual Financial Advisors Offer Tailored Advice

How Virtual Financial Advisors Offer Tailored Advice

One of the strongest advantages of working with a virtual financial advisor (VFA) is the ability to receive highly personalized guidance. Rather than giving generic, cookie-cutter advice, they use a blend of digital tools, secure platforms, and professional expertise to build strategies that reflect your life goals, financial situation, and evolving needs. Here’s how the process of tailoring advice typically works:

1. Understanding Your Personal Goals

Every tailored plan starts with a conversation. Your advisor takes time to learn what matters most to you—whether it’s saving for a down payment, building long-term wealth, planning for retirement, or even funding your children’s education. By focusing on your priorities and values, they can ensure every recommendation connects directly to your financial vision.

2. Collecting and Analyzing Your Financial Data

Instead of lengthy paperwork and office visits, you securely upload your financial details through encrypted portals or digital forms. This includes income, expenses, debt, savings, investments, and insurance. The advisor then analyzes this information with specialized financial software, which helps identify both strengths and gaps in your current financial setup.

3. Creating a Customized Financial Plan

Based on your profile, the advisor develops a plan tailored specifically to your goals. For example, if you’re risk-averse, they might recommend a conservative investment mix, while someone aiming for aggressive growth might receive a different strategy. Plans often combine multiple elements—like retirement savings, tax-efficient investing, and estate planning—to give you a holistic roadmap.

4. Using Technology for Personalization

Virtual financial advisors leverage technology to refine and personalize advice further. They use portfolio tracking dashboards, AI-driven analysis, and even robo-advisor tools to monitor your accounts in real time. This tech integration not only keeps your plan up-to-date but also helps visualize your progress with charts, projections, and scenario planning, making your financial journey easier to understand.

5. Adjusting Strategies as Life Changes

Your life will change—and your financial plan should too. Virtual advisors regularly review your situation and update your plan if you change jobs, get married, start a business, or face unexpected financial challenges. Because everything is managed online, adjustments can be made quickly, ensuring your plan always reflects your current reality.

6. Providing Ongoing Guidance and Support

Tailored advice isn’t just about the initial plan—it’s about continuous partnership. Virtual advisors remain accessible via video calls, emails, or secure messaging whenever questions arise. Whether you want to check if you’re still on track, explore a new investment opportunity, or respond to market changes, your advisor can provide guidance without the delays that often come with traditional office visits.

Challenges and Limitations of Virtual Financial Advisor

While virtual financial advisors (VFAs) offer convenience, affordability, and tailored advice, they are not without challenges. Relying on technology and remote communication introduces certain drawbacks that clients should carefully consider before choosing this approach. Here are some of the most common limitations:

1. Technology Dependence – Reliable internet access and comfort with digital tools are required; technical issues can disrupt meetings or cause delays.

2. Lack of Face-to-Face Interaction – Some clients prefer in-person discussions for trust-building, which can be harder to replicate online.

3. Data Security Concerns – Sharing sensitive financial information online raises privacy and cybersecurity risks if proper safeguards aren’t in place.

4. Limited Emotional Insight – Advisors may miss non-verbal cues that are easier to detect in person, which can affect the depth of advice.

5. Regulatory Complexity – Virtual advisors must comply with state, national, and sometimes international regulations, which may confuse clients.

6. Client Trust Issues – New clients may hesitate to trust someone they’ve never met physically with their financial future.

7. Not Suitable for Everyone – Those uncomfortable with digital platforms or who prefer highly personal, face-to-face services may find VFAs less appealing.

Who Should Consider a Virtual Financial Advisor?

A virtual financial advisor (VFA) can be a smart choice for many people, especially those who prefer flexibility, affordability, and digital solutions. While not every client will find this approach ideal, certain groups often benefit the most:

1. Busy Professionals – People with demanding jobs who struggle to schedule in-person meetings can save time by connecting with advisors online at flexible hours.

2. Tech-Savvy Individuals – Clients comfortable using apps, video calls, and financial dashboards will find virtual advising both efficient and easy to manage.

3. People in Remote Areas – Those living far from major cities gain access to professional financial advice without traveling long distances.

4. Cost-Conscious Investors – Virtual advisors often charge lower fees than traditional advisors, making them appealing for those who want to maximize value.

5. Frequent Travelers or Expats – Individuals who relocate often or live overseas can maintain consistent relationships with advisors regardless of location.

6. Clients Seeking Privacy – Some people feel more comfortable sharing personal financial details virtually rather than face-to-face.

7. Young Adults and First-Time Investors – New investors looking to start budgeting, saving, and building wealth can access professional guidance without formal office visits.

Future of Virtual Financial Advisors

The future of virtual financial advisors looks promising as technology continues to transform the way people manage their money. With advances in artificial intelligence, robo-advisors, and secure digital platforms, clients can expect even more personalized, data-driven strategies delivered with speed and convenience. Hybrid m odels—where human advisors work alongside AI tools—are becoming increasingly popular, blending professional insight with real-time automation. As more people embrace remote services for banking, healthcare, and shopping, financial advising is naturally following the same path. In the coming years, virtual advisors are likely to expand their reach, offer hyper-personalized financial planning, and make quality advice more affordable and accessible to a broader audience.

Conclusion

Virtual financial advisors have redefined the way people access financial guidance, offering a balance of convenience, affordability, and personalization. By combining professional expertise with digital tools, they make it easier for clients to create, manage, and adjust financial plans without the limitations of location or rigid schedules. While challenges like data security and the lack of face-to-face interaction remain, the benefits—especially tailored advice and ongoing support—are hard to overlook. For many individuals, from busy professionals to cost-conscious investors, working with a virtual advisor can be the key to achieving financial goals in today’s fast-paced, digital world.