In simple terms, inflation is the gradual rise in the cost of goods and services, which slowly eats away at the value of your money. Over time, even modest inflation can reduce your purchasing power, making everyday expenses more costly and long-term savings less effective. This is why many investors look for ways to protect their wealth against the eroding effects of inflation. Inflation-protected investing focuses on choosing assets that can hold—or even increase—their value when prices rise, helping you preserve your money’s real worth. In this article, we’ll explore what inflation-protected investing means, why it matters, and which assets have historically worked best to keep pace with rising prices.

What is Inflation-Protected Investing?

Inflation-protected investing is a strategy designed to safeguard your money from losing value as the cost of living rises. Instead of relying solely on traditional fixed-income assets, which can struggle during inflation, this approach focuses on investments that adjust in value or income to match inflation rates. These can include government-issued securities like Treasury Inflation-Protected Securities (TIPS), tangible assets such as real estate and commodities, or stocks in sectors with strong pricing power. The goal is not just to preserve your purchasing power, but to earn a “real return”—growth that outpaces inflation—so your wealth maintains or improves its value over time.

How Inflation Impacts Different Asset Classes

How Inflation Impacts Different Asset Classes

Inflation doesn’t affect all investments equally. While some assets see their value eroded, others can adapt or even benefit when prices rise. The impact largely depends on how the asset generates returns and whether it can adjust to higher costs. Understanding these differences can help you choose investments that better withstand inflationary pressures.

1. Fixed-Rate Bonds

Fixed-rate bonds pay a set interest amount throughout their term. During inflation, this interest becomes less valuable because the purchasing power of the payments declines. At the same time, market interest rates often rise to counter inflation, which pushes down the market value of existing bonds. As a result, investors holding fixed-rate bonds may face both reduced real income and capital losses if they sell before maturity.

2. Stocks (Equities)

Stocks can offer some protection against inflation, but results vary by sector and company. Businesses with strong pricing power—such as consumer staples, utilities, or healthcare providers—can pass increased costs to customers without losing significant demand, helping maintain profit margins. In contrast, companies in highly competitive markets or with high fixed costs may see profits shrink when input prices rise, making their shares more vulnerable during inflationary periods.

3. Real Estate

Real estate often benefits from inflation because property values and rental income typically rise alongside the general cost of living. For landlords, this means higher rental yields over time, helping offset inflation’s impact. However, real estate can be sensitive to interest rates; when rates rise sharply to fight inflation, mortgage costs increase, which can slow property price growth or even cause declines in overheated markets.

4. Commodities

Commodities like oil, natural gas, agricultural goods, gold, and other raw materials often see price increases during inflation. This is because these resources are fundamental to the production of goods and services, so their rising costs ripple through the economy. Gold, in particular, is seen as a “store of value” and often attracts investors during inflationary or uncertain times, although it doesn’t produce income like stocks or real estate.

5. Inflation-Linked Bonds

Inflation-linked securities, such as U.S. Treasury Inflation-Protected Securities (TIPS), are designed specifically to guard against inflation. Their principal value adjusts according to the Consumer Price Index (CPI), and interest payments are calculated on the inflation-adjusted principal. This ensures that returns keep pace with inflation, protecting an investor’s purchasing power more directly than traditional bonds.

6. Cash and Savings Accounts

Cash holdings and low-interest savings accounts lose value quickly during inflation because their returns rarely keep up with rising prices. Even if you’re earning some interest, the real (inflation-adjusted) return may be negative, meaning your money can buy less over time. For this reason, holding too much cash in high-inflation environments can be a drag on overall portfolio performance.

7. Foreign Assets

Investing in foreign currencies, stocks, or bonds can help offset local inflation, especially if those countries have more stable prices or stronger currencies. For example, if your home currency weakens due to inflation but another currency strengthens, foreign investments may gain value when converted back. However, this approach also introduces currency exchange risks and requires careful selection of markets with favorable inflation and economic conditions.

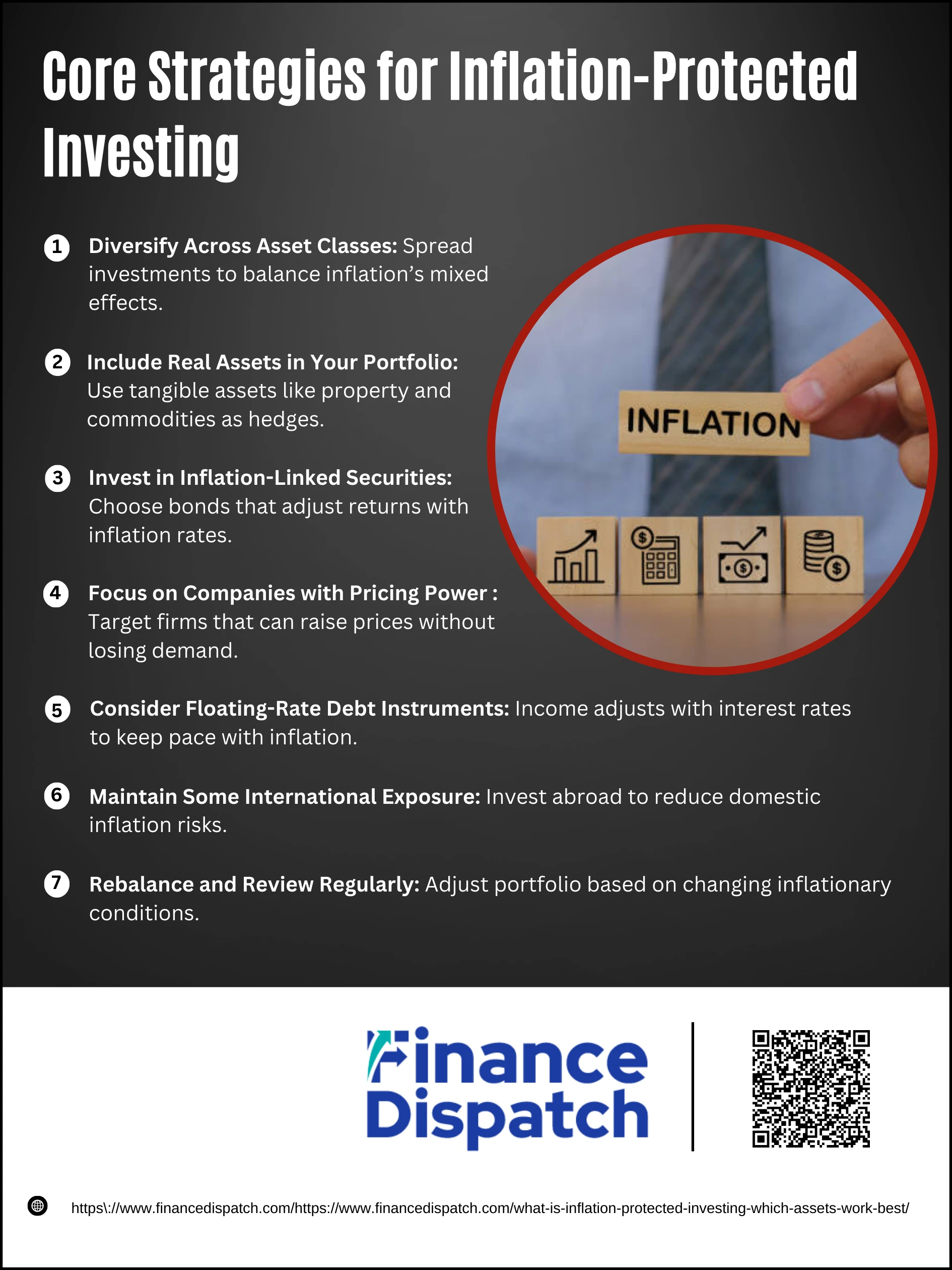

Core Strategies for Inflation-Protected Investing

Core Strategies for Inflation-Protected Investing

Inflation-protected investing is not about chasing the “perfect” asset—it’s about building a portfolio that can hold its ground when the cost of living rises. The aim is twofold: preserve your purchasing power and earn a real return that stays ahead of inflation. This involves combining asset types, looking beyond domestic markets, and regularly adjusting your holdings as conditions change. Below are key strategies that can help protect your wealth in an inflationary environment.

1. Diversify Across Asset Classes

Relying on just one type of investment leaves you vulnerable to market shifts. Inflation can hurt some assets while boosting others. For example, fixed-rate bonds may lose value, but commodities or real estate could rise. By holding a mix of stocks, bonds, real estate, commodities, and inflation-linked securities, you reduce the impact of inflation on your total portfolio and create multiple sources of return.

2. Include Real Assets in Your Portfolio

Real assets—like property, farmland, commodities, and precious metals—are tangible investments that tend to appreciate when prices climb. Real estate can generate higher rental income as living costs increase, and commodities often rise in price because they are core components of goods and services. Holding a portion of your portfolio in these assets provides a direct inflation hedge.

3. Invest in Inflation-Linked Securities

Treasury Inflation-Protected Securities (TIPS), I Bonds, and similar instruments automatically adjust their principal and interest payments based on inflation data, such as the Consumer Price Index (CPI). This ensures that your returns maintain their real value over time. They’re especially useful for conservative investors seeking steady income that won’t be eroded by rising prices.

4. Focus on Companies with Pricing Power

Some companies can pass higher costs to consumers without losing significant sales—think utility providers, healthcare companies, and major consumer brands. Investing in these types of businesses through individual stocks or sector ETFs can help maintain growth and profitability during inflationary periods.

5. Consider Floating-Rate Debt Instruments

Unlike fixed-rate bonds, floating-rate bonds and loans have interest payments that adjust with prevailing market rates. Since interest rates often rise alongside inflation, these instruments can help maintain or even increase your income stream when prices go up.

6. Maintain Some International Exposure

If inflation is a localized issue, holding assets in countries with lower inflation or stronger currencies can help offset domestic losses. Global diversification—through international stocks, bonds, or ETFs—also opens up opportunities in economies that may be benefiting from different market conditions.

7. Rebalance and Review Regularly

Inflationary pressures can change quickly based on economic policies, supply chain shifts, and geopolitical events. Regular portfolio reviews allow you to shift toward assets performing well in the current environment and reduce exposure to those that are struggling, ensuring your inflation-protection strategy stays effective.

Best Assets for Inflation Protection

Best Assets for Inflation Protection

Inflation can quietly erode the value of your money, making it essential to hold assets that can keep pace with—or even outstrip—rising prices. The best inflation-protection assets tend to either adjust their value with inflation or generate income that grows over time. While no single investment works in every economic climate, combining several inflation-resistant assets can help preserve your purchasing power. Below are some of the most effective options to consider.

1. Gold

Gold has long been considered a safe-haven asset during inflationary periods. Its value often rises when the purchasing power of currency falls, making it a reliable store of wealth. While it doesn’t produce income, it can provide portfolio stability during economic uncertainty.

2. Commodities

Essential raw materials like oil, natural gas, agricultural products, and industrial metals often climb in value as production costs rise across the economy. Commodity-focused ETFs provide broad exposure without the complexity of trading futures.

3. Real Estate

Property values and rental income generally move upward with inflation, offering both potential appreciation and a steady income stream. Real Estate Investment Trusts (REITs) make it possible to invest without directly managing property.

4. Treasury Inflation-Protected Securities (TIPS)

TIPS are U.S. government bonds that adjust their principal value in line with the Consumer Price Index (CPI). This means both the interest payments and the principal repayment are protected from inflation’s impact.

5. Dividend-Paying Stocks in Defensive Sectors

Companies in sectors like healthcare, consumer staples, and utilities often maintain steady demand and can raise prices when costs rise. Those with a history of increasing dividends can provide growing income that helps offset inflation.

6. Floating-Rate Bonds and Loans

These debt instruments have interest payments that adjust with prevailing rates, which tend to rise alongside inflation. This feature helps protect income levels in a high-inflation environment.

7. Foreign Currency and International Bonds

Holding assets in countries with lower inflation or stronger currencies can protect against domestic currency devaluation. International diversification can also reduce exposure to local economic shocks.

Comparing Asset Performance in Different Inflation & Growth Environments

Inflation affects asset classes differently depending on the overall state of economic growth. In some cases, high growth can offset inflation’s negative effects, while in others—such as stagflation (low growth with high inflation)—investment returns can suffer across the board. By examining how assets perform under different combinations of inflation and growth, investors can make more informed allocation decisions. The table below summarizes typical performance patterns based on historical trends.

| Asset Class | High Growth / High Inflation | Medium Growth / High Inflation | Low Growth / High Inflation (Stagflation) |

| U.S. Equities | Strong performance; pricing power supports earnings | Moderate gains; sector selection critical | Weak performance; profits squeezed |

| Emerging Markets Equities | Often lead returns; benefit from rapid growth | Outperform developed markets; higher volatility | Underperform; vulnerable to capital outflows |

| Developed International Equities | Solid returns; supported by global demand | Moderate gains; mixed sector performance | Declines; growth constraints dominate |

| Gold | Gains as a hedge; benefits from uncertainty | Strong hedge; stable or rising prices | Mixed; can rise sharply if confidence erodes |

| Commodities | Strong gains from higher demand and costs | Gains from supply constraints and pricing | Volatile; may underperform if demand weakens |

| REITs (Real Estate) | Benefit from rising rents and values | Modest gains; sensitive to rate hikes | Weak; higher rates and low demand hurt values |

| U.S. Treasuries | Underperform; higher rates lower prices | Flat to negative; inflation erodes value | Best among weak options; capital preservation |

| Investment Grade Bonds | Modest returns; rate sensitivity a risk | Underperform; real yields fall | Slightly positive; defensive positioning helps |

| Emerging Markets Debt | Stronger when growth supports repayment | Mixed; currency risks matter | Weak; higher risk of defaults |

| High Yield Bonds | Good returns with growth-driven credit strength | Mixed; selective gains possible | Poor; defaults rise |

Practical Steps to Build an Inflation-Protected Portfolio

Building an inflation-protected portfolio is about more than just picking a few assets—it’s about creating a well-balanced mix that can adapt to changing economic conditions. The aim is to preserve purchasing power, maintain steady income, and capture growth opportunities even when prices are rising. By following a structured approach, you can position your portfolio to handle both inflationary spikes and long-term cost-of-living increases.

1. Assess Your Current Portfolio – Review your holdings to identify assets vulnerable to inflation, such as long-term fixed-rate bonds or excessive cash reserves.

2. Define Financial Goals and Risk Tolerance – Clarify whether your priority is income stability, capital growth, or a balance of both, and match your strategy to your comfort with market fluctuations.

3. Incorporate Inflation-Resistant Assets – Allocate to TIPS, real estate, commodities, and equities in sectors with pricing power to provide multiple layers of protection.

4. Diversify Across Markets and Sectors – Spread investments across asset classes, industries, and geographic regions to reduce concentration risk.

5. Include Income-Producing Investments – Favor assets that generate income that can grow over time, such as dividend-paying stocks or rental properties.

6. Consider Floating-Rate and Short-Duration Bonds – These debt instruments can adjust more quickly to rising interest rates, helping preserve real returns.

7. Review and Rebalance Regularly – Monitor market trends and inflation data, and adjust your portfolio to maintain the intended asset mix and risk profile.

Risks and Limitations of Inflation-Protected Assets

Inflation-protected assets can play an important role in preserving purchasing power, but they are not without drawbacks. While these investments are designed to adjust with rising prices, they can still be affected by market conditions, interest rate changes, and other economic factors. Understanding the potential risks and limitations can help you set realistic expectations and avoid overreliance on any single asset type.

1. Interest Rate Risk – Rising interest rates can reduce the market value of inflation-protected bonds, particularly if you sell before maturity.

2. Tax Implications – Inflation adjustments on certain bonds (like TIPS) can be taxable in the year they occur, even if you don’t receive the cash immediately (“phantom income”).

3. Liquidity Constraints – Some inflation-protected investments, such as certain real estate holdings or corporate inflation-linked bonds, can be harder to sell quickly without affecting price.

4. Opportunity Cost – In periods of low inflation, these assets may underperform stocks or traditional bonds, limiting your overall returns.

5. Deflation Risk – If prices fall, the principal or income from inflation-linked assets may decrease, reducing the benefits you expected.

6. Currency and Market Risks for Foreign Assets – Holding international inflation-protected securities can introduce currency fluctuations and geopolitical uncertainties.

7. Volatility in Certain Asset Classes – Commodities and gold, while often considered inflation hedges, can experience significant short-term price swings unrelated to inflation.

Conclusion

Inflation is an unavoidable force that can steadily erode the value of your money, but with a thoughtful strategy, you can protect your portfolio and even thrive in rising-price environments. No single asset can completely shield you from inflation, which is why diversification—across asset classes, sectors, and geographies—is essential. By combining inflation-protected securities, real assets, equities with pricing power, and other strategic investments, you can create a balanced approach that safeguards purchasing power while still allowing for growth. The key is to remain proactive—monitoring economic trends, rebalancing when necessary, and staying committed to a long-term plan that aligns with your goals and risk tolerance.