Healthcare costs are rising globally, making it more important than ever to have a financial safety net. Health insurance serves as a crucial tool in managing medical expenses, ensuring that you receive the necessary care without facing overwhelming financial burdens. Whether it’s a routine doctor’s visit, an unexpected hospital stay, or treatment for a critical illness, health insurance helps cover these costs, reducing out-of-pocket expenses. Without it, medical emergencies can lead to significant financial strain, even pushing individuals into debt or bankruptcy. This article explores what health insurance is, how it works, and why it is essential for safeguarding your health and finances.

What is Health Insurance?

Health insurance is a financial agreement between an individual and an insurance provider that helps cover medical expenses in exchange for a regular premium. It acts as a safeguard against high healthcare costs, ensuring that policyholders receive necessary medical treatments without bearing the full financial burden. Depending on the plan, health insurance can cover doctor visits, hospital stays, prescription medications, surgeries, and preventive care. In most cases, policyholders share some costs through deductibles, co-pays, or coinsurance before the insurance coverage fully kicks in. With rising medical expenses, health insurance plays a vital role in providing access to quality healthcare while preventing financial hardship.

Why is Health Insurance Crucial for Managing Medical Expenses?

Why is Health Insurance Crucial for Managing Medical Expenses?

Medical expenses are one of the biggest financial burdens people face today. Whether it’s a minor illness, an unexpected accident, or a chronic condition requiring long-term treatment, healthcare costs can quickly add up. Without insurance, even basic medical consultations, tests, or hospitalizations can become financially overwhelming. Health insurance provides a structured way to manage these costs, ensuring that individuals and families receive timely medical care without depleting their savings. It not only covers hospitalization but also includes preventive care, prescription medications, and critical treatments, reducing the risk of financial hardship due to unexpected health issues.

Key Reasons Why Health Insurance is Essential for Managing Medical Costs:

1. Protection against High Medical Bills

Unexpected medical emergencies, such as surgeries, intensive care stays, or specialized treatments, can cost thousands of dollars. Health insurance significantly reduces these costs by covering a major portion of medical expenses, preventing out-of-pocket financial strain.

2. Coverage for Preventive Care

Many insurance plans cover preventive healthcare services, including annual check-ups, vaccinations, and screenings. These services help detect diseases early, leading to timely treatment and reducing long-term medical expenses.

3. Cashless Treatment at Network Hospitals

Most health insurance providers partner with hospitals to offer cashless treatment, meaning the insurer directly settles the bills with the hospital. This eliminates the stress of arranging large sums of money for emergency medical care.

4. Access to Expensive Treatments

Treatments for critical illnesses such as cancer, kidney disease, or heart surgery can be extremely costly. Health insurance covers specialized treatments, expensive medications, and advanced procedures that might otherwise be unaffordable for many individuals.

5. Out-of-Pocket Expense Limits

Health insurance plans come with an out-of-pocket maximum, ensuring that once you reach a certain limit in deductibles, co-pays, or coinsurance, the insurer covers the remaining expenses for the year. This cap protects policyholders from excessive financial burdens.

6. Financial Security for Families

A medical emergency in the family can drain savings, affecting long-term financial goals such as buying a home, education, or retirement planning. Health insurance prevents such financial setbacks by covering medical expenses and preserving savings for the future.

7. Support During Job Loss or Retirement

Employer-sponsored health insurance benefits are lost when an individual leaves a job. Having personal health insurance ensures continued coverage, offering financial security even during transitions such as retirement or unemployment.

8. Tax Benefits

In many countries, premiums paid for health insurance policies qualify for tax deductions, reducing taxable income and providing additional financial savings. This makes health insurance a smart financial investment.

9. Coverage for Maternity and Newborn Care

Many health insurance plans offer maternity benefits, covering prenatal care, delivery expenses, and newborn care. This ensures financial ease during one of the most significant phases of life.

10. Peace of Mind

Beyond financial security, health insurance provides peace of mind. Knowing that you have coverage for medical emergencies allows you to focus on your health and recovery rather than worrying about how to pay for treatment.

How Health Insurance Works

How Health Insurance Works

Health insurance provides a financial safety net by covering medical expenses in exchange for a regular premium. It helps individuals and families afford healthcare services such as doctor visits, hospital stays, medications, and preventive care. Understanding how health insurance works is essential for making informed decisions about coverage, costs, and benefits. The process typically involves paying premiums, meeting deductibles, and sharing costs through co-pays and coinsurance before full coverage kicks in. Below is a step-by-step breakdown of how health insurance functions.

Steps in How Health Insurance Works:

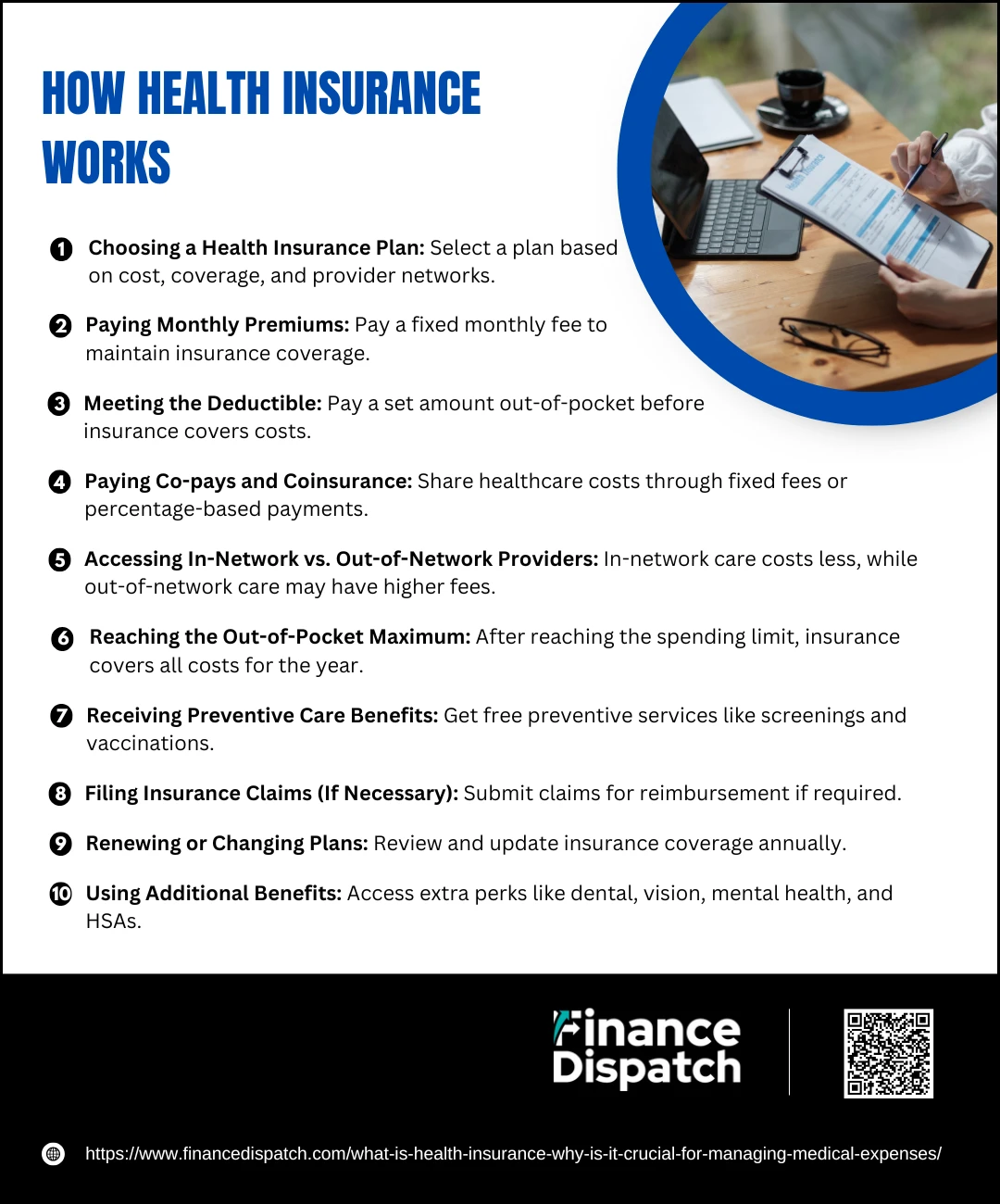

1. Choosing a Health Insurance Plan

You select a health insurance policy based on factors like premium cost, coverage options, network hospitals, and deductible amounts. Plans may be obtained through an employer, government programs, or private insurers.

2. Paying Monthly Premiums

To maintain coverage, policyholders pay a fixed monthly premium. The cost varies depending on the type of plan, coverage level, and individual factors such as age and medical history.

3. Meeting the Deductible

Before insurance starts covering costs, policyholders must pay a certain amount out-of-pocket, known as the deductible. Plans with higher deductibles usually have lower monthly premiums and vice versa.

4. Paying Co-pays and Coinsurance

Even after meeting the deductible, policyholders often pay a portion of medical expenses through co-pays (fixed fees for doctor visits or prescriptions) or coinsurance (a percentage of costs shared with the insurer).

5. Accessing In-Network vs. Out-of-Network Providers

Insurance companies have a network of approved healthcare providers. Visiting an in-network provider costs less, while out-of-network providers may require higher payments or may not be covered at all.

6. Reaching the Out-of-Pocket Maximum

Once the total amount spent on deductibles, co-pays, and coinsurance reaches a set limit, the insurer covers 100% of covered healthcare costs for the remainder of the policy year.

7. Receiving Preventive Care Benefits

Many health insurance plans include preventive services such as vaccinations, screenings, and annual check-ups at no additional cost, helping to detect and prevent illnesses early.

8. Filing Insurance Claims (If Necessary)

In some cases, policyholders may need to submit claims to their insurer for reimbursement, especially if they receive out-of-network care or need coverage verification.

9. Renewing or Changing Plans

Health insurance plans are typically renewed annually, allowing policyholders to review their coverage and make adjustments based on changing healthcare needs.

10. Using Additional Benefits

Some plans offer extra benefits such as maternity coverage, dental and vision care, mental health services, and access to health savings accounts (HSAs) for tax-advantaged medical spending.

Types of Health Insurance Plans

Types of Health Insurance Plans

Choosing the right health insurance plan is essential for ensuring access to quality healthcare while managing costs effectively. Different plans offer varying levels of coverage, flexibility, and cost-sharing structures. Some plans provide broad coverage for all medical needs, while others are designed for specific situations, such as maternity care or critical illness coverage. Understanding the different types of health insurance plans can help individuals, families, and employers select the best option to meet their healthcare and financial needs.

Common Types of Health Insurance Plans:

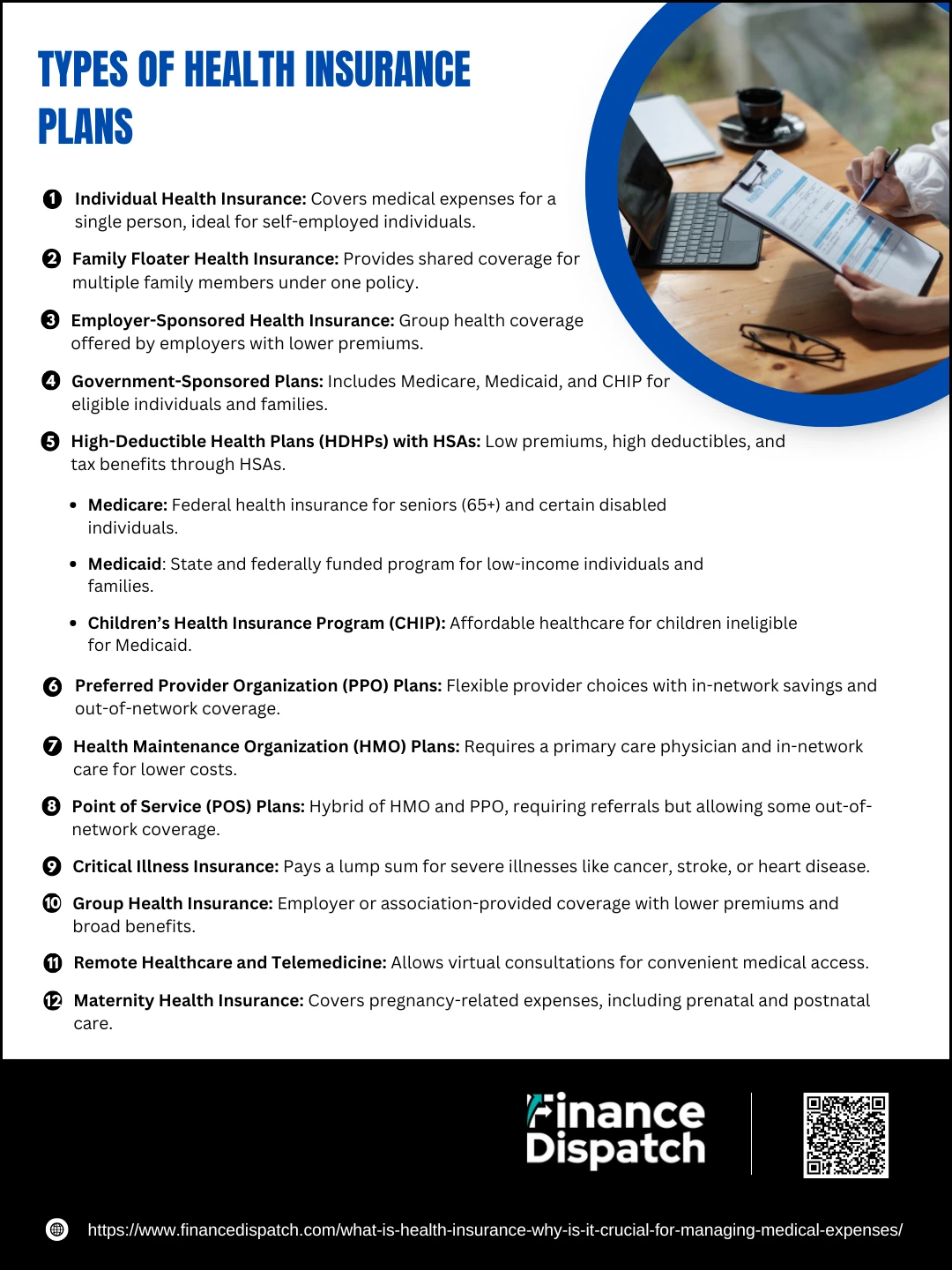

1. Individual Health Insurance

This type of policy is designed for a single person and covers medical expenses such as doctor visits, hospitalization, prescription medications, and preventive care. It is ideal for self-employed individuals or those without employer-sponsored coverage.

2. Family Floater Health Insurance

A family floater plan covers multiple family members under a single policy. The sum insured is shared among all covered members, making it a cost-effective option compared to buying separate individual plans for each person. It typically includes spouse, children, and sometimes parents.

3. Employer-Sponsored Health Insurance

Many employers offer health insurance as part of employee benefits. These plans often have lower premiums since employers cover a portion of the cost. They provide group coverage, making healthcare more affordable for employees and their dependents.

4. Government-Sponsored Plans:

- Medicare – A federal program providing health coverage for individuals aged 65 and older, as well as those with certain disabilities or medical conditions. It includes different parts:

-

- Part A (Hospital Insurance)

- Part B (Medical Insurance)

- Part C (Medicare Advantage Plans)

- Part D (Prescription Drug Coverage)

-

- Medicaid – A state and federally funded program that provides free or low-cost health coverage to low-income individuals and families. Eligibility and benefits vary by state.

- Children’s Health Insurance Program (CHIP) – Provides affordable healthcare coverage for children in low-income families who do not qualify for Medicaid.

5. High-Deductible Health Plans (HDHPs) with Health Savings Accounts (HSAs)

These plans have lower monthly premiums but higher deductibles. They are suitable for individuals who do not expect frequent medical expenses and want to save money. Paired with an HSA, they offer tax benefits by allowing pre-tax savings for qualified medical expenses.

6. Preferred Provider Organization (PPO) Plans

PPO plans offer flexibility in choosing healthcare providers. Members can visit any doctor or specialist without needing a referral. While they get lower costs for in-network providers, they still have coverage for out-of-network services at a higher cost.

7. Health Maintenance Organization (HMO) Plans

HMO plans require policyholders to choose a primary care physician (PCP) who coordinates their care. Specialist visits need referrals from the PCP, and coverage is limited to in-network providers. These plans generally have lower premiums and out-of-pocket costs.

8. Point of Service (POS) Plans

POS plans combine aspects of HMO and PPO plans. Like an HMO, members need a referral from their PCP to see specialists, but they can also receive partial coverage for out-of-network providers, similar to a PPO.

9. Critical Illness Insurance

This policy provides a lump sum payout upon the diagnosis of severe illnesses such as cancer, stroke, or heart disease. The payout can be used for treatment costs, household expenses, or income replacement during recovery.

10. Group Health Insurance

This type of plan is offered by employers, associations, or organizations to a group of people, such as employees or members. It typically offers lower premiums and broader coverage than individual plans.

11. Short-Term Health Insurance

Temporary insurance that provides coverage for a limited period, usually up to a year. It is designed for individuals transitioning between jobs, waiting for employer-sponsored coverage, or those who missed open enrollment for a regular plan. These plans often have limited coverage and do not cover pre-existing conditions.

12. Maternity Health Insurance

Specifically designed for pregnancy-related expenses, including prenatal care, delivery, and postnatal care. Many standard health insurance policies include maternity benefits, but standalone maternity insurance is also available for additional coverage.

Key Features of Health Insurance Plans

Health insurance plans come with various features that determine the level of coverage, cost-sharing, and benefits available to policyholders. Understanding these key features helps individuals choose a plan that meets their healthcare needs and financial situation. From premiums and deductibles to co-pays and coverage limits, each aspect plays a crucial role in how a health insurance policy functions. Below is a table highlighting the key features of health insurance plans and their descriptions.

Table: Key Features of Health Insurance Plans

| Feature | Description |

| Premium | The monthly or annual amount paid to maintain health insurance coverage. |

| Deductible | The amount policyholders must pay out-of-pocket before the insurance begins covering medical expenses. |

| Co-pay (Copayment) | A fixed amount paid for specific medical services (e.g., doctor visits, prescription drugs) at the time of service. |

| Coinsurance | The percentage of medical costs shared between the policyholder and the insurer after meeting the deductible. |

| Out-of-Pocket Maximum | The maximum amount a policyholder has to pay in a year before the insurance covers 100% of eligible expenses. |

| Network Coverage | Specifies whether healthcare providers and hospitals are in-network (lower cost) or out-of-network (higher cost). |

| Pre-existing Conditions Coverage | Determines whether a plan covers medical conditions that existed before purchasing the policy. Many plans now cover pre-existing conditions due to regulations like the ACA. |

| Preventive Care Benefits | Includes services such as vaccinations, screenings, and annual check-ups, often covered at no extra cost. |

| Prescription Drug Coverage | Covers the cost of medications, with different levels of coverage depending on the drug formulary and tier system. |

| Hospitalization Coverage | Pays for hospital stays, surgeries, and inpatient medical care. |

| Maternity and Newborn Care | Some plans include coverage for pregnancy, childbirth, and postnatal care for both mother and baby. |

| Emergency Services | Covers emergency room visits and urgent care, often with set co-pays or cost-sharing. |

| Mental Health Coverage | Provides benefits for counseling, therapy, psychiatric services, and substance abuse treatment. |

| Rehabilitation Services | Covers physical therapy, occupational therapy, and other rehabilitative treatments. |

| Cashless Treatment | Allows policyholders to receive treatment at network hospitals without upfront payments, as the insurer settles the bill directly. |

| Health Savings Account (HSA) Eligibility | High-Deductible Health Plans (HDHPs) allow policyholders to use tax-free Health Savings Accounts for medical expenses. |

| Waiting Period | The time a policyholder must wait before certain coverages become effective (e.g., maternity benefits or pre-existing conditions). |

How to Choose the Right Health Insurance Plan?

How to Choose the Right Health Insurance Plan?

Choosing the right health insurance plan is a critical step in ensuring that you and your family have access to quality healthcare without unnecessary financial strain. With numerous options available, each offering different coverage levels, cost structures, and benefits, selecting the best plan requires careful evaluation. The ideal plan should provide adequate coverage for medical expenses while keeping premiums, deductibles, and out-of-pocket costs manageable. Whether you’re selecting an individual, family, or employer-sponsored plan, it’s essential to consider your healthcare needs, budget, and potential future medical expenses. Below are key factors to guide you in making an informed choice.

Key Factors to Consider When Choosing a Health Insurance Plan:

1. Assess Your Healthcare Needs

Before selecting a plan, consider your medical history, existing health conditions, and expected healthcare needs. If you require frequent doctor visits, prescription medications, or specialist care, opt for a comprehensive plan with broader coverage. If you are generally healthy, a high-deductible plan with lower premiums might be a cost-effective choice.

2. Compare Premiums and Deductibles

Health insurance plans come with different cost structures. Plans with low premiums often have higher deductibles, meaning you’ll pay more out-of-pocket before insurance covers expenses. Conversely, plans with higher premiums usually have lower deductibles, making them suitable for those who need frequent medical care. Choose a plan that balances affordability with your healthcare usage.

3. Check Network Hospitals and Doctors

Insurance providers have a network of hospitals, clinics, and doctors that they cover at lower rates. Ensure that your preferred healthcare providers are included in the insurer’s network. Visiting out-of-network providers can result in higher costs or non-coverage.

4. Understand Co-pays, Coinsurance, and Out-of-Pocket Maximums

In addition to premiums and deductibles, evaluate co-pays (fixed costs for services), coinsurance (percentage you pay after meeting the deductible), and the out-of-pocket maximum (the highest amount you will pay in a year before the insurance covers all costs).

5. Look for Coverage of Essential Benefits

A good health insurance plan should cover essential services, including preventive care, emergency services, hospitalization, prescription drugs, maternity care, mental health treatment, and rehabilitative services.

6. Consider Family Coverage Options

If you are selecting a policy for your family, look into family floater plans that cover all members under a single sum insured. Also, check for maternity benefits, pediatric care, and coverage for dependent children.

7. Evaluate Additional Benefits

Some plans offer extra benefits such as cashless hospitalization, wellness programs, dental and vision care, critical illness coverage, and no-claim bonuses. These features can add value to your policy.

8. Check Policy Exclusions and Waiting Periods

Every insurance plan has exclusions—services or conditions it does not cover. Read the policy carefully to understand exclusions, waiting periods for pre-existing conditions, and limitations on specific treatments.

9. Look for Tax Benefits

In many countries, health insurance premiums qualify for tax deductions, helping you save money while securing medical coverage. Check your local tax regulations to maximize benefits.

10. Compare Plans Using Online Tools

Many insurance providers and government marketplaces offer online comparison tools to evaluate different plans side by side. These tools help compare costs, benefits, and coverage options to make an informed decision.

The Affordable Care Act (ACA) and Its Impact on Health Insurance

The Affordable Care Act (ACA), signed into law in 2010, brought significant reforms to the U.S. healthcare system, making health insurance more accessible and affordable for millions of Americans. One of its key provisions was the expansion of Medicaid eligibility, allowing low-income individuals and families to qualify for government-funded healthcare coverage. The ACA also introduced the Health Insurance Marketplace, where individuals and small businesses could compare and purchase standardized insurance plans, often with government subsidies to lower costs. A major impact of the ACA was its protection for people with pre-existing conditions, preventing insurance companies from denying coverage or charging higher premiums based on medical history. Additionally, the law required insurers to cover essential health benefits such as preventive care, maternity services, mental health treatment, and prescription drugs. Young adults were also allowed to remain on their parents’ insurance plans until the age of 26, extending coverage for millions. Though the ACA faced political and legal challenges, its implementation led to a significant reduction in the uninsured rate across the country, improving healthcare access and financial security for many Americans.

Common Health Insurance Terms Explained

Health insurance can be confusing due to the many terms used in policies. Understanding these key terms helps you make informed decisions about costs, coverage, and benefits. Below is a list of commonly used health insurance terms with their meanings.

Key Health Insurance Terms:

1. Premium: The monthly or annual amount paid to maintain health insurance coverage.

2. Deductible: The amount you pay out-of-pocket before your insurance starts covering costs.

3. Co-pay (Copayment): A fixed fee you pay for specific medical services, like doctor visits or prescriptions.

4. Coinsurance: The percentage of medical costs you share with your insurer after meeting the deductible.

5. Out-of-Pocket Maximum: The highest amount you pay annually before insurance covers all further costs.

6. Network: A group of doctors and hospitals that contract with an insurer to provide discounted rates.

7. In-Network vs. Out-of-Network: In-network providers cost less; out-of-network care may be more expensive or not covered.

8. HMO (Health Maintenance Organization): Requires a primary care doctor and referrals for specialists, covering only in-network providers.

9. PPO (Preferred Provider Organization): Offers flexibility to see any doctor, with lower costs for in-network care.

10. High-Deductible Health Plan (HDHP): A plan with lower premiums but higher deductibles, often paired with an HSA.

11. Health Savings Account (HSA): A tax-advantaged savings account used for medical expenses with an HDHP.

12. Essential Health Benefits: Required coverage under the ACA, including hospitalization, preventive care, and maternity services.

13. Pre-existing Condition: A health issue that existed before obtaining insurance; the ACA prevents insurers from denying coverage.

14. Preventive Care: Services like screenings, vaccines, and annual check-ups covered at no extra cost.

15. Medicare: A government health program for people over 65 or with disabilities.

16. Medicaid: A government program providing healthcare for low-income individuals and families.

Benefits of Health Insurance Beyond Financial Coverage

Benefits of Health Insurance Beyond Financial Coverage

Health insurance is often viewed primarily as a financial tool that helps cover medical expenses, reducing the burden of high hospital bills. However, its benefits extend far beyond just monetary savings. A good health insurance plan ensures access to quality healthcare, encourages preventive care, and enhances overall well-being. Many modern insurance policies now include wellness programs, mental health support, maternity care, and alternative treatments that improve long-term health. With the rise of telemedicine and digital healthcare solutions, health insurance also makes medical services more accessible than ever. Below are the key benefits of health insurance that go beyond just financial coverage.

Key Benefits of Health Insurance Beyond Financial Coverage:

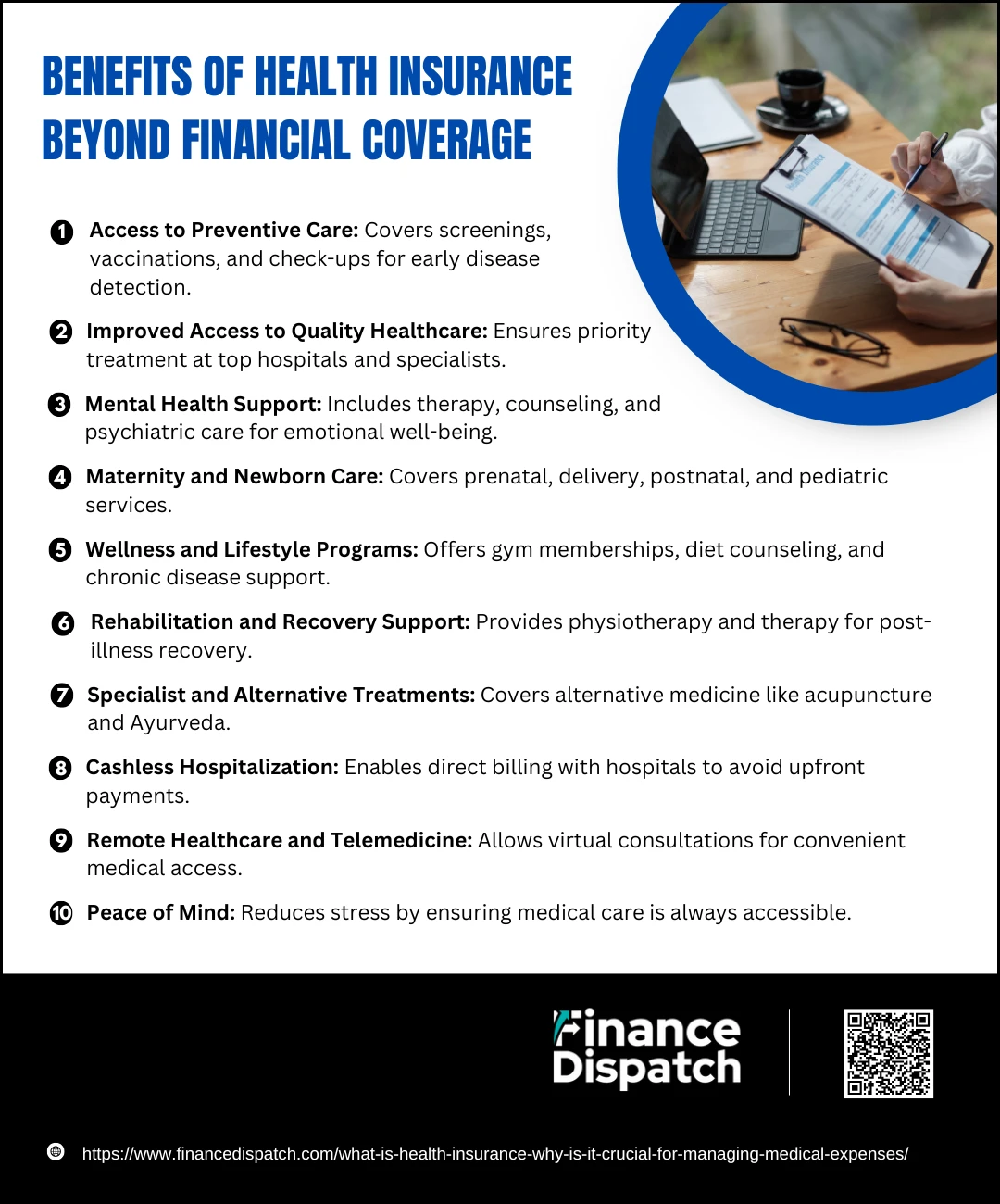

1. Access to Preventive Care

Most health insurance plans cover preventive services such as vaccinations, screenings, and annual health check-ups at no extra cost. Early detection of health conditions like diabetes, high blood pressure, or cancer can lead to timely treatment and better health outcomes.

2. Improved Access to Quality Healthcare

Having health insurance ensures access to the best hospitals, specialists, and advanced medical procedures. Policyholders can receive faster and better treatment compared to those without insurance, as many hospitals prioritize insured patients for consultations and procedures.

3. Mental Health Support

Many health insurance plans now include mental health coverage, offering therapy sessions, counseling, psychiatric services, and medication for mental health conditions such as anxiety and depression. This helps in maintaining emotional well-being and reducing stress.

4. Maternity and Newborn Care

Comprehensive insurance plans provide coverage for prenatal check-ups, hospital delivery, and postnatal care for both the mother and newborn. Some policies also cover newborn vaccinations and pediatric care, ensuring the health of both mother and baby.

5. Wellness and Lifestyle Programs

Many insurers offer lifestyle programs that promote overall well-being, such as gym memberships, diet counseling, smoking cessation programs, and chronic disease management support. These initiatives encourage healthier living and prevent long-term health problems.

6. Rehabilitation and Recovery Support

After a major illness, accident, or surgery, rehabilitation is crucial for recovery. Health insurance often covers physiotherapy, occupational therapy, and other rehabilitation services to help patients regain mobility and strength.

7. Specialist and Alternative Treatments

Some health insurance policies include coverage for alternative treatments such as chiropractic care, acupuncture, naturopathy, or Ayurveda. These options provide additional healthcare solutions for individuals seeking holistic treatment approaches.

8. Cashless Hospitalization

In case of emergencies or planned treatments, many insurance policies offer cashless hospitalization, meaning policyholders do not need to arrange large sums of money upfront. The insurance provider directly settles the bills with the hospital, reducing financial stress.

9. Remote Healthcare and Telemedicine

With advancements in digital healthcare, many insurers now offer telemedicine services. This allows policyholders to consult with doctors remotely via phone or video calls, ensuring easy access to medical advice anytime, anywhere.

10. Peace of Mind

Beyond the tangible health benefits, having insurance provides reassurance that medical care is available when needed. It reduces the stress of worrying about sudden health issues, allowing individuals and families to focus on their well-being rather than financial concerns.

Conclusion

Health insurance is more than just a financial safety net—it is a vital tool that ensures access to quality healthcare, promotes preventive care, and enhances overall well-being. Beyond covering medical expenses, it offers benefits such as mental health support, maternity care, rehabilitation services, and wellness programs, all of which contribute to a healthier life. With advancements in telemedicine and cashless hospitalization, health insurance has made healthcare more accessible and stress-free. Choosing the right plan tailored to your needs provides long-term security and peace of mind, ensuring that you and your loved ones receive timely and high-quality medical care without financial strain. Investing in health insurance today is an investment in a healthier and more secure future.