When people talk about alternative ways to raise money, terms like crowdlending and crowdfunding often come up—and while they sound similar, they work in very different ways. Both methods bypass traditional banks and financial institutions, giving individuals and businesses more direct access to capital. However, the purpose, structure, and benefits of crowdlending compared to crowdfunding set them apart. Understanding these differences is important whether you’re an entrepreneur looking for funding, an investor seeking new opportunities, or simply curious about how modern finance is evolving.

What is Crowdlending?

Crowdlending, also known as peer-to-peer (P2P) lending or debt-based crowdfunding, is a way of borrowing and lending money directly between individuals or businesses through an online platform. Instead of going to a bank for a loan, borrowers list their funding needs on a crowdlending platform, and investors contribute money in exchange for regular repayments with interest. This creates a win-win situation: borrowers gain quicker access to capital, often with more flexible terms, while lenders have the chance to earn higher returns compared to traditional savings accounts. However, like any loan, crowdlending carries the risk of default if the borrower cannot repay.

What is Crowdfunding?

Crowdfunding is a method of raising money by collecting small contributions from a large number of people, usually through online platforms. Instead of relying on a single investor or a bank, individuals, startups, and organizations can showcase their ideas, products, or causes and invite the public to support them. Depending on the type of crowdfunding, backers may receive different outcomes: a reward such as early access to a product, equity or shares in the business, or simply the satisfaction of donating to a cause they believe in. This approach not only provides funding but also helps validate ideas and build a community around them.

Crowdlending vs. Crowdfunding: Key Differences

Although crowdlending and crowdfunding both involve raising money outside of traditional banks, they serve different purposes and offer distinct benefits to participants. Crowdlending is structured as a loan with repayment and interest, while crowdfunding is usually about supporting ideas, projects, or businesses in exchange for rewards, equity, or simply the satisfaction of contributing. To make the contrast clearer, here’s a side-by-side comparison:

| Aspect | Crowdlending | Crowdfunding |

| Purpose | Borrow money as a loan and repay with interest | Raise money to support a project, product, or cause |

| Return for Funders | Interest payments from borrowers | Rewards (products/services), equity shares, or no return (donations) |

| Risk | Borrower may default on loan | Project may fail, rewards may not be delivered |

| Repayment/Return Timeline | Fixed repayment schedule | Varies—depends on project type and delivery |

| Regulation | Often regulated under financial lending laws | Lighter or different regulation depending on type (reward, equity, donation) |

| Best For | Investors seeking financial return | Creators seeking community support or validation of an idea |

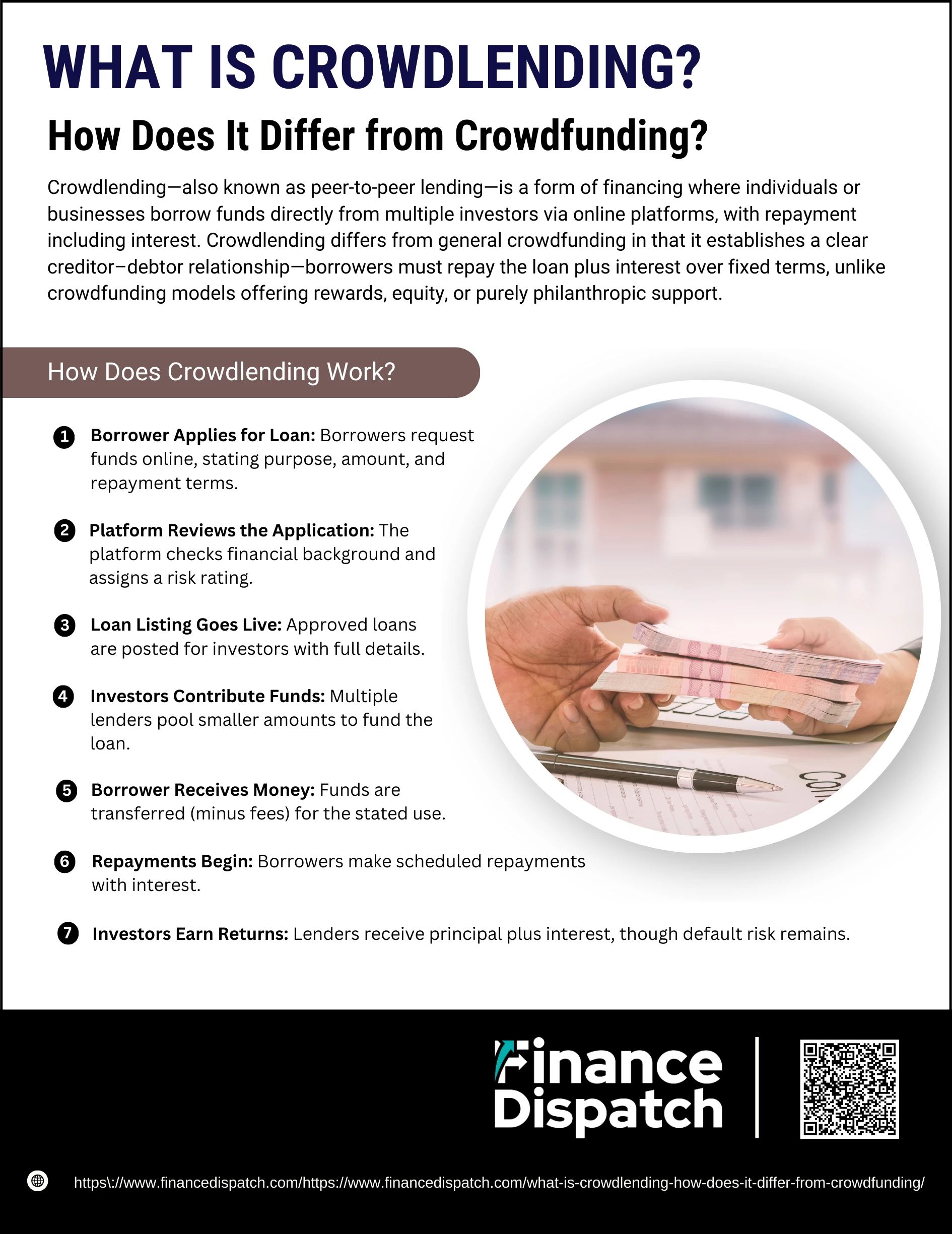

How Does Crowdlending Work?

How Does Crowdlending Work?

Crowdlending connects borrowers with multiple individual investors who collectively fund a loan. The process is designed to be simple, transparent, and efficient, but it still follows structured steps to balance opportunities and risks for both sides.

Steps in the Crowdlending Process

1. Borrower Applies for Loan

A person, startup, or business in need of funds creates a loan request on a crowdlending platform. They specify the amount they want to borrow, how they intend to use the money (e.g., business expansion, home renovation, debt consolidation), and the repayment period.

2. Platform Reviews the Application

Before making the request visible to investors, the platform conducts checks on the borrower’s financial background. This may include reviewing credit scores, income levels, existing debts, and repayment capacity. The borrower is then assigned a risk rating, which influences the interest rate they must pay.

3. Loan Listing Goes Live

Once approved, the loan request is posted publicly on the platform. Potential investors can view details such as the borrower’s profile, loan purpose, interest rate, and repayment terms. This transparency helps investors decide whether to contribute.

4. Investors Contribute Funds

Multiple lenders can each invest small amounts, reducing their individual risk. For example, instead of one person lending $10,000, 100 different investors might each contribute $100. The platform ensures that funds are pooled until the full loan amount is reached.

5. Borrower Receives Money

After the loan is fully funded, the borrower receives the money in their account, minus any platform fees. They can then use it for the stated purpose, such as purchasing equipment, covering operating costs, or financing personal needs.

6. Repayments Begin

Borrowers make regular repayments, typically monthly, which include both principal and interest. The platform automates this process, collecting payments from the borrower and redistributing them to investors.

7. Investors Earn Returns

As repayments are made, each investor receives their share of the principal and interest. Returns are usually higher than traditional savings or fixed deposits, but they depend on the borrower’s ability to repay. If the borrower defaults, investors may lose part of their investment.

Benefits of Crowdlending and Crowdfunding

Benefits of Crowdlending and Crowdfunding

Both crowdlending and crowdfunding are transforming how money moves between people, businesses, and communities. They eliminate many of the barriers created by traditional finance, making it easier for entrepreneurs to fund their projects and for individuals to participate as lenders or supporters. Below are the key benefits explained in more detail:

Key Benefits

1. Easier Access to Capital

Traditional bank loans often involve strict requirements such as high credit scores, collateral, or long approval processes. Crowdlending and crowdfunding reduce these barriers by allowing individuals and small businesses to raise funds directly from people online. This makes them especially valuable for startups, creative projects, or borrowers who may not qualify for conventional financing.

2. Flexibility for Businesses and Individuals

Unlike bank loans that are usually limited to specific purposes, both models provide flexibility. Entrepreneurs can use crowdfunding to finance new products, apps, or artistic ventures, while crowdlending can support anything from personal loans and home renovations to small business expansion. This freedom of use is one of the reasons they appeal to such a wide audience.

3. Opportunities for Investors and Supporters

Investors in crowdlending earn regular interest payments, often higher than what they’d get from savings accounts or fixed deposits. Crowdfunding backers, on the other hand, can receive early access to products, equity shares, or simply the joy of helping bring an idea to life. Both sides—lenders and supporters—get to participate in financial opportunities that were once restricted to banks or large investors.

4. Community Engagement

Crowdfunding in particular fosters a strong sense of belonging between creators and their supporters. People who back a project often feel personally connected to its success and may even promote it within their own circles. In crowdlending, although the focus is financial, trust is still built between borrowers and lenders, creating a more personal connection compared to traditional banking.

5. Validation of Ideas

For entrepreneurs, launching a crowdfunding campaign is a way to test the market before fully investing in production. If hundreds or thousands of people are willing to contribute money, it signals strong demand for the idea. This “proof of concept” not only attracts backers but can also help in securing additional investors later on.

6. Higher Returns for Investors

Crowdlending offers a chance for lenders to earn better returns than typical savings accounts or government bonds. Because loans are directly funded by individuals without bank overhead costs, interest rates for borrowers can still be competitive, while lenders enjoy a share of those returns. Of course, higher returns also come with higher risks, but the potential earnings are a strong incentive.

7. Diverse Funding Options

The availability of both crowdlending and crowdfunding provides choices based on financial goals. Those seeking structured repayment and interest might prefer crowdlending, while those looking to build community support or test an idea may lean toward crowdfunding. This variety ensures that different needs—whether financial or creative—can be met outside the traditional system.

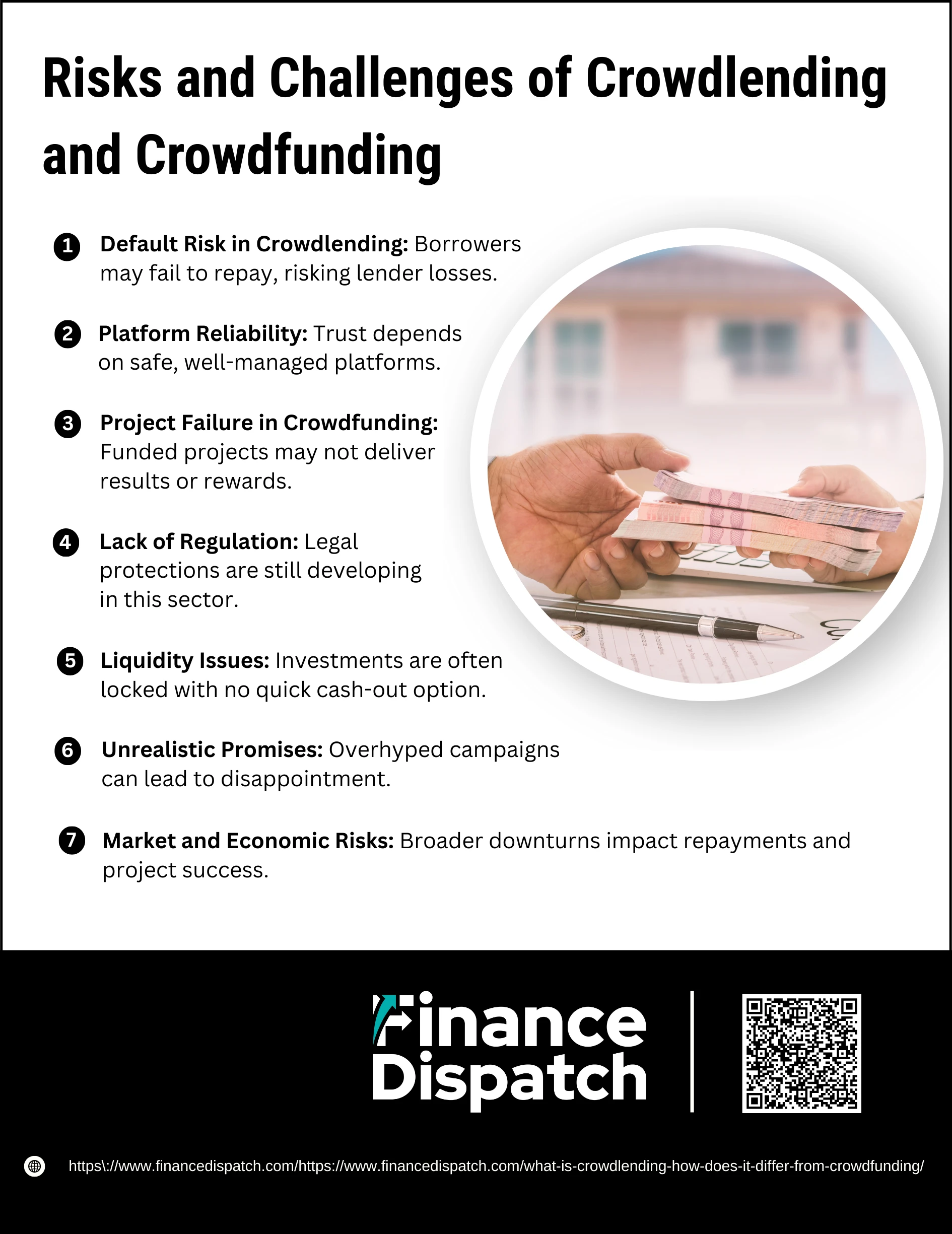

Risks and Challenges of Crowdlending and Crowdfunding

Risks and Challenges of Crowdlending and Crowdfunding

Although crowdlending and crowdfunding provide innovative ways to raise and invest money, they are not risk-free. Both models shift financial responsibility away from banks and institutions to individuals, which creates opportunities but also vulnerabilities. To make informed decisions, it’s important to understand the main challenges associated with these platforms.

Key Risks and Challenges

1. Default Risk in Crowdlending

In crowdlending, borrowers promise to repay the loan with interest, but there’s always a chance they may fail to do so. If a borrower defaults, lenders can lose part or all of their investment. Unlike banks, which have more tools for debt collection and collateral management, crowdlending platforms often provide limited protection, making this one of the biggest risks for investors.

2. Platform Reliability

Both crowdlending and crowdfunding rely entirely on the online platform acting as a trustworthy middleman. If the platform mismanages funds, shuts down unexpectedly, or worse, turns out to be fraudulent, users could lose their money. Choosing a regulated and reputable platform is critical to reducing this risk.

2. Project Failure in Crowdfunding

Just because a crowdfunding campaign reaches its funding goal does not guarantee success. Many projects fail to deliver products on time, meet promised quality standards, or even launch at all. Backers often have little legal recourse if creators cannot fulfill their commitments, which can lead to frustration and financial loss.

3. Lack of Regulation

While traditional banks and financial institutions are strictly regulated, alternative finance platforms operate in a relatively new space. Laws and protections for investors or backers are still evolving. This lack of regulation can make it harder to resolve disputes, recover funds, or hold parties accountable if things go wrong.

4. Liquidity Issues

Money invested in crowdlending or contributed to crowdfunding campaigns is usually locked in. In crowdlending, lenders must wait until the loan matures and repayments are made, while crowdfunding contributions are often non-refundable. Unlike stocks or savings, there’s no easy way to “cash out” early, which limits financial flexibility.

5. Unrealistic Promises

Many crowdfunding campaigns attract attention with bold claims and ambitious visions. However, some creators exaggerate what they can deliver, leading to unrealistic expectations among backers. When projects fail to live up to the hype, it creates disappointment and damages trust in the system.

6. Market and Economic Risks

Broader economic conditions also affect these models. In times of recession or financial instability, borrowers may struggle to repay crowdlending loans, and consumer interest in crowdfunding projects may decline. Investors and backers need to account for external factors beyond the platform itself.

Types of Crowdlending Platforms

Crowdlending platforms come in different forms, each catering to specific borrower needs and investor interests. By understanding the main types, you can decide which platform aligns best with your financial goals, whether you’re borrowing money or looking to invest.

1. Consumer Lending Platforms

These platforms focus on personal loans for individuals. Borrowers might use them for debt consolidation, home renovations, medical bills, or other personal needs. Investors benefit by earning interest on relatively short- to medium-term loans.

2. Business Lending Platforms

Aimed at small and medium-sized enterprises (SMEs), these platforms help businesses raise capital without going through banks. The funds might support expansion, purchase of equipment, or day-to-day operations, while investors enjoy structured repayment plans.

3. Real Estate Crowdlending Platforms

Specialize in financing property projects, such as housing developments, commercial buildings, or renovations. They are attractive to investors who want exposure to real estate markets without directly owning property.

4. Invoice Financing Platforms

Allow businesses to borrow against unpaid invoices, giving them quick access to working capital. For investors, this type of lending offers shorter repayment cycles, since invoices are usually settled within a few months.

5. Student Loan Platforms

Help students fund education by connecting them directly with individual lenders. Borrowers gain access to funds for tuition or living expenses, and lenders often receive fixed interest payments over several years.

6. Green or Impact Lending Platforms

Dedicated to financing environmentally friendly or socially responsible projects, such as renewable energy, sustainable farming, or community initiatives. Investors here are motivated not only by financial returns but also by the desire to create a positive impact.

Crowdlending vs. Crowdfunding: Which One is Right for You?

When you’re looking to raise capital, both crowdlending and crowdfunding open doors that traditional banks often keep closed. The right choice depends on your goals and what you’re willing to give up in return. If you need a loan that you can repay over time with interest—while keeping full ownership of your business—crowdlending is often the better option. It provides faster access to funds, more flexible terms, and allows you to build credibility with a community of lenders. Crowdfunding, on the other hand, works best when your project is creative, community-driven, or product-focused. Instead of paying back money, you typically offer rewards, early access, or even equity. This makes crowdfunding attractive if you want to test the market or build a loyal customer base, but it may mean sharing part of your vision or ownership. Ultimately, the decision comes down to whether you prefer the security of keeping control with scheduled repayments, or the community engagement and visibility that comes from sharing your idea with backers.

Conclusion

Crowdlending and crowdfunding both harness the power of the crowd, but they serve very different purposes. Crowdlending is debt-based, giving startups and businesses the ability to borrow funds directly from individual investors while retaining full ownership, with the obligation to repay with interest. Crowdfunding, by contrast, is more about community support, whether through donations, rewards, or equity, and often works well for creative ideas or early-stage projects looking to gain visibility. Choosing between the two comes down to your priorities—whether you value predictable repayment and ownership (crowdlending) or community engagement and flexibility without repayment (crowdfunding). Understanding these distinctions allows you to select the financing model that aligns best with your business goals and growth strategy.