In today’s fast-paced financial world, robo-advisory has emerged as a transformative force, redefining how people approach investment strategies. Powered by advanced algorithms and artificial intelligence, robo-advisors offer automated, data-driven solutions for managing investments. These digital platforms provide personalized recommendations by assessing individual financial goals, risk tolerance, and market trends. By combining accessibility, affordability, and precision, robo-advisory bridges the gap between traditional financial advising and modern technology, making wealth management more inclusive and efficient. This article explores the concept of robo-advisory and delves into its role in tailoring investment strategies to suit diverse needs and preferences.

What is Robo-Advisory?

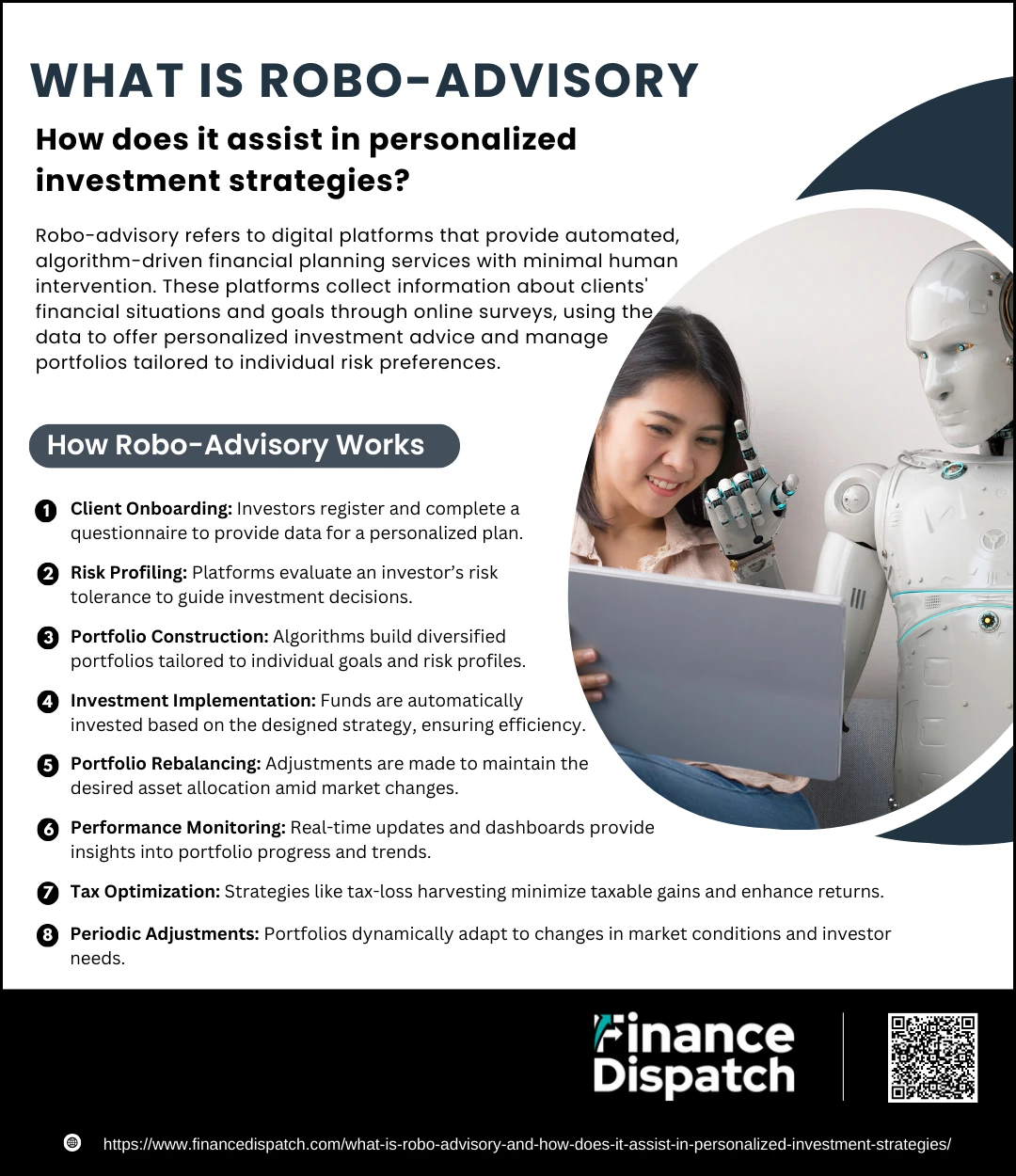

Robo-advisory refers to digital platforms that provide automated, algorithm-driven financial planning and investment management services. These platforms utilize advanced technologies such as artificial intelligence, machine learning, and big data analytics to create personalized investment strategies. Unlike traditional financial advisors, robo-advisors operate online and require minimal human intervention, making them highly accessible and cost-effective. By analyzing factors like an individual’s financial goals, risk appetite, and investment horizon, robo-advisors offer customized solutions for wealth management. With their ability to simplify complex investment decisions, robo-advisors are becoming an essential tool for both novice and experienced investors seeking efficient and tailored financial guidance.

How Robo-Advisory Works

Robo-advisory platforms revolutionize investment management by leveraging advanced algorithms and digital tools to deliver personalized, efficient, and cost-effective financial guidance. By automating key aspects of portfolio creation and maintenance, these platforms cater to both novice and experienced investors. They utilize data-driven insights to assess an investor’s needs and design strategies tailored to their goals and risk preferences. Below is a detailed step-by-step explanation of how robo-advisory works:

1. Client Onboarding

The journey begins with users registering on the platform and completing a detailed questionnaire. This form collects vital information about their financial situation, investment goals, income, expenses, and timeline. The insights gathered during onboarding serve as the foundation for designing a personalized investment plan.

2. Risk Profiling

Robo-advisors use the data from the questionnaire to assess the investor’s risk tolerance. This involves understanding how comfortable the user is with potential losses or market volatility. Based on this evaluation, the platform classifies investors into categories such as conservative, moderate, or aggressive, which guide subsequent investment decisions.

3. Portfolio Construction

Using pre-defined algorithms and financial models, the robo-advisor constructs a diversified investment portfolio. This portfolio allocates funds across various asset classes such as stocks, bonds, ETFs, or mutual funds. The allocation is designed to match the investor’s risk profile and long-term financial goals, ensuring optimal balance between risk and return.

4. Investment Implementation

Once the portfolio is created, the platform automatically implements the strategy by investing the user’s funds. This eliminates manual intervention, ensuring that the investment process is seamless and efficient. The system ensures the allocations remain aligned with the pre-designed strategy.

5. Portfolio Rebalancing

Market movements can cause a portfolio’s allocation to deviate from its intended design. Robo-advisors monitor these changes and periodically rebalance the portfolio to maintain the desired risk-return profile. For example, if the equity portion grows disproportionately due to market gains, the system will adjust by reallocating funds to other asset classes.

6. Performance Monitoring

The platform provides continuous monitoring of portfolio performance, offering real-time updates through dashboards. Investors can review their progress toward financial goals, access reports, and gain insights into market trends. This transparency builds trust and allows users to make informed decisions.

7. Tax Optimization

Advanced robo-advisors often include features like tax-loss harvesting, where they strategically sell underperforming assets to offset taxable gains. This ensures that investors can maximize their returns while staying tax-efficient.

8. Periodic Adjustments

Robo-advisors are dynamic, adapting to changes in market conditions or user preferences. If an investor’s financial situation evolves, such as achieving a milestone or altering risk tolerance, the platform adjusts the portfolio accordingly to reflect the new goals.

Features of Robo-Advisory

Robo-advisory platforms have reshaped the investment landscape by introducing innovative, technology-driven solutions that simplify financial planning and portfolio management. They are designed to cater to a diverse range of investors, offering features that combine convenience, customization, and cost-effectiveness. These platforms rely on advanced algorithms and data analytics to provide highly personalized investment strategies. Below is a detailed look at the features that make robo-advisors stand out:

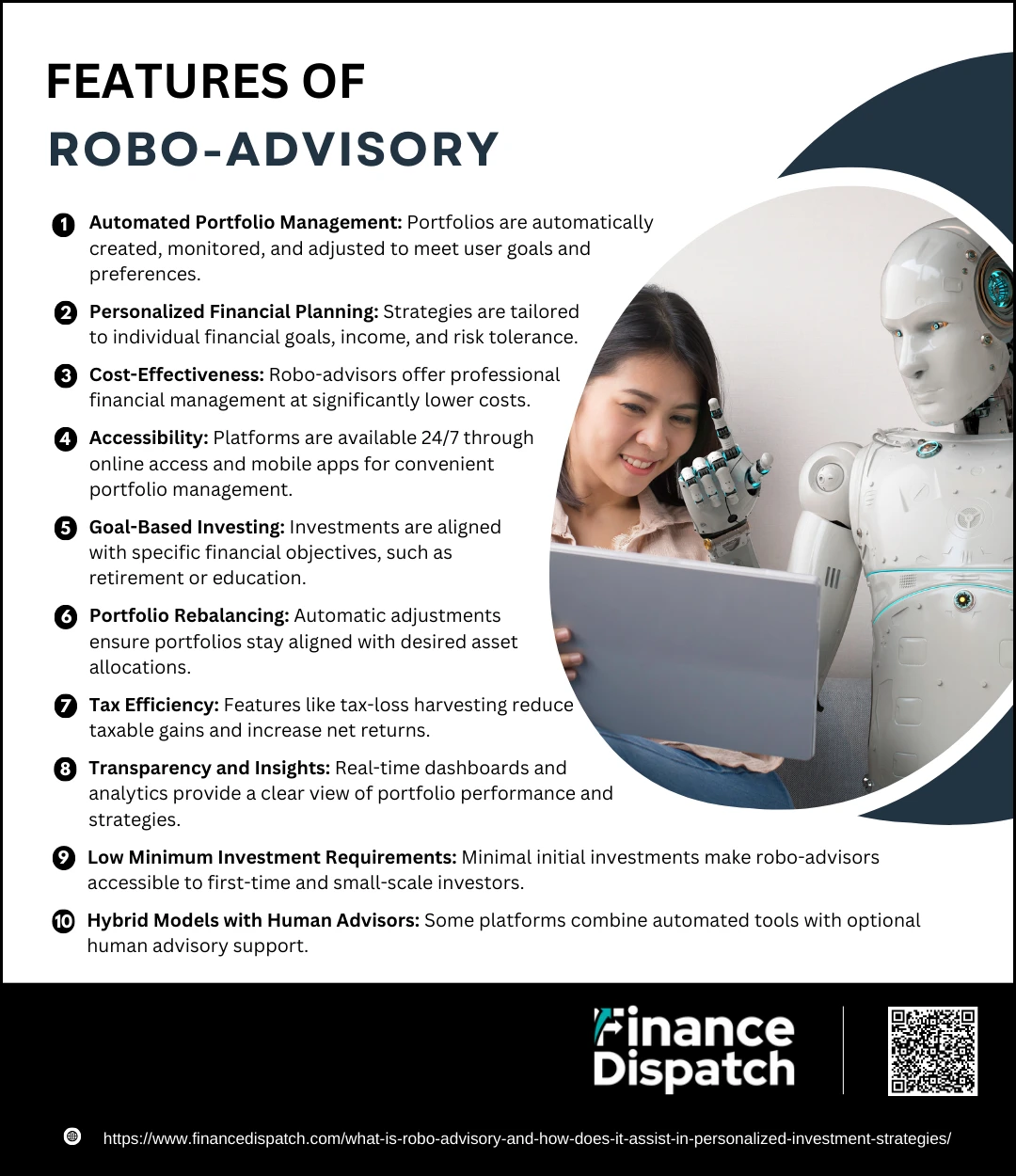

1. Automated Portfolio Management

Robo-advisors automatically design and manage investment portfolios based on individual preferences and market trends. They continuously monitor and adjust the portfolio to align with the user’s goals and risk tolerance.

2. Personalized Financial Planning

By gathering information about an investor’s goals, income, and risk appetite, robo-advisors offer tailored investment strategies. This ensures a highly customized approach that adapts to changing financial circumstances.

3. Cost-Effectiveness

Robo-advisors operate at a fraction of the cost of traditional financial advisors. They achieve this by automating processes, making professional-grade financial management accessible to more people.

4. Accessibility

Available 24/7 via online platforms or mobile apps, robo-advisors offer unmatched convenience. Investors can easily track, manage, or modify their portfolios from anywhere in the world.

5. Goal-Based Investing

These platforms help investors define and achieve specific objectives, such as buying a home, funding education, or building a retirement corpus. The investments are strategically aligned with these goals.

6. Portfolio Rebalancing

Market fluctuations can cause an investment portfolio to drift from its intended allocation. Robo-advisors automatically rebalance the portfolio, ensuring it stays within the desired asset distribution.

7. Tax Efficiency

Many robo-advisors include tax-loss harvesting, a process where underperforming assets are sold to offset taxable gains, reducing the overall tax burden and increasing net returns.

8. Transparency and Insights

Robo-advisors provide real-time dashboards and detailed analytics, giving users a comprehensive view of their investments. This transparency builds trust and allows for informed decision-making.

9. Low Minimum Investment Requirements

Unlike traditional financial services, which often require significant initial investments, robo-advisors typically allow users to start with small amounts, making them accessible to first-time investors.

10. Hybrid Models with Human Advisors

Some robo-advisors offer the option of consulting with human advisors, blending the efficiency of technology with the expertise and empathy of traditional financial guidance.

Personalized Investment Strategies via Robo-Advisory

Robo-advisory platforms have redefined the way investors manage their portfolios by providing tailored strategies designed to meet individual financial goals and preferences. These digital platforms combine advanced algorithms with big data analytics to ensure that every investment decision is customized and aligned with the user’s needs. They adapt seamlessly to changes in personal circumstances and market dynamics, offering a level of personalization that was once exclusive to traditional financial advisors. Here’s a detailed look at how robo-advisors deliver personalized investment strategies:

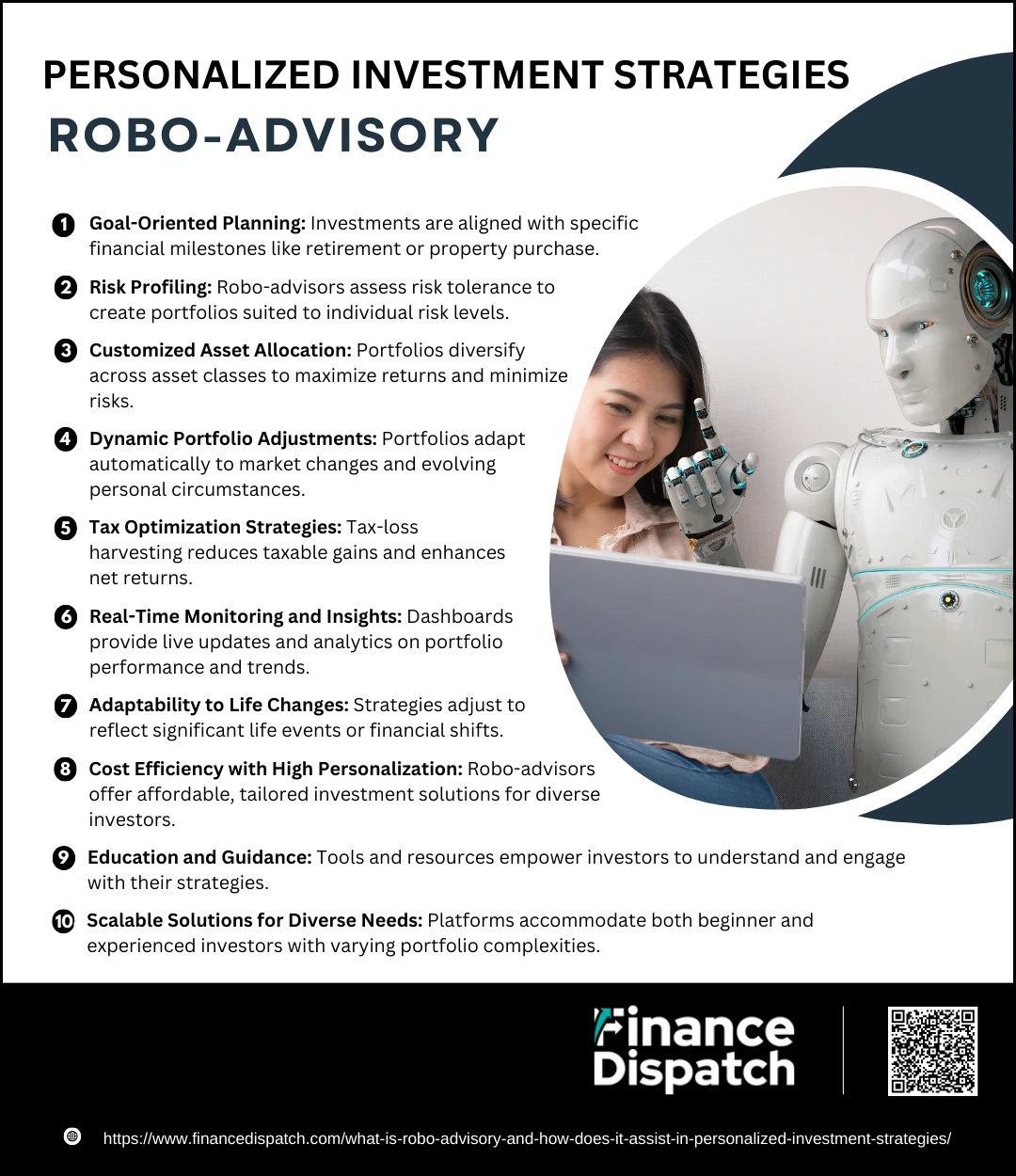

1. Goal-Oriented Planning

Robo-advisors assist users in identifying specific financial milestones, such as saving for retirement, building a college fund, or purchasing property. By aligning investments with these goals, they create focused and achievable strategies tailored to each objective.

2. Risk Profiling

Every investor has a unique tolerance for risk. Robo-advisors use comprehensive questionnaires to gauge factors like investment knowledge, financial stability, and emotional readiness for market fluctuations. Based on this analysis, they categorize users into risk profiles (e.g., conservative, balanced, aggressive) to guide portfolio creation.

3. Customized Asset Allocation

Robo-advisors design portfolios that diversify investments across asset classes like equities, bonds, and exchange-traded funds (ETFs). This diversification is optimized to match the investor’s risk profile and maximize returns while minimizing exposure to unnecessary risks.

4. Dynamic Portfolio Adjustments

Markets are volatile, and life circumstances often change. Robo-advisors constantly monitor these factors, automatically adjusting portfolios to ensure they stay aligned with the investor’s long-term goals and risk tolerance. For example, they may shift allocations from high-risk stocks to stable bonds as retirement approaches.

5. Tax Optimization Strategies

Advanced robo-advisors offer tax-efficient investing features like tax-loss harvesting, where underperforming assets are sold to offset taxable gains. This strategy reduces the tax burden and boosts overall returns, particularly for high-income investors.

6. Real-Time Monitoring and Insights

Investors have access to intuitive dashboards that provide real-time updates on portfolio performance. Detailed analytics and market insights empower users to understand their investments better and stay informed about market trends.

7. Adaptability to Life Changes

Significant life events, such as a career change, marriage, or having children, often impact financial goals. Robo-advisors adjust strategies to reflect these changes, ensuring that the investment approach remains relevant and effective.

8. Cost Efficiency with High Personalization

Traditional financial advisors often charge high fees for tailored strategies. Robo-advisors democratize access to personalized investment solutions by delivering similar services at significantly lower costs, making them accessible to a broader audience.

9. Education and Guidance

Many platforms incorporate educational tools and resources to help users understand the principles behind their personalized strategies. This feature bridges the gap for novice investors, making them more confident and informed participants in their financial journey.

10. Scalable Solutions for Diverse Needs

Robo-advisors cater to a wide range of investors, from beginners with minimal capital to seasoned professionals managing complex portfolios. This scalability ensures that every investor, regardless of their financial background, can benefit from a personalized approach.

Benefits of Using Robo-Advisory

Robo-advisory platforms are transforming the financial landscape by offering innovative, accessible, and cost-efficient investment solutions. These platforms leverage cutting-edge technology to manage portfolios, providing personalized strategies and streamlining complex financial processes. Whether you are a novice investor or an experienced professional, robo-advisors cater to diverse financial needs with precision and adaptability. Here’s a detailed look at the benefits of using robo-advisory:

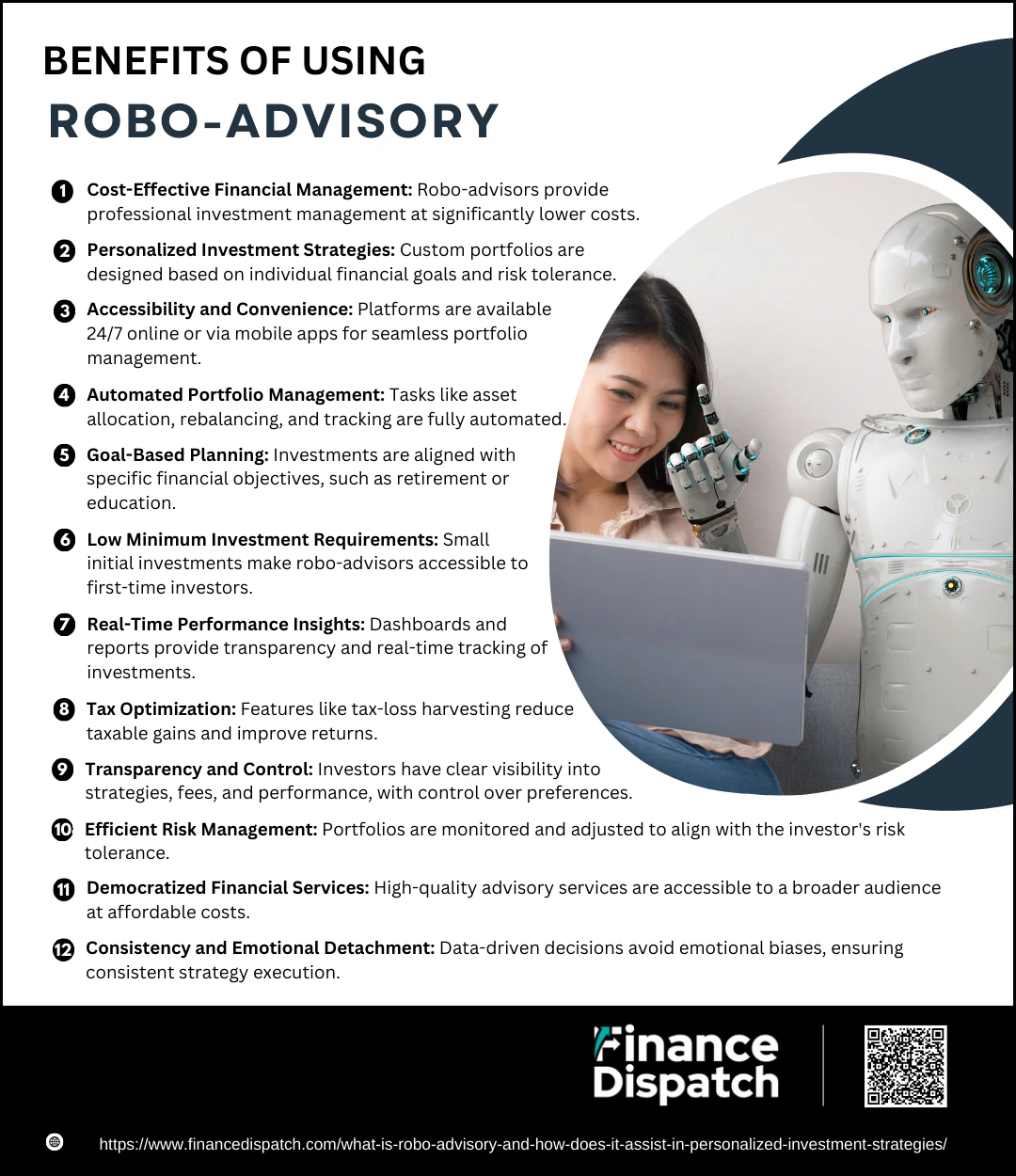

1. Cost-Effective Financial Management

Robo-advisors charge significantly lower fees compared to traditional financial advisors, often using a flat percentage of assets under management. This affordability opens doors for investors who might have previously found professional advisory services out of reach.

2. Personalized Investment Strategies

By analyzing data such as financial goals, income, and risk tolerance, robo-advisors create customized portfolios that align with individual needs. This ensures that each investment plan is tailored for optimal outcomes, whether it’s for short-term growth or long-term wealth building.

3. Accessibility and Convenience

Available 24/7 through online platforms and mobile apps, robo-advisors allow users to manage their investments anytime and from anywhere. This eliminates the need for scheduling in-person consultations, offering unparalleled convenience.

4. Automated Portfolio Management

Robo-advisors handle tasks such as asset allocation, portfolio rebalancing, and performance tracking. This automation reduces the time and effort required for manual management, ensuring that portfolios remain optimized without constant oversight.

5. Goal-Based Planning

These platforms enable users to set specific financial objectives, such as saving for a home, retirement, or education, and design investment strategies to achieve these goals. They track progress, keeping investors aligned with their targets.

6. Low Minimum Investment Requirements

Unlike traditional financial advisors that often require substantial initial capital, many robo-advisors allow users to start with minimal investments. This makes investing accessible to young or first-time investors.

7. Real-Time Performance Insights

Robo-advisors provide detailed dashboards and performance reports, offering transparency into how investments are performing. Users can easily track their progress and gain insights into market trends, enhancing decision-making.

8. Tax Optimization

Advanced features like tax-loss harvesting minimize taxable gains, helping users retain more of their earnings. This is especially beneficial for investors in higher tax brackets seeking efficient tax management.

9. Transparency and Control

Investors have complete visibility into their portfolios, including allocation strategies, fees, and performance metrics. Robo-advisors also allow users to adjust their risk preferences or financial goals as needed, providing a balance of automation and user control.

10. Efficient Risk Management

Robo-advisors continuously monitor market conditions and make necessary adjustments to portfolios, ensuring they align with the investor’s risk tolerance. This proactive approach minimizes potential losses and maximizes returns.

11. Democratized Financial Services

By offering high-quality advisory services at low costs, robo-advisors make professional-grade investment management accessible to a broader audience, bridging the gap between expert financial guidance and everyday investors.

12. Consistency and Emotional Detachment

Unlike human advisors or individual investors who might make decisions influenced by emotions, robo-advisors rely solely on data and algorithms. This ensures consistency in strategy execution, even during volatile market periods.

Challenges and Limitations of Robo-Advisory

While robo-advisory platforms offer significant advantages, they are not without challenges and limitations. One of the primary concerns is the lack of human interaction, which can be a drawback for investors seeking personalized advice or guidance on complex financial situations. Robo-advisors rely heavily on algorithms and predefined models, which may not adequately account for sudden market disruptions or unique individual circumstances. Additionally, their dependency on user-provided data means that inaccurate or incomplete information can lead to suboptimal recommendations. Security and privacy concerns also arise, as these platforms handle sensitive financial data that could be vulnerable to cyber threats. Furthermore, robo-advisors may not cater well to high-net-worth individuals or those with sophisticated investment needs, as they often focus on basic asset classes like stocks and bonds. These limitations highlight the importance of understanding the scope and boundaries of robo-advisory services before relying on them for comprehensive financial planning.

Comparing Robo-Advisory with Traditional Advisory

Robo-advisory and traditional advisory services offer distinct approaches to financial planning and investment management, catering to different types of investors. Robo-advisors leverage advanced algorithms to deliver low-cost, automated, and accessible solutions, while traditional advisors provide personalized guidance and human expertise, often at a higher cost. Understanding the key differences between these two models can help investors choose the option that best suits their financial goals and preferences.

| Aspect | Robo-Advisory | Traditional Advisory |

| Cost | Low fees (usually 0.25%-0.50% of AUM) | Higher fees (1%-2% of AUM or hourly rates) |

| Personalization | Algorithm-based, tailored to user inputs | Deeply personalized through human interaction |

| Accessibility | Available 24/7 via online platforms and mobile apps | Requires scheduled meetings, often during business hours |

| Minimum Investment | Low or no minimum investment required | Often requires a high minimum investment |

| Human Interaction | None or limited (some offer hybrid models with advisors) | Full access to a financial advisor for guidance |

| Service Scope | Focused on basic asset classes like stocks and bonds | Broader range of services, including estate planning and tax advice |

| Decision-Making | Automated, emotion-free decision-making | Can include emotional and subjective judgment |

| Complex Needs | May struggle with complex financial scenarios | Well-suited for addressing sophisticated financial needs |

| Speed and Efficiency | Fast execution and real-time adjustments | May take longer due to manual processes |

| Transparency | High, with real-time dashboards and clear fee structures | Varies, often less transparent in terms of fees and processes |

Future of Robo-Advisory in Personalized Investments

The future of robo-advisory in personalized investments is poised for significant growth and innovation as technology continues to advance. With the integration of artificial intelligence, machine learning, and big data analytics, robo-advisors are expected to deliver even more accurate, tailored, and dynamic investment strategies. Enhanced features like real-time risk management, predictive analytics, and seamless integration with other financial tools will cater to the evolving needs of investors. Additionally, as financial literacy improves and trust in digital platforms grows, robo-advisors will likely expand their reach, democratizing access to professional-grade financial planning for a global audience. The hybrid model, combining digital automation with human expertise, is also expected to gain traction, bridging the gap for investors who seek both efficiency and personalized guidance. With these developments, robo-advisory platforms are set to play a pivotal role in shaping the future of wealth management and personalized investments.

Conclusion

Robo-advisory has revolutionized the world of investment management by making personalized financial strategies accessible, affordable, and efficient. By leveraging advanced algorithms, these platforms offer tailored solutions that cater to diverse investor needs, from beginners to seasoned professionals. Despite certain limitations, such as the lack of human interaction and challenges with complex financial scenarios, robo-advisors continue to evolve, integrating advanced technologies and hybrid models to address these gaps. As the financial landscape becomes increasingly digitized, robo-advisory platforms are positioned to play a central role in empowering individuals to achieve their financial goals with confidence and ease. Whether used independently or alongside traditional advisors, robo-advisors are shaping a future where investing is more inclusive, transparent, and data-driven.