Life is unpredictable, and sometimes, even the best precautions can’t shield you from unexpected events. That’s where umbrella insurance steps in. It’s not just for the wealthy; this extra layer of liability protection can safeguard anyone with assets to protect. Whether you’re a homeowner, a landlord, or someone who loves outdoor activities, umbrella insurance offers peace of mind by covering costs that exceed the limits of your regular insurance policies. From lawsuits to unexpected accidents, understanding what umbrella insurance is and who needs it could make all the difference in securing your financial future.

What Is Umbrella Insurance?

Umbrella insurance is a type of extra liability insurance that provides coverage beyond the limits of your existing policies, such as auto, homeowners, or renters insurance. It’s designed to protect your assets and future income in situations where your standard insurance falls short. This policy not only covers claims for injuries and property damage but also extends to certain lawsuits, like those for libel or slander. Essentially, it acts as a financial safety net, shielding you from the potential fallout of costly legal claims or damages that exceed the coverage limits of your primary policies.

Coverage Comparison Table

| Aspect | Umbrella Insurance Covers | Umbrella Insurance Does Not Cover |

| Personal Liability | Injuries to others caused by accidents (e.g., car or property-related) | Injuries to the policyholder or household members |

| Property Damage | Damages to someone else’s property | Damage to the policyholder’s own property |

| Legal Protection | Lawsuits involving defamation, libel, slander | Liability from intentional or criminal acts |

| Broader Coverage | Covers claims exceeding primary policy limits | Business-related liabilities unless explicitly covered |

| Scope of Application | Global coverage for personal liability issues | Breaches of contract or liabilities linked to war |

How Does Umbrella Insurance Work?

Umbrella insurance works as an extra layer of protection that kicks in when the liability limits of your existing policies, like auto or homeowners insurance, are exhausted. For example, if you’re at fault in a car accident that results in damages exceeding your auto insurance coverage, your umbrella policy steps in to cover the remaining costs, up to its limit. Additionally, umbrella insurance can cover certain claims not included in standard policies, such as lawsuits for libel, slander, or defamation. It typically requires you to carry a minimum amount of liability coverage on your primary policies and can also extend to members of your household, ensuring broader protection. Essentially, it safeguards your savings, assets, and future earnings from unexpected liabilities, providing peace of mind in worst-case scenarios.

Key Features of Umbrella Insurance

Umbrella insurance is a valuable tool for anyone seeking additional liability protection that goes beyond standard insurance policies. It not only provides financial security in cases of significant legal claims or damages but also covers a range of scenarios that other policies often exclude. Here are the key features that make umbrella insurance an essential safeguard:

- Extended Liability Coverage

Umbrella insurance steps in when the limits of your existing policies, like auto or homeowners insurance, are exhausted. For example, if you cause a car accident resulting in damages exceeding your auto policy, the umbrella policy will cover the remaining costs, ensuring you’re not left paying out of pocket. - Global Coverage

Unlike standard policies, umbrella insurance often provides liability protection worldwide. Whether you’re traveling for leisure or business, it covers incidents involving injury to others or damage to their property, safeguarding your assets even abroad. - Legal Defense Costs

Lawsuits can be expensive, with legal fees quickly adding up. Umbrella insurance covers the costs associated with your legal defense, including attorney fees and court expenses, even if the lawsuit’s damages are within your policy’s coverage limits. - Personal Liability Protection

Beyond physical damages, umbrella insurance covers personal liability issues such as libel, slander, defamation, and false imprisonment. These claims, which are not typically covered under standard policies, can result in significant financial strain without an umbrella policy. - Household Protection

The coverage isn’t limited to just you. Umbrella insurance extends to members of your household, such as a teenage driver or family member who unintentionally causes damage or injury, ensuring broader protection for your loved ones. - Affordable Premiums

Umbrella insurance offers high liability limits at relatively low costs. A $1 million policy typically costs between $150 and $300 annually, making it a cost-effective way to secure substantial coverage. - Broad Asset Protection

This policy protects your savings, investments, home equity, and other assets from being seized to pay for legal judgments or settlements. It ensures that a single lawsuit doesn’t derail your financial future.

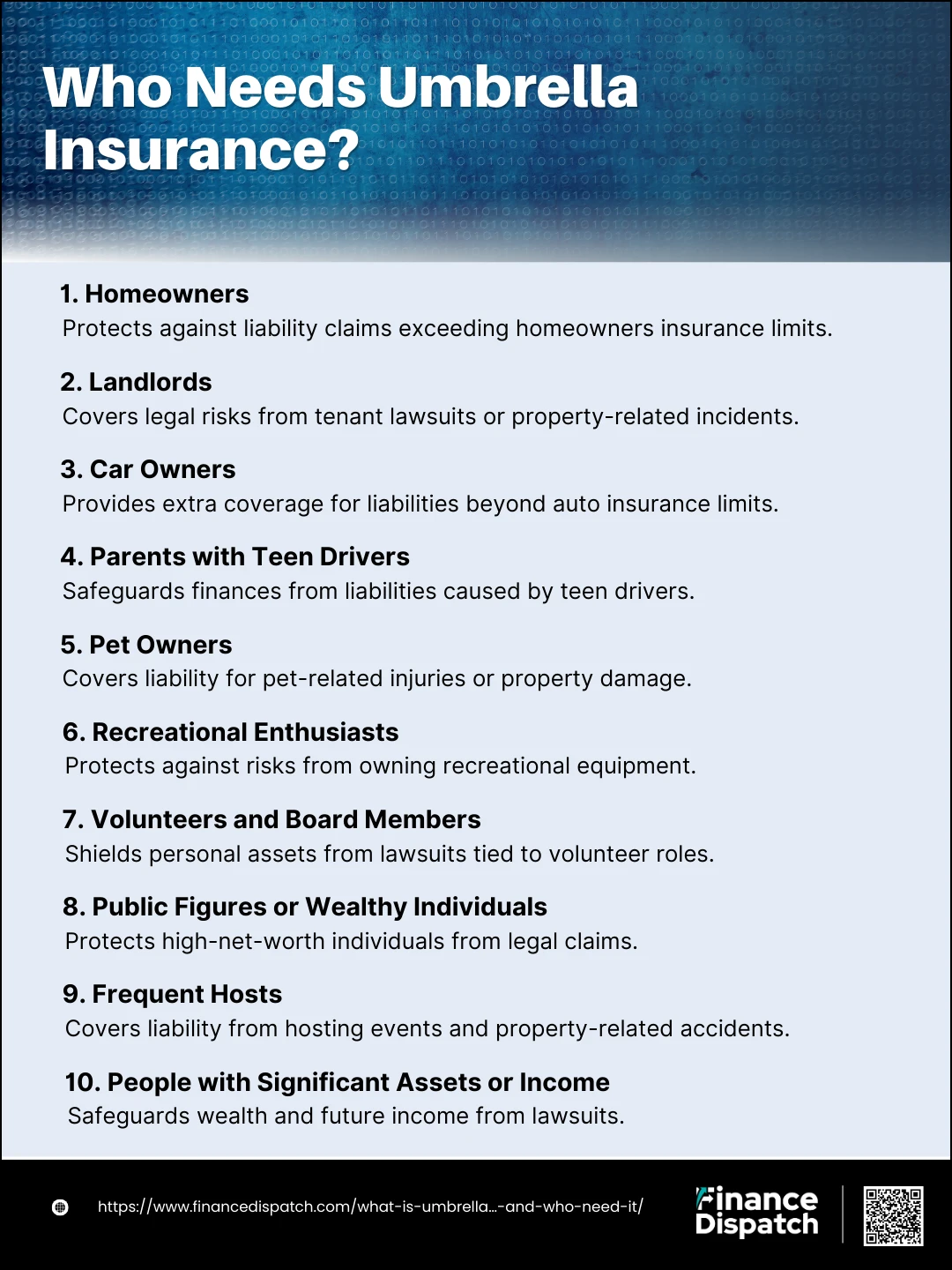

Who Needs Umbrella Insurance?

Umbrella insurance isn’t just for the wealthy; it’s a practical safeguard for anyone with assets to protect or a risk of facing significant liability claims. Whether you own property, have savings, or engage in activities that increase your chances of lawsuits, umbrella insurance can provide an essential safety net. Here’s a closer look at who can benefit the most:

1. Homeowners

Owning a home comes with inherent risks. From someone tripping on your driveway to a delivery person getting injured on your porch, you could face liability claims for accidents that occur on your property. While homeowners insurance covers a portion of these costs, umbrella insurance provides additional coverage if claims exceed your primary policy’s limits.

2. Landlords

Renting out property exposes you to legal risks, including tenant lawsuits for injuries or damages sustained on your property. For example, if a tenant trips on a broken step, they could sue you for medical expenses and lost wages. Umbrella insurance offers protection beyond what rental property insurance covers, ensuring your rental income and assets are secure.

3. Car Owners

Accidents can happen on the road, and the costs can quickly exceed the limits of your auto insurance. If you’re responsible for a severe accident involving injuries or extensive property damage, an umbrella policy helps cover the difference, sparing your personal savings and assets from depletion.

4. Parents with Teen Drivers

Teen drivers are statistically more likely to be involved in accidents due to inexperience. If your teen causes a collision resulting in significant injuries or damages, your auto insurance might not fully cover the liability. Umbrella insurance ensures you’re protected against the financial fallout.

5. Pet Owners

Even the friendliest pets can behave unpredictably. If your dog bites someone or causes property damage, you could be held liable for medical costs or legal fees. Umbrella insurance provides an extra layer of protection for such incidents, beyond what homeowners insurance covers.

6. Recreational Enthusiasts

Owning recreational equipment like swimming pools, trampolines, or ATVs can be enjoyable but also poses significant risks. Injuries or accidents involving these items can lead to expensive lawsuits. Umbrella insurance covers liabilities that go beyond the limits of your standard policies, ensuring your finances remain intact.

7. Volunteers and Board Members

Serving on nonprofit boards or volunteering for organizations can expose you to legal risks. For example, decisions you make as a board member might result in a lawsuit. Umbrella insurance extends coverage to such scenarios, protecting your personal assets from being targeted in legal claims.

8. Public Figures or Wealthy Individuals

High-net-worth individuals or public figures are often at a higher risk of being sued. This can include lawsuits for defamation, negligence, or accidents involving their property. Umbrella insurance acts as a safeguard, ensuring their wealth and lifestyle are not jeopardized by legal claims.

9. Frequent Hosts

Hosting events, whether small gatherings or large parties, increases the likelihood of accidents, such as a guest slipping on spilled drinks or getting injured on your property. Umbrella insurance provides peace of mind by covering liability claims beyond what your homeowners insurance can handle.

10. People with Significant Assets or Income

If you’ve built substantial savings, investments, or have a high earning potential, protecting these assets from lawsuits is crucial. Umbrella insurance ensures that your hard-earned wealth and future income are shielded from devastating legal judgments or settlements.

Real-Life Scenarios Where Umbrella Insurance Can Help

Life is full of unexpected situations where your regular insurance coverage may fall short, leaving you financially vulnerable. Umbrella insurance acts as a financial safety net, stepping in to cover costs that exceed your primary policy limits or for situations your standard insurance doesn’t cover. Here are some real-life scenarios where umbrella insurance can make a difference:

1. Serious Car Accident

Imagine you’re at fault in a car accident that results in extensive property damage and serious injuries to multiple people. If the total costs exceed your auto insurance liability limits, umbrella insurance will cover the remaining amount, saving you from draining your savings or assets.

2. Accident on Your Property

A guest at your home slips on an icy walkway and sustains severe injuries, resulting in a lawsuit. If the damages surpass your homeowners insurance coverage, umbrella insurance can help cover medical bills, legal fees, and settlement costs.

3. Dog Bite Incident

Your dog unexpectedly bites a neighbor, causing injury and leading to medical expenses and a lawsuit. While your homeowners insurance may cover some of the costs, an umbrella policy steps in to handle any excess liability.

4. Teenage Driver in an Accident

Your teenage child causes a multi-car accident with significant property damage and injuries. When your auto insurance reaches its limit, umbrella insurance provides the additional coverage needed to settle claims.

5. Defamation Lawsuit

You post an online review of a business that leads to a defamation lawsuit for libel or slander. Most standard insurance policies don’t cover such claims, but umbrella insurance ensures you’re protected against legal fees and damages.

6. Landlord Liability

A tenant trips on a loose floorboard in your rental property and sues for medical expenses and lost wages. Umbrella insurance covers the liability costs that exceed your landlord insurance policy.

7. Recreational Mishap

Someone gets injured while using your backyard trampoline or swimming pool. The liability costs could surpass your homeowners insurance limits, but umbrella insurance steps in to cover the excess amount.

8. Accident Abroad

While traveling internationally, you accidentally injure someone or damage their property. Umbrella insurance provides liability coverage, even when you’re outside the United States.

9. Neighborhood Dispute Escalation

A neighborhood child gets injured on your property, such as while climbing a tree in your yard. If the family sues, your umbrella policy can handle costs beyond your homeowners insurance coverage.

10. High-Stakes Legal Judgment

A lawsuit against you results in a judgment exceeding the limits of your existing policies. Without umbrella insurance, your personal savings and future income could be at risk.

Benefits of Having Umbrella Insurance

Umbrella insurance provides an extra layer of protection that can safeguard your assets and financial future in ways standard insurance policies cannot. Here are the key benefits of having umbrella insurance:

- Extra Liability Coverage

Umbrella insurance steps in when the liability limits of your auto, homeowners, or other primary policies are exhausted. This ensures you’re not left paying out of pocket for substantial claims or legal judgments. - Protection Against Lawsuits

Whether it’s a defamation claim, a personal injury lawsuit, or a property damage case, umbrella insurance covers legal fees, court costs, and settlement expenses that could otherwise drain your finances. - Broader Coverage

Unlike standard policies, umbrella insurance often covers incidents like libel, slander, or false imprisonment, which are usually excluded from primary insurance policies. - Global Protection

Umbrella insurance offers worldwide liability coverage, making it a great option if you travel frequently and want peace of mind against unexpected incidents abroad. - Affordable Premiums for High Coverage

Compared to the potential financial protection it provides, umbrella insurance is relatively inexpensive. You can often secure $1 million in coverage for just a few hundred dollars annually. - Safeguards Future Income

Lawsuits can target not only your current assets but also your future income. Umbrella insurance helps protect your financial future from garnishments or large settlements. - Extends Coverage to Household Members

Many umbrella policies cover incidents caused by family members in your household, such as a teenage driver or a pet-related accident, ensuring broader protection for your loved ones. - Peace of Mind

Knowing you have financial protection in place allows you to live without the constant worry of unexpected liabilities that could upend your life.

How Much Does Umbrella Insurance Cost?

Umbrella insurance is surprisingly affordable, especially considering the substantial financial protection it offers. The cost depends on factors such as the coverage amount, your location, and the risk level associated with your lifestyle or assets. Typically, umbrella policies are offered in increments of $1 million, with premiums that are far less than you might expect. Here’s a breakdown of the factors influencing the cost:

- Base Cost for Coverage

A $1 million umbrella insurance policy generally costs between $150 and $300 annually. Additional coverage, such as $2 million or $3 million, increases the premium incrementally. - Location

Your state of residence can impact premium costs. States with higher legal claim rates may result in slightly higher premiums for umbrella insurance. - Number of Assets Insured

Owning multiple properties, vehicles, or other assets increases the risk for claims, which can raise the cost of your umbrella policy. - Risk Profile

If you own high-risk items like swimming pools, trampolines, or recreational vehicles, or if you have teenage drivers in your household, your premiums may be higher due to increased liability exposure. - Bundling Discounts

Purchasing umbrella insurance from the same provider as your auto or homeowners policies can lead to discounts, making coverage even more affordable. - Minimum Underlying Coverage

To qualify for umbrella insurance, most providers require a minimum level of liability coverage on your primary policies. If you need to increase those limits, your overall insurance costs may rise. - Claims History

A history of liability claims may lead to higher premiums, as insurers assess you as a higher-risk policyholder.

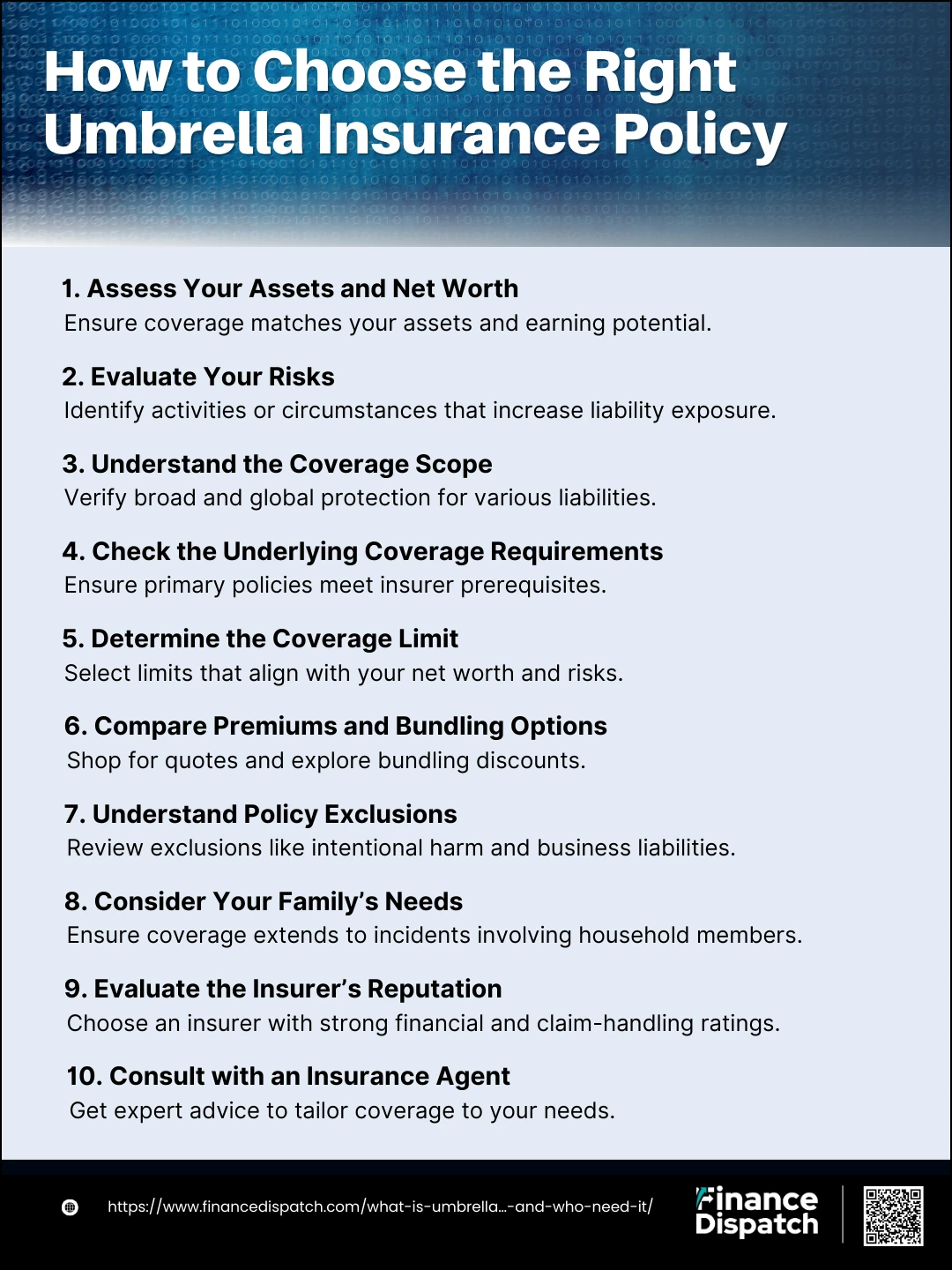

How to Choose the Right Umbrella Insurance Policy

How to Choose the Right Umbrella Insurance Policy

Selecting the right umbrella insurance policy involves understanding your coverage needs, assessing your risks, and comparing options to find the best fit for your financial situation. With a little research and careful planning, you can secure the peace of mind that comes with knowing your assets are protected. Here’s how to choose the right umbrella insurance policy:

1. Assess Your Assets and Net Worth

Start by calculating the total value of your assets, including savings, investments, real estate, and other valuable possessions. Choose a policy that provides enough coverage to protect everything you own and your future earning potential.

2. Evaluate Your Risks

Consider activities or circumstances that increase your liability risk, such as owning high-risk items (like a pool or trampoline), having a teenage driver, or serving as a landlord. Ensure your policy covers these scenarios.

3. Understand the Coverage Scope

Look for a policy that provides broad protection, including coverage for personal injury claims, property damage, defamation, and other liabilities. Verify whether it includes global coverage if you travel frequently.

4. Check the Underlying Coverage Requirements

Most insurers require minimum liability coverage on your primary policies (e.g., auto and homeowners insurance) to qualify for an umbrella policy. Make sure your existing coverage meets these requirements.

5. Determine the Coverage Limit

Umbrella policies are typically available in $1 million increments. Choose a coverage limit that aligns with your net worth and potential risks, ensuring your assets are fully protected.

6. Compare Premiums and Bundling Options

Request quotes from multiple insurers and inquire about discounts for bundling your umbrella policy with your existing auto or homeowners insurance. Bundling can reduce overall costs while simplifying policy management.

7. Understand Policy Exclusions

Review the exclusions in the policy carefully. Common exclusions include intentional harm, liability from business activities, and breach of contract. Make sure you’re comfortable with what the policy doesn’t cover.

8. Consider Your Family’s Needs

If you have family members in your household, ensure the policy extends coverage to incidents caused by them, such as a child causing an accident or a pet-related injury.

9. Evaluate the Insurer’s Reputation

Research the financial stability, customer service, and claim-handling reputation of the insurance provider. A reliable insurer ensures smooth claim processing when you need it.

10. Consult with an Insurance Agent

Speak with a trusted insurance professional to discuss your unique needs and risks. They can help tailor a policy that provides the best protection for your circumstances.

Why is umbrella insurance important?

Umbrella insurance is important because it provides an additional layer of financial protection when your primary insurance policies, such as auto or homeowners insurance, fall short. In today’s world, lawsuits and liability claims can result in costs that far exceed standard policy limits, putting your savings, assets, and even future earnings at risk. Whether it’s a car accident with substantial damages, an injury on your property, or a defamation claim, umbrella insurance steps in to cover the excess costs, including legal fees. It ensures that one unexpected event doesn’t lead to financial ruin, offering peace of mind and safeguarding your hard-earned assets.

Conclusion

Umbrella insurance is a vital tool for protecting your financial future and ensuring peace of mind in a world filled with uncertainties. By providing extended liability coverage beyond your standard insurance policies, it shields you from the devastating impact of costly lawsuits, accidents, and unexpected claims. Whether you’re safeguarding your assets, future earnings, or family’s security, an umbrella policy offers a safety net that is both affordable and invaluable. Investing in umbrella insurance isn’t just about covering risks—it’s about securing the life you’ve worked hard to build.